CEO Morning Brief

Heineken Malaysia’s Earnings Forecasts Raised on Beer Demand Recovery

edgeinvest

Publish date: Tue, 16 Aug 2022, 08:45 AM

KUALA LUMPUR (Aug 15): Analysts have raised their earnings forecasts for Heineken Malaysia Bhd, after the brewing company's latest results for the first half ended June 30, 2022 (1HFY22) came in above their expectations.

Hong Leong Investment Bank (HLIB) Research said in a note on Monday (Aug 15) that Heineken's 1HFY22 core net profit of RM199.5 million was above the research house's and the market consensus’ forecasts of 58% and 63% respectively.

Heineken Malaysia’s net profit doubled to RM199.5 million in 1HFY22, compared with RM98.81 million in 1HFY21, mainly driven by robust sales performance during the festive period and steady recovery for the on-trade business.

Post results, HLIB revised Heineken's earnings forecasts upward by 2% to 7% for FY22-FY24, on the assumption of higher sales volume and stronger recovery in beer demand. HLIB is estimated to register earnings of RM369.3 million, RM372.8 million and RM377.4 million for FY22-FY24 respectively.

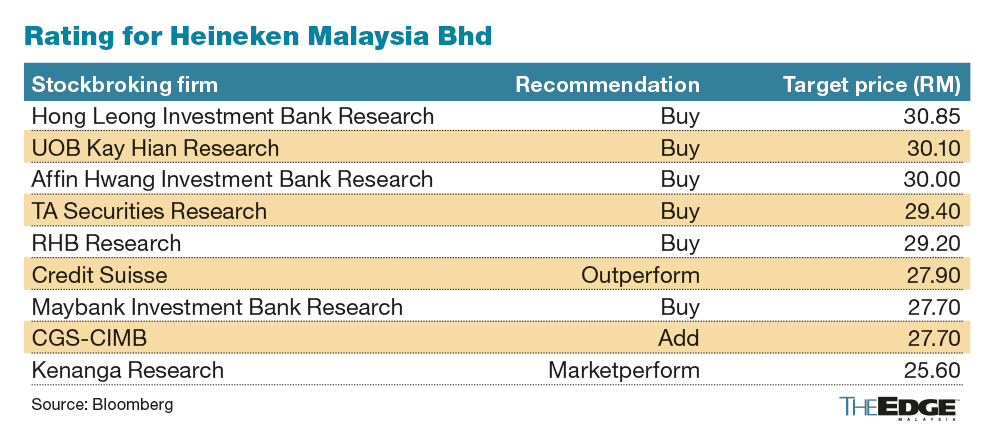

As a result, the target price (TP) for the company was raised to RM30.85 from RM28.87 previously, implying a price-to-earnings multiple of 25 times based on FY23 earnings per share of 123.4 sen, said HLIB, which reiterated a “buy” recommendation on the stock.

Kenanga Research, meanwhile, raised Heineken’s FY22 and FY23 profit forecasts by 12% and 3% to RM361 million and RM388 million each. However, considering a higher risk premium due to elevated inflation, the research house lowered its TP by 7% to RM25.60 from RM27.40.

At the same, Kenanga downgraded Heineken to "market perform" from "outperform", given that the decent share price performance in recent months has exhausted its upside potential.

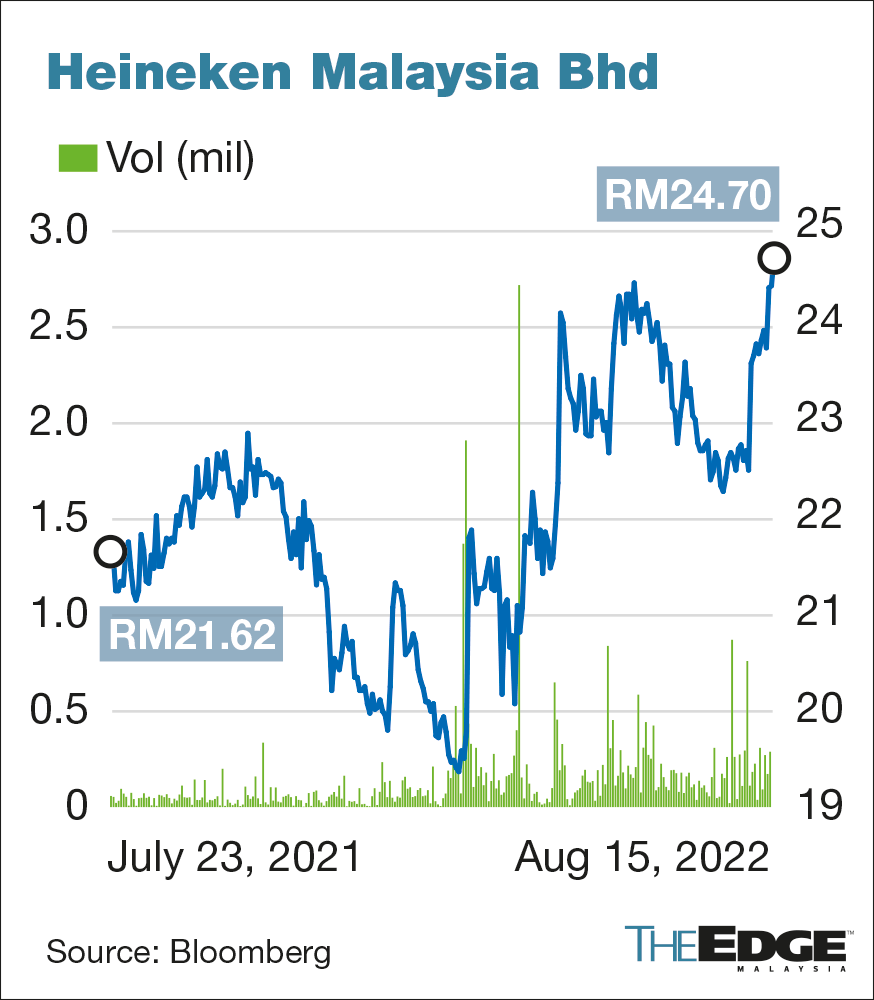

On Monday, Heineken Malaysia’s share price finished up 30 sen or 1.23% at RM24.70 — valuing it at RM7.46 billion, with some 288,400 shares exchanging hands, making it the third-largest gainer across the local bourse. Year to date, the stock has risen 13.93%.

Bloomberg data showed that there are 10 “buy” calls, one “hold” and one “sell” for the company, with a 12-month TP of RM28.30.

Meanwhile, RHB Research raised its FY22-FY24 profit forecasts by 9%, 5% and 1% to RM348 million, RM390 million and RM408 million respectively.

"Correspondingly, our TP rises to RM29.20 (inclusive of a 6% ESG premium), as we also take [the] opportunity to revise our risk assumptions to factor in the rising rate environment.”

Beer price hike to cushion margin erosion

Given the pent-up demand for out-of-home consumption, the strong return of foreign tourists and the upcoming 2022 FIFA World Cup, beer sales are expected to remain strong in 2H22, HLIB said. In particular, the depreciation of the ringgit, which has a positive impact on domestic tourism, is expected to lead to stronger foreign tourist arrivals in 2H22, boosting retail sales.

“Despite lingering concern on demand slowing down after Heineken raised its beer price by 6%-8% (both off-trade and on-trade) effective Aug 1 in response to the rising input cost, we are not overly concerned as beer remains the cheapest alcoholic drink in the market, and thus has relatively inelastic demand.

“We opine the price hike, together with better operating leverage (due to the absence of forced brewery closures) and “premiumisation push” should help cushion any margin erosion arising from cost inflation,” the research house explained.

Looking at past performance, Kenanga highlighted that the impact on sales volume was relatively “muted” when Heineken Malaysia raised prices by 5% to 7% in 4Q21. This time, however, may see some erosion of demand as high inflation affects consumers' disposable income.

Also, there is a concern over a potential hike in excise duty on alcoholic products in the coming budget, given that the industry has been relatively spared since the rebasing of the excise calculation in 2016 and a direct excise increase in 2006 by 23% to RM7.40/litre, from RM6.00/litre.

RHB opined that the premiumisation strategy, product innovation, and effective marketing campaigns will mitigate some headwinds — such as supply chain disruptions, rising input costs, weakening ringgit, and inflation — while the implementation of price increases should protect the group’s margins.

“On top of that, we also foresee sustainable volume recovery, particularly in the on-trade segments on the back of broader containment of pandemic and economic recovery. These should underpin the 42% earnings growth in FY22, notwithstanding the higher tax expenses arising from the prosperity tax,” it added.

Source: TheEdge - 16 Aug 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on CEO Morning Brief

China Condemns US’ Overcapacity Claim Just Before Blinken Visit

Created by edgeinvest | Apr 24, 2024

Thailand to Replace Military-appointed Senate, Reduce Its Powers

Created by edgeinvest | Apr 24, 2024

Shadow Banking Stress in South Korea Sends Warning to Global Investors

Created by edgeinvest | Apr 24, 2024

Indonesia's Biggest Party Confirms President Jokowi No Longer a Member After Backing Prabowo

Created by edgeinvest | Apr 24, 2024

Telegram Founder Says China Downloads Have Not Fallen Since Apple Move

Created by edgeinvest | Apr 24, 2024

Indian Watchdog Said to Have Queried Global Funds Over Manipulation of Adani Stocks

Created by edgeinvest | Apr 24, 2024

China’s Surging Steel Exports Are Inflaming Global Trade Tensions

Created by edgeinvest | Apr 24, 2024

Bubble Tea Maker Chabaidao Slumps 38% in HK’s Biggest Debut This Year

Created by edgeinvest | Apr 24, 2024

Commodities Are a ‘win-win’ With US$100 Oil in Sight, Carlyle’s Currie Says

Created by edgeinvest | Apr 24, 2024

Japan Issues Strongest Warning Yet on Readiness to Intervene in Currency Market

Created by edgeinvest | Apr 24, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

MQ Trading Signals

Time

Signal

Duration

Type

2024-04-24 16:40:00

EMA 5

10 Mins

BUY

2024-04-24 16:40:00

TURTLE SYSTEM 20

10 Mins

BUY

2024-04-24 16:40:00

TURTLE SYSTEM 55

10 Mins

BUY

2024-04-24 16:15:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-04-24 16:15:00

TURTLE SYSTEM 55

5 Mins

SELL

Apps

Top Articles

2

3

save malaysia!

4

Koon Yew Yin's Blog

5

6

IPOWatcher

7

THE INVESTMENT APPROACH OF CALVIN TAN

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....