CEO Morning Brief

TM Climbs Over 6% After Earnings Beat Expectations

edgeinvest

Publish date: Thu, 25 Aug 2022, 08:52 AM

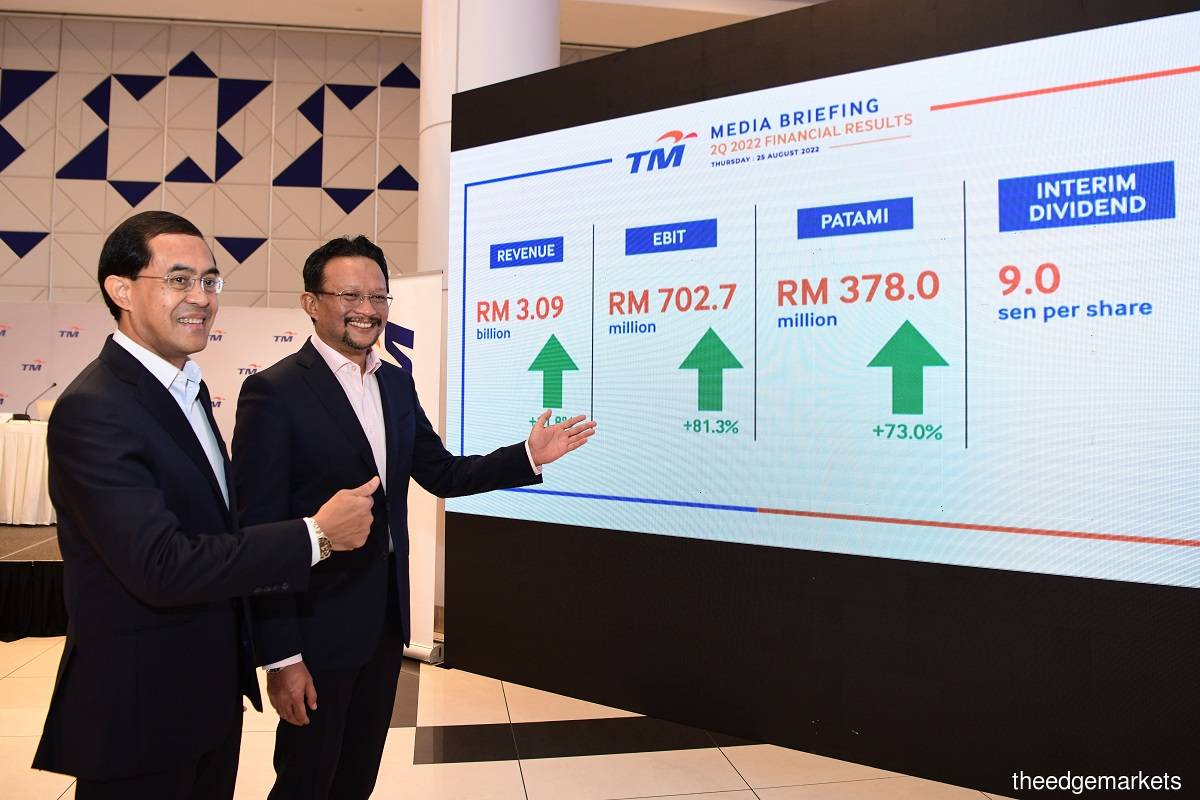

KUALA LUMPUR (Aug 25): The share price of Telekom Malaysia Bhd (TM) climbed more than 6% as the telco’s quarterly earnings beat analysts’ expectations.

On top of that, it declared an interim dividend of nine sen per share, accompanied by an applicable dividend reinvestment scheme.

At the market close, TM finished at RM5.95, up 30 sen or 5.31%, after it soared to a high of RM6.10 in the first hour of trading. Trading volume was at 9.42 million shares.

In a note on Thursday (Aug 25), CGS-CIMB Research analysts Foong Choong Chen and Sherman Lam Hsien Jin wrote that TM's second quarter ended June 30, 2022 (2QFY22) earnings exceeded the research house’s expectations, citing that key variances were the higher-than-expected revenue as well as the earning before interest, tax, depreciation and amortisation (EBITDA) margin.

“Total 2QFY22 revenue grew an encouraging 11.8% y-o-y (year-on-year), led by internet (+9.5%), voice (+6.7%), domestic wholesale (fibre leasing; +22.2%), higher indefeasible right of use (IRU) sales, and resumption of y-o-y growth at TM One (+4.1%; on more customer projects).

“2QFY22 EBITDA margin expanded 4.3% points y-o-y (+1.7% pts q-o-q) to a record 41.5% stemming from revenue growth, coupled with lower staff cost (most VSS (voice storage system) cost was already booked upfront in 1QFY22) and other costs,” it said.

Overall, CGS-CIMB noted that 1HFY22 results also beat its expectations, but the analysts maintain its earnings forecasts, target price (TP) and rating — “add” with a discounted cash flow-based (DCF) TP of RM6.75 — pending TM's press conference on the results on Thursday.

The telco’s net profit of RM378.06 million is the highest quarterly net profit since 4QFY11’s RM598.3 million. Earnings per share came to 10.02 sen from 2QFY21’s 5.79 sen.

The solid earnings came on the back of its revenue for the quarter growing 11.8% to RM3.09 billion from RM2.76 billion a year ago driven by higher contributions from all lines of services, particularly data and internet services.

For the cumulative period (1HFY22), TM's net profit rose 32% to RM717.91 million from RM544.06 million as cumulative revenue increased 7.34% to RM5.98 billion from RM5.57 billion.

Singing a similar tune, HLIB Research’s Tan J Young said 2QFY22’s net profit lifted 1HFY22’s net profit above the research firm’s expectations — accounting for 61% of its as well as the consensus full-year estimates.

“The outperformance was attributable to effective cost discipline which led to higher-than-expected EBITDA margin. 1HFY22 core earnings was arrived after adjusting for forex gain on international trade settlement (-RM58 million) and prosperity tax (+RM24 million),” Tan added.

The HLIB Research analyst also maintained a “buy” rating on the telco, but with a lower DCF-derived TP of RM6.94 — from RM7.23 previously.

Meanwhile, Kenanga analyst Ahmad Ramzani Ramli said TM's 1HFY22 results were within the research house’s expectations, noting that historically the telco’s first-half results are usually significantly stronger than results in the latter half of the year.

“Post results, we made no changes to our FY22 earnings [forecasts] with the company maintaining its guidance of: (i) low-to-mid single-digit growth, (ii) earnings before interest and tax of more than RM1.8 billion, and (iii) capex/revenue of 14% and 18% (1HFY22: 14%).

Ahmad reiterated an “outperform” rating on the telco, but with a higher TP of RM7.95 — as compared to RM6.90 — as he noted: “We rationalise our valuation basis to seven times FY23 EV/EBITDA (in line with the average historical forward EV/EBITDA of the broadband sector) from DCF basis.”

Source: TheEdge - 25 Aug 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on CEO Morning Brief

China Condemns US’ Overcapacity Claim Just Before Blinken Visit

Created by edgeinvest | Apr 24, 2024

Thailand to Replace Military-appointed Senate, Reduce Its Powers

Created by edgeinvest | Apr 24, 2024

Shadow Banking Stress in South Korea Sends Warning to Global Investors

Created by edgeinvest | Apr 24, 2024

Indonesia's Biggest Party Confirms President Jokowi No Longer a Member After Backing Prabowo

Created by edgeinvest | Apr 24, 2024

Telegram Founder Says China Downloads Have Not Fallen Since Apple Move

Created by edgeinvest | Apr 24, 2024

Indian Watchdog Said to Have Queried Global Funds Over Manipulation of Adani Stocks

Created by edgeinvest | Apr 24, 2024

China’s Surging Steel Exports Are Inflaming Global Trade Tensions

Created by edgeinvest | Apr 24, 2024

Bubble Tea Maker Chabaidao Slumps 38% in HK’s Biggest Debut This Year

Created by edgeinvest | Apr 24, 2024

Commodities Are a ‘win-win’ With US$100 Oil in Sight, Carlyle’s Currie Says

Created by edgeinvest | Apr 24, 2024

Japan Issues Strongest Warning Yet on Readiness to Intervene in Currency Market

Created by edgeinvest | Apr 24, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

MQ Trading Signals

Time

Signal

Duration

Type

2024-04-24 16:40:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-04-24 16:00:00

TURTLE SYSTEM 55

Hourly

BUY

2024-04-24 16:00:00

ADX

5 Mins

BUY

2024-04-24 15:50:00

TURTLE SYSTEM 20

5 Mins

BUY

2024-04-24 15:35:00

TURTLE SYSTEM 20

5 Mins

SELL

Apps

Top Articles

1

2

4

5

THE INVESTMENT APPROACH OF CALVIN TAN

6

7

save malaysia!

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....