CEO Morning Brief

Cover Story: Knocking Affin Bank Into Shape

edgeinvest

Publish date: Thu, 13 Oct 2022, 08:45 AM

WHEN Datuk Wan Razly Abdullah Wan Ali joined Affin Bank Bhd as its president and group CEO in April 2020, one of the biggest hurdles he faced was getting people to believe in his three-year plan to transform the country’s second-smallest of eight local banking groups into a stronger entity.

Staff were weary from past attempts at change, and analysts — the few that continued to keep the stock under their coverage — were sceptical about the lofty targets set under the so-called AIM22 plan.

It was also the early days of the Covid-19 pandemic and the country was in the midst of an unprecedented lockdown.

“The problem I had was getting people to believe in the plan. Those that didn’t, left us … from C-suites, middle management, down the whole chain,” recalls Wan Razly, speaking to The Edge in his first interview since taking the helm.

Candid and brimming with energy, he chats with us for more than two hours in a boardroom with a bird’s-eye view of the Kuala Lumpur skyline, in the 43-storey

Menara Affin@TRX. The spanking-new building at Tun Razak Exchange is soon to be the group’s new headquarters.

Wan Razly declines to disclose how many staff left, saying only: “The departures were regrettable, but we had to move on.” It was clear that tough and necessary changes were needed at the bank, and fast. The group, whose controlling shareholder is the Armed Forces Fund Board (LTAT), had a plethora of issues — high cost of funds, weak asset quality mainly from legacy loans, low loan loss coverage (LLC) and underperforming employees, among others — weighing on its performance even as the industry was moving ahead and getting increasingly competitive. Its digital initiatives lagged peers and it had the lowest return on equity (ROE) among the banks, at just 5.42%, in 2019.

Though considered the “jewel” of the LTAT group, Affin Bank clearly needed polishing.

As at August, LTAT and its subsidiary Boustead Holdings Bhd had a 33.33% and 20.99% stake respectively in Affin Bank, while Hong Kong-based Bank of East Asia Ltd held 23.86%.

Wan Razly and his team persevered with the plans under AIM22, which included a rebranding of Affin Bank. It was not just a logo change he sought, but also a change in culture — staff needed to be pushed out of their comfort zones. Stretch targets — or what he refers to as “aspirationally realistic” targets — were set.

Delivering results

These efforts are finally showing the desired results. Last year, the group’s profit before tax (PBT) rose 82% year on year to RM703.85 million, even as net profit grew 128.8% y-o-y to RM526.93 million — its highest in five years.

The performance puts it on course to reaching a key AIM22 target of RM1 billion in PBT in the year ending Dec 31, 2022 (FY2022), when the three-year plan concludes. This goal should be easily met, given the bank’s recent disposal of its 63%-owned subsidiary Affin Hwang Asset Management Bhd (AHAM) to CVC Capital Partners for RM1.42 billion, from which a divestment gain of RM1.063 billion will be reflected in 3QFY2022.

The disposal gives it a capital boost, with the group’s Common Equity Tier-1 (CET-1) ratio expected to rise to around 16% — well above the industry’s 15.1% — from 13.4% as at end-June.

As at 1HFY2022, Affin Bank managed to bring down its cost of funds substantially to 1.97% compared with 3.24% two years earlier. This was done by restructuring its balance sheet and growing CASA (current accounts and savings accounts) — a relatively cheaper source of funds — much more aggressively. CASA made up 21% of its total deposits compared with 13.9% in 2QFY2019.

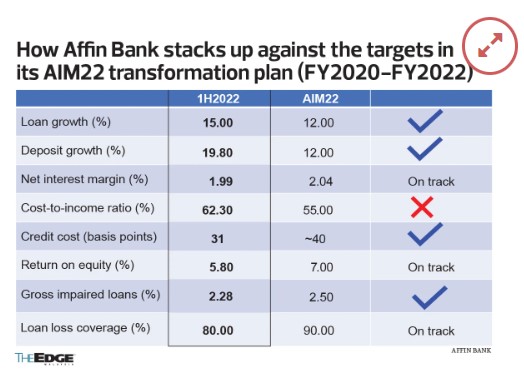

By bringing down its cost of funds, the group’s net interest margin (NIM) expanded from 1.49% in FY2019 to 1.99% in 1HFY2022. Wan Razly believes the bank is on track to meeting its 2.04% target by year’s end.

Its gross impaired loans (GIL) ratio — an indicator of asset quality — improved to 2.28% in 1HFY2022 from 3% in FY2019.

“Our GIL ratio was elevated during Covid-19 — at 3.52% in 4Q2020 — and we were one of the worst in the market. The [problem] was mainly in the corporate banking segment. But we’ve managed to bring the ratio down and strive to go under 2%, which will put us more in line with our peers in the market,” Wan Razly says.

“People asked us how we did it — was it through manipulation of numbers? If you look at it, we had RM1.63 billion of impaired loans in 4Q2020 and, today, we have RM1.26 billion. We worked hard and recovered almost RM370 million in the past two years. This is how we did it.”

Notably, Affin Bank steadily built up its LLC ratio, which was very low at 43.8% in FY2019 — a point of discomfort for analysts — to 80% as at 1HFY2022. Nevertheless, it is still below the industry average of 100%.

“We are on track with a plan to get to 100% by next year — if not earlier, if we take special provision overlays, which will put us in line with the market. We’ve made pre-emptive provisions of more than RM300 million over the course of Covid-19, and we will continue to build [such provisions],” says Wan Razly.

The only hard miss so far on Affin Bank’s AIM22 targets is on the cost-to-income ratio front. CIR, an indicator of operational efficiency, stood at 62.3% as at end-June — a long shot from its 55% target because of slower fee income — and is among the highest in the sector. This remains a work in progress, says Wan Razly.

What gives him great satisfaction is that people’s perception of Affin Bank has vastly improved — as indicated by the bank’s net promoter score (which measures customer experience) of +39 as at June this year compared with +27 in 2021 and the current industry average of 41 — and employees are a lot more motivated.

“We have 5,300 people [employed] in the bank today. We haven’t really increased the workforce, just added a few key hires here and there. We rallied the team, gave them the confidence that they could do it. Today, it’s a very energised and confident team that we have — drastically different from where we were almost three years ago,” he remarks.

“We’ve had so many stumbling blocks, but every problem we came across, we tackled. There’ll be other things to fix, to make better. But I am reassured that the results are coming in, the team is delivering the numbers. We haven’t got full marks for AIM22, but we’re more than a ‘pass’ — we’re somewhere between a ‘more than pass’ and an ‘A’. But what it proves to us is that we can achieve aspirational [targets].”

Investors, taking note of Affin Bank’s progress and attracted by the possibility of a special dividend after the AHAM sale, have driven the shares up 23.2% so far this year — making it one of the top gainers among the banks — to RM2.01 as at Sept 29, giving the lender a market capitalisation of RM4.45 billion. Kenanga Research listed Affin Bank as one of its top sector picks for the third quarter.

Digital is key in next three-year plan

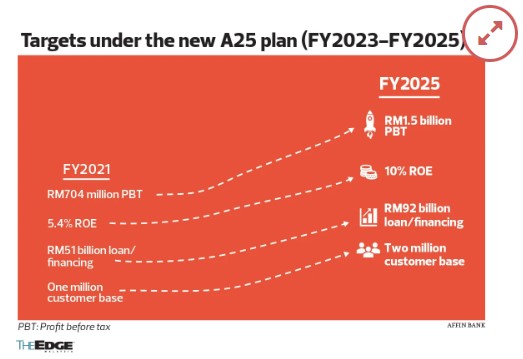

Now that it is on a firmer footing, the bank is embarking on the second phase of its transformation plan. It has laid out equally ambitious growth targets for the next three years (FY2023 to FY2025) under a new plan known as A25.

“Phase 2 is where we strive to become a modern and progressive group, which means we need to enhance a lot of the digital stuff that we didn’t have in the past. We want to get our mobile [banking] platform up, we want a new and enhanced CRM [customer relationship management] system so that we know our customers better and are able to cross-sell to them,” Wan Razly says.

It now aims for PBT to reach RM1.5 billion by end-FY2025 (from RM704 million in FY2021); ROE to double to 10% (from 5.4%); loans/financing to almost double to RM92 billion (from RM51 billion); and its customer base to double to two million. Other targets include having the GIL ratio improve further to 1.5% and the CIR to come in below 53%.

It plans to launch its mobile banking app this month and refresh its internet banking portal later this year. Last November, it rolled out a simple digital bank proposition known as A1addin — a mobile app — which it hopes to build on further for the digital-savvy generation.

Affin Bank is noticeably late in the digital game compared with other banks. Wan Razly says: “Yes, we’re a bit late, but we are getting there at a rapid rate. Once our mobile banking app goes live, it will support our CASA initiatives. The more CASA we have, the stronger this bank will become.

“Everything we’re doing today is trying to build the bank to the scale it should be. Some people say we are growing aggressively, [but] I say we are growing at a scale that we should have been.”

Interestingly, while most banks hope to reduce the number of their physical branches as they go increasingly digital, Affin Bank has no plans to do so. It believes in a hybrid model where branches will remain a key means by which customers interact with the bank, along with other channels and platforms. It has 115 branches — five more than in 2020 — which it plans to maintain, or add to slightly, in the coming years.

Many are wondering how Affin Bank will make up for the loss of earnings contribution from AHAM, from August. That business accounted for a sizeable 16.8%, or RM68.8 million, of the group’s PBT of RM408.51 million in 1HFY2022.

“AHAM was making about RM77 million a year. [With the RM1 billion-odd gain on divestment, which will be reinvested into the group,] we can double this to RM140 million to RM150 million over the course of two years,” Wan Razly estimates.

He indicates that its Islamic banking business, Affin Islamic Bank Bhd, which has grown significantly since FY2021 and emerged as a major earnings contributor to the group, will play a big part in filling the gap. He also sees the investment banking business, Affin Hwang Investment Bank Bhd (AHIB), weighing in more.

“We have our plans, and I don’t want to give away too much, but I do feel they can do a lot better — twice better at least from where they are today,” he says of AHIB.

AHIB accounted for 7.6%, or RM31 million, of the group’s PBT in 1HFY2022, while Affin Islamic was the biggest contributor (36.2%, or RM147.9 million), followed by the main bank (31.9%, or RM130.2 million).

New CEOs for two subsidiaries

Both Affin Islamic and AHIB are currently without a CEO. The Islamic bank CEO Nazlee Khalifah retired at end-May, while AHIB CEO Mona Suraya Kamaruddin — formerly Nomura Holding Inc’s head of Malaysia — retired at the end of last month after just two years on the job.

Industry sources tell The Edge that Datuk Syed Mashafuddin Syed Badaruddin, the CEO of Principal Islamic Asset Management Sdn Bhd who is understood to have recently submitted his resignation, will soon be joining the group to helm Affin Islamic. Bank Negara Malaysia is understood to have green-lit the pending appointment.

Wan Razly, however, declines to comment. Affin Islamic is growing fast — its PBT jumped 156% y-o-y to RM248.5 million in FY2021 and is estimated to expand a further 41% to RM350 million this year, he says.

As a group, Affin Bank has been growing loans at a significantly faster pace than the industry. Loans grew a blistering 15% y-o-y in 2QFY2022 but, for the full year, it is sticking to its projection of 12% growth — about double what most banks expect — as higher interest rates crimp loan demand.

“People are thinking twice about whether to take loans, given the [higher] cost of the borrowing. But we still have a heavy pipeline of business and that will run us [through] a few quarters of growth,” Wan Razly says. It will concentrate on growing retail and small and medium enterprise (SME) loans, the bank’s two pillars of focus. “For corporates, we’ll be selective. If it fits our [risk] appetite, then we’ll do a corporate deal.”

Of the local banks, Affin Bank stands to benefit the least from a rising interest rate environment, as it has one of the lowest proportions of floating-rate loans. Such loans accounted for 75% of its total loans as at end-June. Bank Negara Malaysia has raised the overnight policy rate three times so far this year by a total of 75 basis points.

“There’s going to be a lot of pressure on our margins, which is why it is important that we work on growing our CASA. We also want more floating-rate loans — we’ll soon be offering floating-rate hire purchase (HP) loans as part of our product innovation,” he says.

HP accounted for RM12.16 billion of the group’s RM55.43 billion loan book as at end-June, with housing loans making up RM15.3 billion.

Meanwhile, loans under repayment assistance have now declined to 5.9%, or RM3.25 billion, of its total portfolio compared with 6.92%, or RM3.75 billion, in April, Wan Razly says. “It has been a slow process of recovery, especially [for corporates].”

On the sustainability front, the group is aiming for 4% of its total financing to be ESG (environmental, social and governance)- friendly by year’s end, from 1.8% as at end-June. The target for 2025 is 10%.

Headwinds ahead

Despite its remarkable progress thus far, analysts and industry observers believe there is still a long way to go in Affin Bank’s transformation. It is still a work in progress and needs to show that it can keep up its positive momentum amid growing headwinds, not least of which is the rising risk of a global recession next year.

Wan Razly himself speaks of “dark clouds” coming.

What is clear is that he has put the building blocks in place and the bank is moving in the right direction.

“While it may take some time [for Affin Bank] to stand on a similar footing [with] its peers, it certainly seems to be moving in the right direction,” says MIDF Research.

Source: TheEdge - 13 Oct 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on CEO Morning Brief

Flooded UAE Counts Cost of Epic Rainstorm, Dubai Airport Still Facing Disruptions

Created by edgeinvest | Apr 19, 2024

UBS Shuts Some China Private Funds, Will Lay Off Staff, Sources Say

Created by edgeinvest | Apr 19, 2024

Japan Firms' Business Mood Slips as Weak Yen Squeezes Households

Created by edgeinvest | Apr 19, 2024

Bank of Japan's Noguchi Says Future Rate Hikes Likely to be Slow

Created by edgeinvest | Apr 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

MQ Trading Signals

Time

Signal

Duration

Type

2024-04-19 16:50:00

EMA 5

5 Mins

SELL

2024-04-19 16:50:00

ADX

5 Mins

SELL

2024-04-19 15:55:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-04-19 15:50:00

TURTLE SYSTEM 20

10 Mins

BUY

2024-04-19 15:50:00

TURTLE SYSTEM 20

5 Mins

BUY

Apps

Top Articles

2

3

4

Koon Yew Yin's Blog

5

Good Articles to Share

Slower US Fed pivot weakens rate-cut bets across emerging Asia

6

7

Good Articles to Share

8

Good Articles to Share

Bank of America CEO talks earnings, consumer spending, and inflation

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....