CEO Morning Brief

YTL Power Hits New Record High as YTL-linked Counters Extend Gains

edgeinvest

Publish date: Tue, 30 May 2023, 08:37 AM

KUALA LUMPUR (May 29): Shares in YTL Power International Bhd closed at a new record high on Monday (May 29), while parent company YTL Corp Bhd also jumped, following analysts’ rerating of the counter as its latest earnings beat expectations.

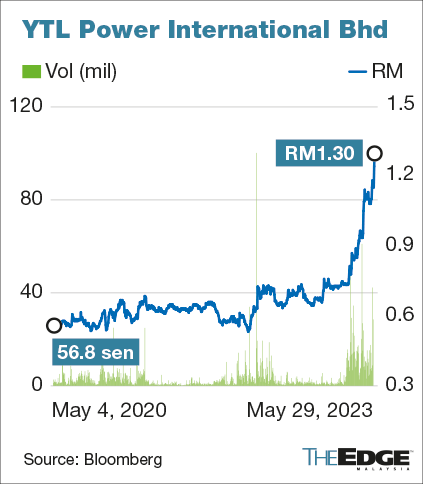

YTL Power closed up six sen or 4.84% at RM1.30, Bloomberg data showed. It touched an intraday high of RM1.34, with trading volume more than triple its two-month average to 38.98 million shares.

The counter's previous high was recorded on Dec 31, 2010, when it closed at RM1.24 per share.

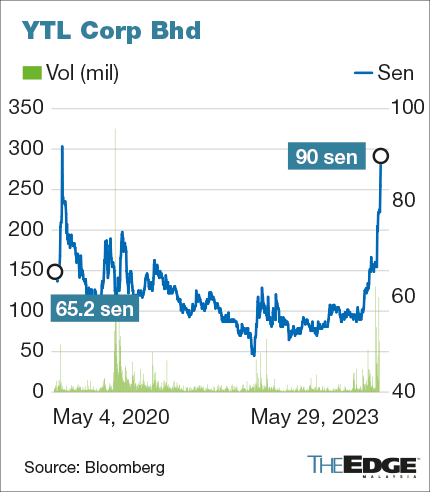

Meanwhile, shares in its 56%-parent YTL Corp closed at their intraday and three-year high of 90 sen, up 6.5 sen or 7.78%. Trading volume surged to 74.98 million shares, more than four times its two-month average.

Both counters have been rising steadily through March this year, with YTL Corp’s share price up 55%, tracking YTL Power’s 81% rise as investors took their cue from improved energy sales volume and prices in its Singapore operations.

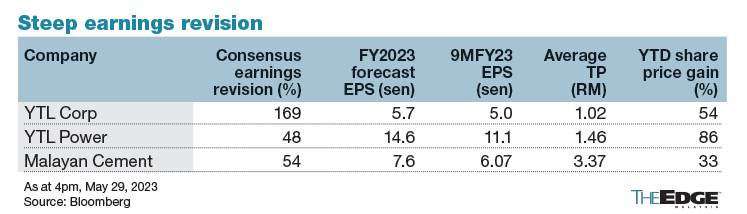

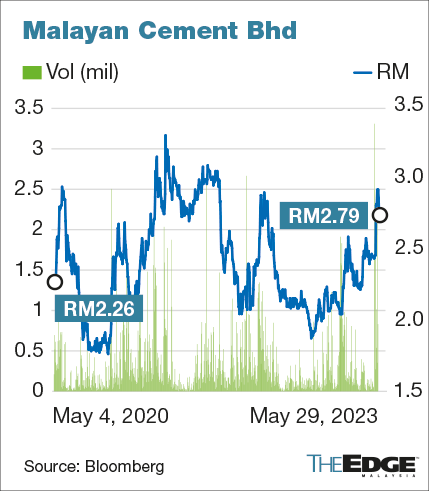

Another YTL-linked counter, Malayan Cement Bhd, which is 76%-owned by YTL Corp, rose as much as nine sen before settling four sen or 1.45% higher at RM2.79.

Shares in the cement manufacturer — which YTL Corp bought into in 2021 — have climbed 33% this year, as it posted its strongest earnings since 2015 and record quarterly revenue due to improved demand, which supported prices and eased some cost pressures.

The recovery in the YTL-linked counters followed a few years of underperformance, in the absence of new mega construction projects, and dragged by shrinking power generation operations as well as the highly competitive telco business in Malaysia.

Sentiment was also supported by the recent lifting of the renewable energy (RE) export ban by the Malaysian government, with YTL Power having a footprint in both the power generation and power retail businesses in RE-hungry Singapore.

YTL Corp also has international operations, investments and projects under development in countries including Singapore, the UK, Australia, France, Indonesia, Japan, Jordan, Myanmar, the Netherlands, Thailand and Vietnam.

Strong recovery from FY2023, say analysts

“YTL Corp’s latest set of results underpin our thesis of a strong earnings recovery from FY2023 (the financial year ending June 30, 2023),” said MIDF Research analyst Hafriz Hezry in a report on YTL Corp dated May 26.

MIDF increased its target price (TP) for YTL Corp to RM1.05 from 83 sen previously, on the improved performance of YTL Power and Malayan Cement, coupled with the economic reopening theme for the hotel division.

Including MIDF’s revised forecast, consensus earnings per share (EPS) for YTL Corp for FY2023 have been revised higher by 169% to 5.7 sen, according to two analysts' coverage tracked by Bloomberg.

Meanwhile, YTL Power, which has screaming "buy" calls from all 10 analysts covering the counter, saw consensus EPS revised 48.28% higher to 14.6 sen, following the third-quarter results announcement, with an average TP of RM1.46.

On YTL Power, Hafriz said in a separate note that the utility firm’s latest Singapore acquisition — the 396MW Tuaspring plant — effectively increased the generation capacity of its Singapore unit YTL PowerSeraya Pte Ltd by 16%.

“In the short term, we expect the weaker ringgit against the Singapore dollar to also artificially lift earnings contributions from Seraya,” he said.

Analysts are also expecting a recovery in the water business in the UK after a tariff revision that will be reflected in the coming quarter, coupled with the start-up of another 45%-owned, 554MW shale-fired power plant in Jordan.

Separately, consensus FY2023 EPS for Malayan Cement were also raised by 54.04% to 7.6 sen. The cement producer has four "buy" calls against two "hold" calls, with an average TP of RM3.37.

“We anticipate a stabilised earnings profile, even though average selling prices have peaked, with much lower volatility on the input costs front,” said HLIB Research analyst Edwin Woo in a note dated May 26. HLIB has a “hold” call at RM2.78 on the counter, in view that the upside has been priced in following the rally this year.

Read also:

YTL Power’s 3Q net profit drops 49% due to absence of gain on investment disposal; declares 2.5 sen dividend

YTL Corp posts flat 3Q net profit

Source: TheEdge - 30 May 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on CEO Morning Brief

China Condemns US’ Overcapacity Claim Just Before Blinken Visit

Created by edgeinvest | Apr 24, 2024

Thailand to Replace Military-appointed Senate, Reduce Its Powers

Created by edgeinvest | Apr 24, 2024

Shadow Banking Stress in South Korea Sends Warning to Global Investors

Created by edgeinvest | Apr 24, 2024

Indonesia's Biggest Party Confirms President Jokowi No Longer a Member After Backing Prabowo

Created by edgeinvest | Apr 24, 2024

Telegram Founder Says China Downloads Have Not Fallen Since Apple Move

Created by edgeinvest | Apr 24, 2024

Indian Watchdog Said to Have Queried Global Funds Over Manipulation of Adani Stocks

Created by edgeinvest | Apr 24, 2024

China’s Surging Steel Exports Are Inflaming Global Trade Tensions

Created by edgeinvest | Apr 24, 2024

Bubble Tea Maker Chabaidao Slumps 38% in HK’s Biggest Debut This Year

Created by edgeinvest | Apr 24, 2024

Commodities Are a ‘win-win’ With US$100 Oil in Sight, Carlyle’s Currie Says

Created by edgeinvest | Apr 24, 2024

Japan Issues Strongest Warning Yet on Readiness to Intervene in Currency Market

Created by edgeinvest | Apr 24, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

One App To Trade Malaysia & US Stock With 0* Commission

MQ Trading Signals

Time

Signal

Duration

Type

2024-04-24 16:30:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-04-24 16:30:00

TURTLE SYSTEM 55

5 Mins

SELL

2024-04-24 16:05:00

TURTLE SYSTEM 20

5 Mins

BUY

2024-04-24 16:05:00

TURTLE SYSTEM 55

5 Mins

BUY

2024-04-24 16:00:00

TURTLE SYSTEM 20

10 Mins

BUY

Apps

Top Articles

1

2

4

5

THE INVESTMENT APPROACH OF CALVIN TAN

6

7

save malaysia!

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....