Koon Yew Yin's Blog

Why I Bought into Hengyuan - Koon Yew Yin

Koon Yew Yin

Publish date: Fri, 28 Jul 2017, 10:58 AM

Koon Yew Yin

0 1,414

An official blog in i3investor to publish sharing by Mr. Koon Yew Yin.

All materials published here are prepared by Mr. Koon Yew Yin

All materials published here are prepared by Mr. Koon Yew Yin

I see there are so many people writing articles and commentaries in i3investor on Hengyuan. Even during last week end, Mr Ooi Teik Bee with 4 of his friends who are also his clients came from KL to my house in Ipoh. He strongly recommended me to buy Hengyuan.

But he was pleasantly surprised that I told him that I started buying as soon as I saw that the company has been producing increasing profit in the last 2 quarters which were 69.27 sen EPS for quarter ending Dec 2016 and 93.14 sen for quarter ending March 2017, totalling 162.41 sen. Based on the result of the last 2 quarters, its annual profit will be about Rm 3.25 EPS. That is why so many investors are chasing to buy it because it is selling at P/E 2.

Where can you find such a good stock selling at such low P/E?

It complies with my share selection golden rule which has a long proven track record.

Based on my golden rule, I have bought so much shares of Latitude Tree, Lii Hen, VS Industry, Eversendai and JAKS and became the second largest shareholders of each of the companies. The share price of each of these companies has gone up several hundred per cent with 3 years. If you look at the price charts of Latitude and Lii Hen, you will see that each of them has gone up more than 800 per cent and VS has gone up more than 550 per cent. Eversendai and JAKS has gone up about 50 per cent in the last few months. They will continue to go higher when they continue to show increasing profit.

Fundamental Business Factors that would affect profit:

During my last 60 years in doing business, I must examine all the factors that affect the bottom line. In the case of refining petroleum, the profit depends on the crude oil price in the open market, refining cost and the selling price of the refined oil. There is an oversupply of crude oil in the world and this situation will continue for a long time to come. Hengyuan is currently sells most of its product to Shell Stations and the pump price is controlled by the Government which is always high to protect Petronas.

Moreover, Hengyuan can sell its product to its own petrol stations in China. This does not sound right but if you examine it closely you will understand what I said. China buys most of its crude oil from the Middle East and ship it to China. The ships have to travel and past Port Dickson, the location of Hengyuan’s refinery on the way to China. Whether Hengyuan refines its crude oil in China or in Port Dickson makes very little difference because the refining process cost is very small in comparison with the selling price.

Currently the local demand for refined oil is more than supply until the completion of the new refinery in about 2 years.

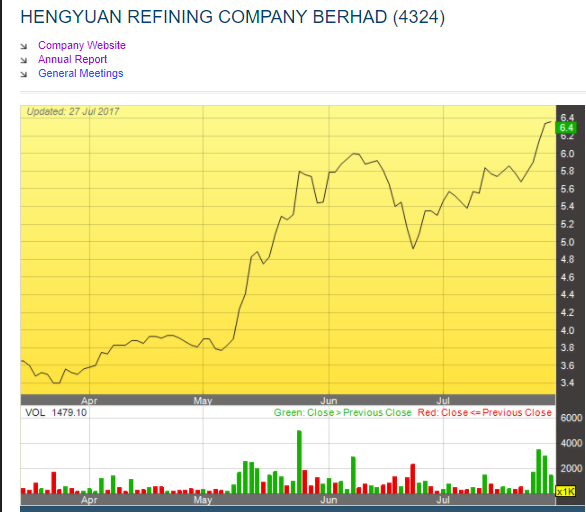

The price chart shows Hengyuan’s share price is on an uptrend which is a buy signal according the expert chartists.

Mr Ooi Teik Bee’s recommendation:

If you are a subscriber, you should have received Mr Ooi Teik Bee’s recommendation of Hengyuan with a target price of Rm 15.93.

I am obliged to tell you that I have quite a lot of Hengyuan and I am not asking you to buy it. But if you decide to buy it, you are doing at your own risk.

As much as I am reluctant to post this piece on i3investor to avoid seeing some stupid commentaries, Mr Ooi Teik Bee asked me to post it to teach people how to make more money.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Koon Yew Yin's Blog

Eversendai Corporation made a remarkable comeback in FY2023 - Koon Yew Yin

Created by Koon Yew Yin | Apr 22, 2024

Eversendai Corporation Berhad made a remarkable comeback in FY2023, reporting strong profit growth. Here are the key highlights from their financial performance:

Sendai price trend reversal - Koon Yew Yin

Created by Koon Yew Yin | Apr 22, 2024

Sendai price chart below is showing its price trend reversal. It is hitting a record high.

How can KSL double its profit? - Koon Yew Yin

Created by Koon Yew Yin | Apr 18, 2024

After the stock closed yesterday, KSL announced its 4th quarter EPS which is 40.76 sen and its net tangible asset (NTA) backing of Rm 3.65. Its profit increased by 230% more than last year.

Why Sabah will leave Malaysia - Koon Yew Yin

Created by Koon Yew Yin | Mar 29, 2024

Currently Sabah Government does not know that solar panel produces the cheapest electricity???

Malaysia can be one of the richest nations in the world - Koon Yew Yin

Created by Koon Yew Yin | Mar 23, 2024

During my life time I saw every Prime Minister being replaced by another politician for one reason or another. Dr Mahathir managed to stay the longest time of 22 years.

Property Developers comparison - Koon Yew Yin

Created by Koon Yew Yin | Mar 04, 2024

All property developers have just announced their annual profit for 2023. All of them reported increased profit.

My contribution as an Engineer - Koon Yew Yin

Created by Koon Yew Yin | Mar 04, 2024

Although my writing of this article sounds boastful but I feel that it is important to keep this record for posterity. Engineers play a pivotal role in shaping our modern world.

What can KSL can do to benefit shareholder? - Koon Yew Yin

Created by Koon Yew Yin | Mar 01, 2024

What can KSL do to benefit shareholders? I hope all the shareholders will read this article so that they can attend the coming annual general meeting to vote out those directors who are seeking re...

All Investors require Anticipation - Koon Yew Yin

Created by Koon Yew Yin | Feb 29, 2024

After the stock market closed, KSL announced its 4th quarter ending Dec 2023 EPS of 12.74 sen. The total is 40.76 sen for 4 quarters. Its total EPS for 4 quarter ending 2020 was only 17.8 sen.

Property developers share prices comparison based on latest EPS - Koon Yew Yin

Created by Koon Yew Yin | Feb 29, 2024

KSL is the cheapest in terms of PE ratio. KSL Holdings Bhd is a holding company. It is engaged in real estate services.

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

MQ Trading Signals

Time

Signal

Duration

Type

2024-04-25 16:40:00

TURTLE SYSTEM 20

10 Mins

SELL

2024-04-25 16:40:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-04-25 16:35:00

TURTLE SYSTEM 20

5 Mins

BUY

2024-04-25 16:30:00

TURTLE SYSTEM 20

10 Mins

BUY

2024-04-25 16:20:00

EMA 5

10 Mins

BUY

Apps

Top Articles

1

Good Articles to Share

Malaysia in Talks With Tycoons on Casino to Revive $100 Billion Forest City

2

3

4

5

THE INVESTMENT APPROACH OF CALVIN TAN

7

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....