THE INVESTMENT APPROACH OF CALVIN TAN

Kim Loong Resources eyes record year amid high CPO prices (The Lessons Revealed From Edgedaily Interview with KM Loong, Comments by Calvin Tan

calvintaneng

Publish date: Sat, 28 Aug 2021, 12:43 PM

calvintaneng

0 1,788

Hi Guys,

I have An Investment Approach I which I would like to all.

I have An Investment Approach I which I would like to all.

This article first appeared in The Edge Malaysia Weekly, on July 5, 2021 - July 11, 2021.

AFTER reporting its third-highest profit of RM94.89 million for the financial year ended Jan 31, 2021 (FY2021), Johor-based planter Kim Loong Resources Bhd is confident of delivering another year of strong performance in FY2022, riding on the commodity boom and high crude palm oil (CPO) prices, which have risen 59% from a year ago.

The group’s highest profit was RM96.57 million in FY2012, followed by RM96.54 million in the FY2018.

“Looking at the current external environment factors, it is really a perfect storm for the vegetable oil market,” Kim Loong managing director and major shareholder Gooi Seong Heen tells The Edge in a phone interview.

According to him, the Covid-19 pandemic hampered the CPO market in the first half of 2020, as people stopped dining out. As demand recovered, coupled with supply shortage, CPO prices started to rise since last July.

“First, there was tighter supply and higher demand for palm oil. Then, sunflowers and soybeans were hit by bad weather. And now that US President Joe Biden is pushing the green agenda, there is soaring demand for biodiesel that uses soybean oil,” he explains.

Gooi, 70, was appointed the group’s executive director in 1990, before he was redesignated to his current position in 2006.

Even with decades of experience in the plantation business, he has never seen a commodity boom quite like this, where CPO prices have reached almost RM5,000 per tonne.

“Previously, the highest we had seen was RM4,000 per tonne, but RM5,000 per tonne was just beyond our imagination,” he remarks.

According to data from the Malaysia Palm Oil Board, the spot price for CPO hit RM4,773 per tonne in May.

Gooi believes that in the next 12 to 18 months, CPO prices are likely to remain quite strong. As long as they hold above the RM3,000 level, plantation companies such as Kim Loong should continue to do well.

The potential risk, however, is that demand for CPO might be affected if the US and Indonesia change their biodiesel policies. On the other hand, he says if bad weather recurs in the US, CPO prices may revisit the RM5,000 level.

“It is a very uncertain market for the seed oil players, as it has always been throughout the years. But, as far as we are concerned, the RM3,000 level is just nice for us. We hope CPO prices do not shoot up to a super-high level because it might kill the market.”

Gooi points out that, so far, the growers have not seen much improvement in palm oil production, as the industry still faces a labour shortage.

“For us, the labour shortage at our estates in Sabah is not too serious, but more so for our estates in Sarawak. We have to improve productivity since we are not allowed to recruit new workers. Overall, we are suffering crop losses of 10% to 20%,” he says.

Kim Loong is 63.72%-controlled by Sharikat Kim Loong Sdn Bhd, the private vehicle of the Gooi brothers.

Gooi’s elder brother Seong Lim is executive chairman of Kim Loong, and his two younger brothers Seong Chneh and Seong Gum also sit on the board as executive directors.

It is worth noting that Seong Lim, who shares his fortune with his three younger brothers, is ranked by Forbes magazine as Malaysia’s 48th richest man, with a net worth of US$340 million (RM1.4 billion).

The Gooi family also controls Crescendo Corp Bhd, a Main Market-listed property and construction firm with a market capitalisation of RM336.56 million.

Shunned by investors

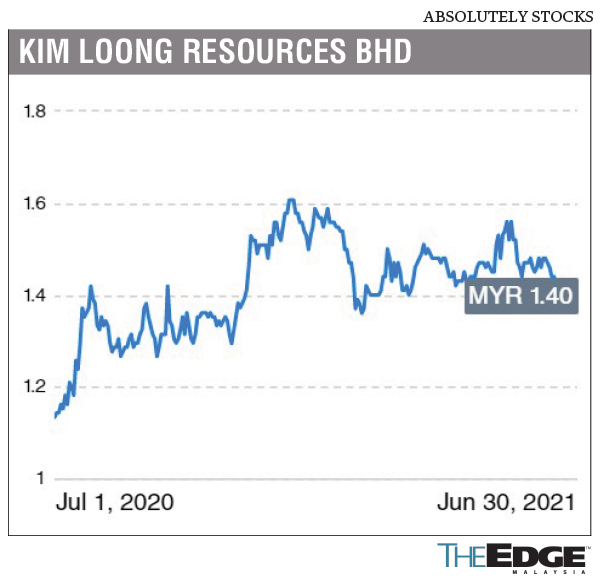

So far this year, shares in Kim Loong have declined 11% to close at RM1.40 last Wednesday, giving it a market capitalisation of RM1.31 billion.

Suffice it to say, Kim Loong and its plantation peers have not been favoured by investors in recent years, owing to investors’ focus on environmental, social and governance (ESG) issues.

Furthermore, Gooi believes investors remain sceptical probably because they have never seen CPO prices approaching the RM5,000 level.

“Over the years, every time the CPO price reached the RM3,000 level, it would crash back to the RM2,000 level. I suppose this could be a psychological barrier for investors.”

He also acknowledges that green lobby groups have been targeting the palm oil industry and have created negative perception on plantation companies.

“We do what we can. We comply with all the requirements. We obtained the MSPO (Malaysian Sustainable Palm Oil) certification. Some companies even go all the way to the RSPO (Roundtable on Sustainable Palm Oil), which involves a lot of work and documentation. If they (the green lobby groups) still don’t accept that, there is nothing much we can do, is there?”

Gooi adds that, today, even big plantation companies with RSPO certification have problems selling to Europe. “This is the current situation that we are in. Plantation companies will continue to focus on the China and India markets, not so much on the US and Europe.”

Fortunately, he says, Kim Loong has little exposure to foreign markets, as it sells most of its fresh fruit bunches (FFB) locally.

“Frankly, businesswise, there is not much impact on us. But, obviously, not many investors are looking at plantation stocks now. As it is, I guess you can only invest for dividends. The capital appreciation may not come so soon because we are not a favoured counter at the moment,” Gooi says.

He concedes that despite Kim Loong’s strong earnings performance, there are still a lot of issues to be resolved that are largely beyond his control now.

“To be honest, we do not know how to solve these issues. We will just focus on our business. We will try to be as efficient as possible. Comparatively, in terms of efficiency, we are among the top in the industry,” he points out.

Gooi says that, compared with bigger plantation companies — some of which command price-earnings ratios (PERs) of 30 times — Kim Loong, which is trading at a PER of 14 times, has been undervalued.

“Some investors would rather invest in loss-making companies or technology companies that are trading at high PERs; the stock market doesn’t quite make sense. We can only focus on generating profits and paying dividends. In fact, we have been paying up almost all our profits as dividends,” he stresses.

Limited room for growth

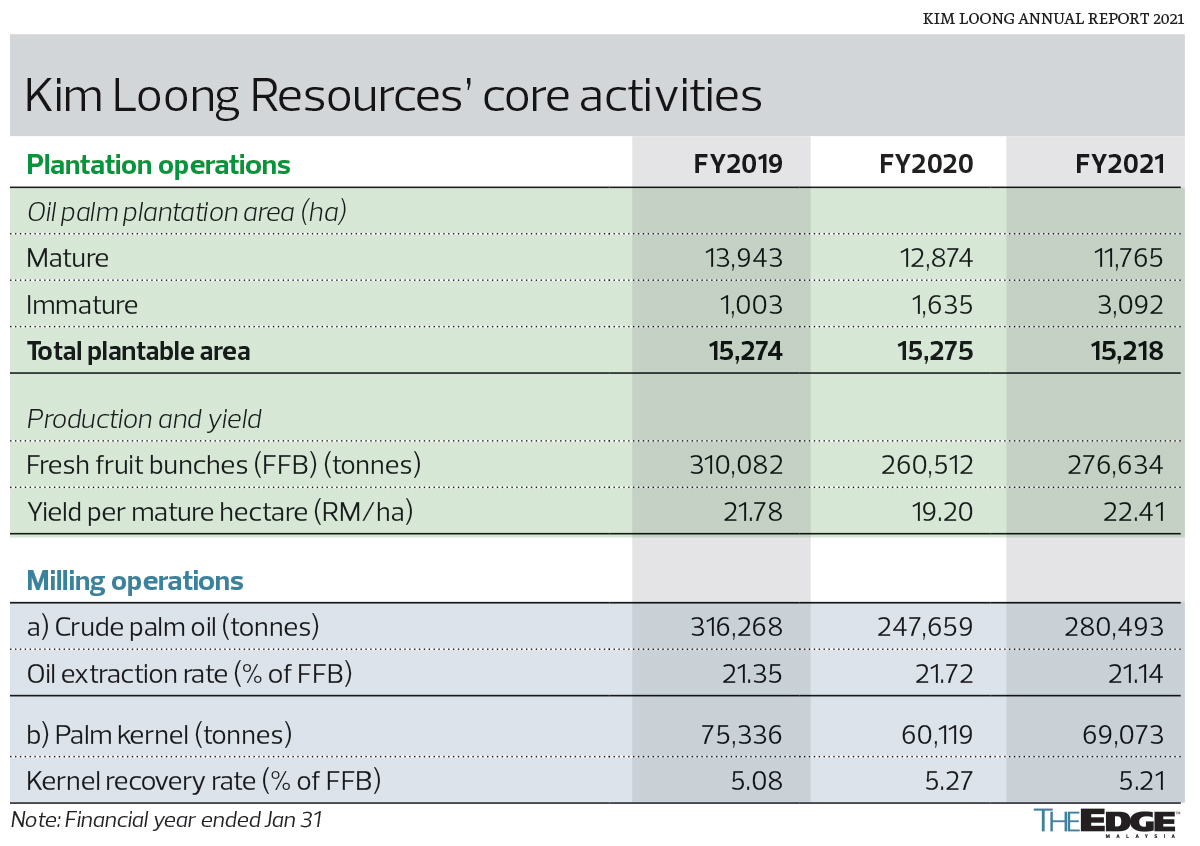

Kim Loong owns eight estates in Johor, Sabah and Sarawak, with a total plantable area of more than 15,000ha. Gooi accepts the reality that the group will not be able to grow and expand in the near future.

“The Malaysian government has put a limit on new planting; we can’t plant on jungle land. So, that’s the end of the story. Meanwhile, Indonesia also has a moratorium on the expansion of new plantation areas. Realistically, there is no more land for us to expand. It will be very expensive to buy a brownfield estate. We recently bought an additional 2,700ha estate near Sandakan, so, that’s about all we can do now,” he says.

Kim Loong also operates three mills — two in Sabah and one in Kota Tinggi, Johor — with a total processing capacity of 250 tonnes of FFB per hour.

Over the past few years, the milling operations have been contributing 60% of the group’s profits, with the remaining 40% coming from its plantation operations.

“With the high CPO price, we had seen a rather significant shift in our sales mix, whereby the plantation division accounted for 60% of our group’s profit instead,” says Gooi.

He adds that the plantation division’s profit contribution to the group is expected to increase to 70%.

“Our mills are mainly for commercial use. In other words, we source our raw materials from other plantation companies, not from our own estates. Therefore, higher CPO price actually means higher cost for our milling operations.”

Calvin comments:

This single phone interview has given us a clear picture of the Palm Oil business. A Real Revelation indeed!

Let's go into the details (comments are in brackets)

1) Kim Loong Resources Bhd is confident of delivering another year of strong performance in FY2022, riding on the commodity boom and high crude palm oil (CPO) prices, which have risen 59% from a year ago.

(Kim Loong Resources sounds very confident of the future)

2) The group’s highest profit was RM96.57 million in FY2012, followed by RM96.54 million in the FY2018.

(Year 2012 was commodity boom year as KMloong did well was expected. Year 2018? More due to its milling business)

3) Even with decades of experience in the plantation business, he has never seen a commodity boom quite like this, where CPO prices have reached almost RM5,000 per tonne.

“Previously, the highest we had seen was RM4,000 per tonne, but RM5,000 per tonne was just beyond our imagination,” he remarks.

(Even with decades of experience the CPO prices reaching RM5,000 per ton caught them by surprise)

4) “First, there was tighter supply and higher demand for palm oil. Then, sunflowers and soybeans were hit by bad weather. And now that US President Joe Biden is pushing the green agenda, there is soaring demand for biodiesel that uses soybean oil,” he explains.

(Reasons for high Cpo prices were given above.)

5) Gooi believes that in the next 12 to 18 months, CPO prices are likely to remain quite strong. As long as they hold above the RM3,000 level, plantation companies such as Kim Loong should continue to do well.

But, as far as we are concerned, the RM3,000 level is just nice for us.

(KMloong is so sanguine that Cpo prices will hold above Rm3,000 till end 2022. Cpo at above Rm3,000 a ton already good enough for KMLoong)

6) Furthermore, Gooi believes investors remain sceptical probably because they have never seen CPO prices approaching the RM5,000 level.

“Over the years, every time the CPO price reached the RM3,000 level, it would crash back to the RM2,000 level. I suppose this could be a psychological barrier for investors.”

(Due to past years of sudden cyclical upturn then followed by swift downturn people are still skeptical that prices of Cpo will remain high for long)

(NOTE: CALVIN THINKS THERE IS NOW A FUNDAMENTAL STRUCTURAL SHIFT

1) DUE TO CLIMATE CHANGE USA IS GOING BIG TIME INTO BIIODISEL WHICH WILL INCREASE DEMAND FOR SOYBEAN: THUS PUSHING UP PALM OIL PRICES)

IN YEAR 1973 ARAB OIL EMBARGO & ITS SUBSEQUENT MIDDLE EAST OIL BOOM PUSHED UP OIL PRICES TO ELEVATED LEVEL: NO LONGER CHEAP CRUDE OIL

BY THE SAME TOKEN THERE MAY NO LONGER BE CHEAP PALM OIL PRICES LIKE BEFORE)

7) He also acknowledges that green lobby groups have been targeting the palm oil industry and have created negative perception on plantation companies.

“We do what we can. We comply with all the requirements. We obtained the MSPO (Malaysian Sustainable Palm Oil) certification. Some companies even go all the way to the RSPO (Roundtable on Sustainable Palm Oil), which involves a lot of work and documentation. If they (the green lobby groups) still don’t accept that, there is nothing much we can do, is there?

Gooi adds that, today, even big plantation companies with RSPO certification have problems selling to Europe. “This is the current situation that we are in. Plantation companies will continue to focus on the China and India markets, not so much on the US and Europe.”

(Due to ESG concerns ill-informed people shun palm oil stocks which is wrong, totally wrong as Palm oil is a useful product found in 50% of Super Market items.

So Palm oil adds VALUE TO LIFE)

(Why? ESG SHOULD APPLY TO USA WHICH IS THE WORLD NUMBER ONE EXPORTER OF CIGARRETES (CAUSE CANCER & POLLUTION) & SELL WEAPONS THAT KILL PEOPLE!!)

(IN ANY CASE PALM OIL MAJOR BUYERS ARE INDIA & CHINA WITH COMBINED POPULATION ALMOST 2.8 BILLION PEOPLE ALONE)

8) “Some investors would rather invest in loss-making companies or technology companies that are trading at high PERs; the stock market doesn’t quite make sense. We can only focus on generating profits and paying dividends. In fact, we have been paying up almost all our profits as dividends,” he stresses.

(MR. MARKET IS CRAZY. HE CHASES HOT AIR BALLOON STOCKS BY RUMOUR & HOT AIR & WHAT SYNDICATES WANT TO CHURN UP FOR ALL TO PUNT LIKE A CASINO. SERIOUS INVESTORS WILL SHUN GAMBLING AND INVEST IN PALM OIL. KMLOONG EXPECTS TO GIVE GOOD DIVIDENDS)

9) “The Malaysian government has put a limit on new planting; we can’t plant on jungle land. So, that’s the end of the story. Meanwhile, Indonesia also has a moratorium on the expansion of new plantation areas. Realistically, there is no more land for us to expand. It will be very expensive to buy a brownfield estate. We recently bought an additional 2,700ha estate near Sandakan, so, that’s about all we can do now,” he says.

(SARAWAK ALREADY BANNED CONVERSION FROM TIMBER LANDS TO PALM OIL & INDONESIA LIKEWISE SO THERE IS NO MORE EXTRA LAND FOR EXPANSION FOR PALM OIL PLANTING.)

(NOTE: THIS IS A HIGH BARRIER TO ENTRY FOR PALM OIL AS LAND IS NOW LIMITED OR ALMOST NIL. AND EVEN IF LAND IS AVAILABLE IT WILL TAKE 4 YEARS TO PLANT AND SEE FIRST HARVEST)

(THAT MEANS THAT THOSE WHO OWN PALM OIL LANDS WILL SEE LONG TERM LAND PRICE APPRECIATION AS SUPPLY NO MORE & DEMAND WILL STILL BE THERE)

10) Over the past few years, the milling operations have been contributing 60% of the group’s profits, with the remaining 40% coming from its plantation operations.

“With the high CPO price, we had seen a rather significant shift in our sales mix, whereby the plantation division accounted for 60% of our group’s profit instead,” says Gooi.

He adds that the plantation division’s profit contribution to the group is expected to increase to 70%.

“Our mills are mainly for commercial use. In other words, we source our raw materials from other plantation companies, not from our own estates. Therefore, higher CPO price actually means higher cost for our milling operations.”

(NOTE THIS VERY, VERY, VERY CAREFULLY

Past few years Milling profit was 60%; Sale of Fresh Fruit Bunches was 40%

That was when FFB prices were around Rm350 per ton. Now FFB is over RM800 per ton the shift of earnings

Cpo price plantation now earns 60% (up from 40%) Milling down to 40% (was 60% due to buying Cpo from others at higher price for its Mills)

SEE THIS

Over the past few years, the milling operations have been contributing 60% of the group’s profits, with the remaining 40% coming from its plantation operations.

“With the high CPO price, we had seen a rather significant shift in our sales mix, whereby the plantation division accounted for 6Over the past few years, the milling operations have been contributing 60% of the group’s profits, with the remaining 40% coming from its plantation operations.

“With the high CPO price, we had seen a rather significant shift in our sales mix, whereby the plantation division accounted for 60% of our group’s profit instead,” says Gooi.

He adds that the plantation division’s profit contribution to the group is expected to increase to 70%.

“Our mills are mainly for commercial use. In other words, we source our raw materials from other plantation companies, not from our own estates. Therefore, higher CPO price actually means higher cost for our milling operations.”Over the past few years, the milling operations have been contributing 60% of the group’s profits, with the remaining 40% coming from its plantation operations.

“With the high CPOOver the past few years, the milling operations have been contributing 60% of the group’s profits, with the remaining 40% coming from its plantation operations.

“With the high CPO price, we had seen a rather significant shift in our sales mix, whereby the plantation division accounted for 60% of our group’s profit instead,” says Gooi.

He adds that the plantation division’s profit contribution to the group is expected to increase to 70%.

(NOTE:

Last time MILLING PROFIT 60% & SELLING FFB PROFIT 40%

Now that Palm Oil Prices are High: The Shift: Palm oil makes 60% & Milling 40%

Why Palm oil make more?

Answer:

Because Fresh Fruit Bunches was Rm350 per ton & now over Rm800 a ton - up by over 100%!!)

Why milling profits down?

Answer:

Because their mills must buy more expensive FFB from others.

Now read this

He adds that the plantation division’s profit contribution to the group is expected to increase to 70%.

Read one more time:

(HE ADDS THAT THE PLANTATION DIVISION'S PROFIT CONTRIBUTION TO THE GROUP IS EXPECTED TO INCREASE TO 70%)

THAT MEANS THAT UPSTREAM WILL GET EVEN BETTER WHEN PALM OIL PRICES ARE HIGH

SO THE CONCLUSION

THE PALM OIL COMPANIES WITH LARGE LAND BANKS IN UPSTREAM WILL DO THE VERY BEST AT THIS TIME WHEN LAND IS SCARE & PALM OIL PRICES ARE VERY HIGH))))

Best Regards

Calvin Tan

Please buy or sell after doing your own due diligence or consult your Remisier/Fund Manager

More articles on THE INVESTMENT APPROACH OF CALVIN TAN

Rimbunan Sawit to beef up crop production and yield, By JACK WONG (Calvin Tan comments)

Created by calvintaneng | Apr 06, 2024

TSH RESOURCES VERSUS SERBA DINAMIK (WHY THEIR ACCOUNTS ARE TOTALLY OPPOSITE) Calvin Tan

Created by calvintaneng | Feb 25, 2024

CALVIN SUNDAY SHARING: And God created great whales (Genesis 1:21) Calvin Tan

Created by calvintaneng | Feb 25, 2024

Discussions

Be the first to like this. Showing 13 of 13 comments

Yes durian will take 7 long years to see fruit.

Bud grafted takes 3 to 4 years but won't stand strong wind or else the trunk will snap.

NOW IS SUPER BULL TIME FOR PALM OIL!

BE RELEVANT

2021-08-28 13:49

Note:

It will be very expensive to buy a brownfield estate

Brownfield refers to lands already converted to palm oil with fruiting trees

Greenfield on the other hand means empty lands or virgin forest lands

That means that those currently own palm oil lands will see long term price appreciation

2021-08-28 14:04

KMLoong total Palm Oil Estates are less than 40,000 Acres

These got larger Plantation Lands

FGV

TAANN

TSH Resources

SIMEDARBY PLANT

THPLANT

BPLANT

From 200,000 Acres above.

2021-08-28 16:22

how come nobody likes inno? 77% of their palm tree is in prime mature and the oldest one is just 13 years hence no capex needed for replanting in next 10 years.

2021-09-02 00:16

u cant find any other palm oil company in klse with such a huge DY and young tree profile.

2021-09-02 00:20

InnoPrise Plant is v good

Since TSH Resources is Top 2nd holder of INNOPLANT

GO FOR TSH REOURCES!

2021-09-02 20:35

Why sifu calvin call on buying into plantations relentlessly are very sound investing advice loh?

Yes buy what u understand loh!

Remember 2 of the world most richest & savvy investors w.buffet & bill gates like investing in farmland now mah!

U can emulate them now too mah....!!

Thats why the 2 richest savvy investors have taken note the point of concern that palmoil & commodity price cannot going up forever like the case of glove & eventually the commodity price will also fall 1 day mah!

To address this issue or concern w.buffet & bill gates, say buy farmland & palmoil plantation, even the commodity price fall, u still have great protection on the value of cheap plantation land & farmland mah..!

If u buy into cheap land, u have both margin of safety accorded by cheap land plus prospect of reaping great profit from high palmoil price loh!

Thus u should Quickly Buy into palmoil plantation now, b4 its price shoot up mah!

Time to be a little bit more contraian in view of mkt at reasonable high level mah!

Warren buffet says inflation is definitely coming in view of low interest interest and speculative sign such as bitcoin, rubbish stock price run up sky high and unrealistic stock valuation & expectation and now raw commodities price run up mah!

Bill Gates already bought alot of farmland at low in preparation & in anticipation for the coming armmagedoom coming mah!

Why would one the world tech best richest owner switch alot of his investment into farmland, this bcos farmland or value real estate if it is bought at reasonable low price, u cannot go wrong over longterm bcos the availability of land is limited, u cannot manufacture land like bitcoin mah!

Coming back to msia the equivalent to farmland is oil plantation, u still can get it real cheap & it is paying u reasonably good dividend loh...this is the best defensive & offensive play like bill gates and warren buffet had highlighted mah!

As calvin sifu said timber is at record price & palmoil at record price surely some optimism will spillover to plantation & timber share price mah!

But this up 1 to 2 sen is chicken feed mah, why up so little leh ??

Timber & palmoil share r suffering from lack of production mah and also huge impairment losses on its assets mah & previous falling share price mah!

Thus they are jittery on recovery of palmoil & timber share loh!! They want to see actual profit b4 jump in loh!!

That means if u base on profit...as indicator that means the share price will be lagging loh!

2021-09-03 13:25

JTIASA 206,000 ACRES MORE THAN KMLOONG IN UPSTREAM

NOW CPO VERY HIGH AND KMLOONG NEED TO PAY MORE FOR FFB

SO GO FOR JTIASA, THPLANT, BPLANT OR TSH RESOURCES BEST

2022-03-19 13:16

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Apps

Top Articles

3

TA Sector Research

4

7

BFM Podcast

8

save malaysia!

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

ooi8888

use the big piece of land to plant musangking & black tone durians can earn even more.

2021-08-28 12:54