CEO Morning Brief

Good Time to Buy Planters Even as CPO Rally Seen Losing Steam Soon — Analysts

edgeinvest

Publish date: Wed, 17 Apr 2024, 09:06 AM

KUALA LUMPUR (April 17): The recent spike in crude palm oil (CPO) prices echoes the commodity boom of 2021/22, as supply constraints from lower palm oil production and robust consumer demand push prices up.

The anticipation of production disruption as a result of the prolonged effect of El Niño, which brings dry and hot weather conditions, has also pushed up CPO prices.

Year to date (YTD), the three-month CPO futures have surged over 11%, closing at RM4,074 per tonne on Tuesday. The commodity just hit a high of RM4,336 on April 3.

Bursa Malaysia’s Plantation Index has likewise climbed, rising a total of 5.58% YTD. The index closed at 7,399.24 on Tuesday.

“The rise in CPO prices is in line with the general trend of other commodities, which have been affected by all the recent sanctions on 'unfriendly' nations and escalating geopolitical risks. With shipping routes affected, it has also cost more to transport commodities,” TA Investment Management Bhd chief investment officer Choo Swee Kee told The Edge.

CPO prices are highly correlated to Brent crude, which surged past US$90 (RM431.28) per barrel ahead of Iran's anticipated retaliatory strikes on Israel following the strike on Iran's embassy. It has been hovering near that since Iran struck back over the weekend. At the time of writing on Tuesday, Brent was trading at US$89.73 per barrel, up 16.5% YTD.

While one may think that the condition for CPO prices to continue to rally looks promising, industry analysts believe otherwise as they anticipate palm oil production to increase beginning in May.

That said, analysts still believe it could be an opportune time to invest in plantation stocks, particularly those of pure planters that are heavily involved in the upstream sector with robust production growth.

CIMB Investment Bank’s head of Malaysian research and regional head of agribusiness research Ivy Ng Lee Fang, who is anticipating a softening of CPO prices in May as supplies rebound after the Hari Raya Aidilfitri celebrations and as competition from alternative edible oils increased, has kept kept an 'overweight' rating on plantations.

This is due to improving earnings prospects from lower costs and higher output. “For me, factors such as the EUDR (the European Union’s Regulation on Deforestation-free Products) and ESG (environmental, social and governance) are not new and likely priced in,” Ng said.

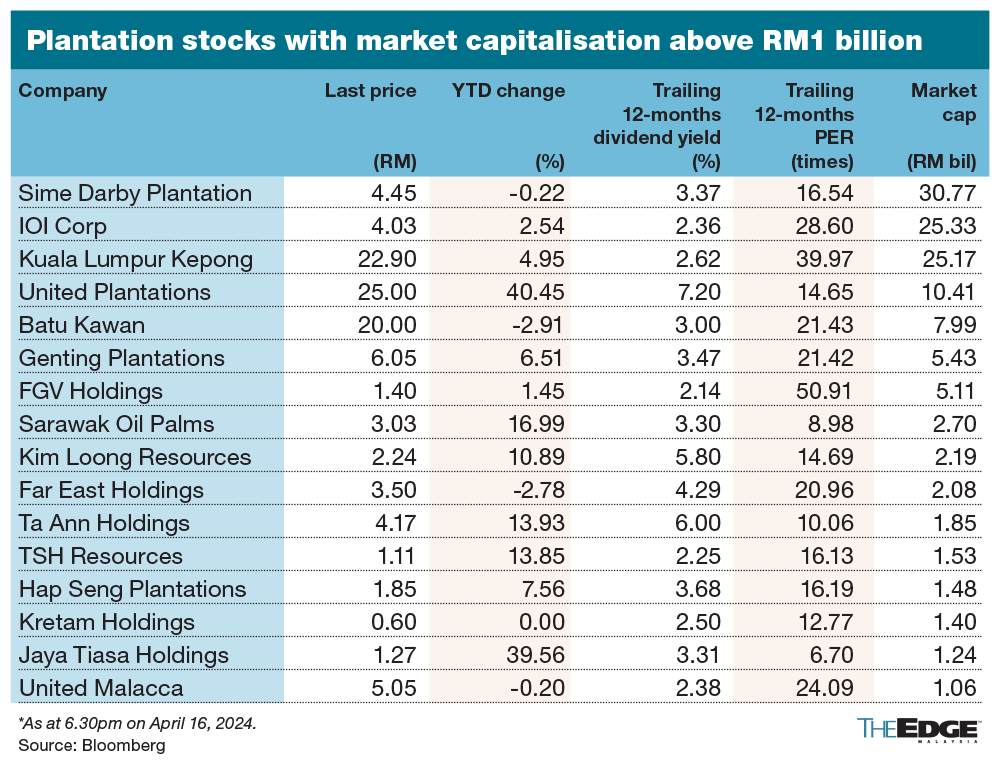

“We have ‘buy’ calls on IOI Corp Bhd, Sime Darby Plantation Bhd, Hap Seng Plantations Holdings Bhd and Ta Ann Holdings Bhd,” she added, while maintaining her average CPO price forecast of RM3,900 per tonne for 2024.

Steven Chong of Apex Securities Research foresees a better top line outlook for plantation companies in the coming quarters, after some companies provided guidance on improved fresh fruit bunch production in 2024 compared to the previous year.

Although market attention is shifting towards the potential impact of La Niña, which, like the El Niño season, can disrupt vegetable oil supply chains, Chong noted that the impact on the weather is currently unclear at this juncture. “Any effects are expected to be felt only in 2H2024 (the second half of 2024),” he added.

But if a strong La Niña event occurs, it could lead to dryness and drought along the southern tier of the US, affecting soybean production in the Midwest US, as well as Argentina and Southern Brazil, UOB Kay Hian Research wrote in a note on April 4.

Apex’s Chong, who is expecting an average CPO price of RM4,000 per tonne for 2024, has United Plantations Bhd (UP) as his top pick. UP closed at a new all-time high of RM24.84 on Monday — surpassing Apex Securities' target price of RM23.57 — giving it a market capitalisation of RM10.34 billion.

UP's remarkable rally, up over 39% YTD, is bolstered by its record earnings and dividends for the financial year ended Dec 31, 2023 (FY2023), driven by a recovery in crop production and improved operating margins.

Apex Securities is the only research house covering UP, which was trading at 14.56 times forward price-earnings ratio (PER) at Monday's market close. In contrast, IOI was trading at 28.74 times PER, while Sime Darby Plantation was at 16.51 times. Hap Seng Plantations was at 16.71 times, and Ta Ann was at 10.15 times, Bloomberg data showed.

The 12-month trailing dividend yield for UP stood at 7.25%. IOI's was at 2.35%, while Sime Darby Plantation was at 3.38%, followed by Hap Seng Plantations at 3.56%, and Ta Ann at 5.94%.

Impact of Latin America's shift to palm oil production limited on Southeast Asia — for now

Analysts anticipate that the shift in palm oil production to Latin America will profoundly affect Malaysia and Indonesia, which currently dominate the market, as Latin America contributes only 5% to total palm oil output.

“We believe that in the short term, it is improbable for this to have a significant impact, as it will take time for them to match Malaysia's production efficiency. However, we view this as a dynamic shift in the long run, foreseeing that Malaysia will gradually capture a smaller market share in the future, due to the scarcity of land for expansion to accommodate the growth in demand as the population increases,” said Chong of Apex Securities.

Bloomberg reported that the shift towards Latin America as a major player in the palm oil market poses a challenge to Southeast Asian producers, particularly in Europe, where there is increasing demand for sustainably sourced products.

With their ability to produce higher yields and demonstrate traceability in their supply chains, Latin American producers are gaining a competitive edge in the global palm oil market.

In contrast, Malaysia and Indonesia face challenges such as ageing trees and labour shortages, which are diminishing palm oil productivity. Additionally, stricter regulations on land clearing are impeding replanting efforts in these regions.

Source: TheEdge - 17 Apr 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-04-30

JTIASA2024-04-30

KLK2024-04-30

UTDPLT2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

CIMB2024-04-29

FGV2024-04-29

FGV2024-04-29

FGV2024-04-29

FGV2024-04-29

HSPLANT2024-04-29

IOICORP2024-04-29

KLK2024-04-29

KLK2024-04-29

KLK2024-04-29

KLK2024-04-29

KLK2024-04-29

KLK2024-04-29

KLK2024-04-29

KRETAM2024-04-29

SIME2024-04-29

SIME2024-04-29

TAANN2024-04-29

UTDPLT2024-04-29

UTDPLT2024-04-27

KLK2024-04-26

BKAWAN2024-04-26

IOICORP2024-04-26

KLK2024-04-26

SIME2024-04-26

SIME2024-04-26

SIME2024-04-26

SIME2024-04-26

SIME2024-04-26

SIME2024-04-26

TAANN2024-04-26

UTDPLT2024-04-25

CIMB2024-04-25

CIMB2024-04-25

CIMB2024-04-25

CIMB2024-04-25

CIMB2024-04-25

GENP2024-04-25

IOICORP2024-04-25

KLK2024-04-25

KLK2024-04-25

SIME2024-04-25

SIMEPLT2024-04-25

SIMEPLT2024-04-25

UTDPLT2024-04-25

UTDPLT2024-04-25

UTDPLT2024-04-25

UTDPLT2024-04-24

CIMB2024-04-24

CIMB2024-04-24

CIMB2024-04-24

CIMB2024-04-24

IOICORP2024-04-24

KLK2024-04-24

KLK2024-04-24

KLK2024-04-24

SIME2024-04-24

SIME2024-04-24

SIME2024-04-24

SIME2024-04-24

SIME2024-04-24

SIME2024-04-24

SIME2024-04-24

SIME2024-04-24

SIMEPLT2024-04-24

UTDPLT2024-04-24

UTDPLT2024-04-24

UTDPLTMore articles on CEO Morning Brief

Turkish Airlines in Talks With Airbus, Boeing to Buy 235 Planes

Created by edgeinvest | Apr 30, 2024

Indonesia's GoTo Says on Track for Profitability Despite 1Q Loss

Created by edgeinvest | Apr 30, 2024

Petrofac Shares Hit Record Low After Warning It Will Miss Coupon Payment

Created by edgeinvest | Apr 30, 2024

China Hints at Retaliation After Biden Signs Taiwan, TikTok Legislation

Created by edgeinvest | Apr 30, 2024

Japan Opts to Keep Traders in Dark on Whether It Intervened in Yen

Created by edgeinvest | Apr 30, 2024

Discussions

Be the first to like this. Showing 2 of 2 comments

In Year 2021 we Recommended Top 10 Palm oil Stocks

See

https://klse.i3investor.com/web/blog/detail/www.eaglevisioninvest.com/2021-11-04-story-h1593687704-Reposted_Article_OIL_PALM_STOCKS_IN_Bull_Run_Time_Those_Prepared_with_B

All these are PURE UPSTREAMS

1. Bplant was 57 sen

LTAT took it private at Rm1.55

2. Jaya Tiasa (Jumping Tiger)

Was 63 sen. Now Rm1.32

1 & 2 up by over 100% each

3. Thplant

Was 47 sen. Now 68 sen

Up 45%

4. TSH RESOURCES

Was Rm1.09. Now Rm1.13

While all above Bplant, Jtiasa & Thplant up from 45% to over 100%

Tsh Resources only up by a mere 3%

SO%

SO THE BEST COURSE OF ACTION IS TO SELL BPLANT & ALL IN TSH

SELL SOME JTIASA KEEP SOME FOR HIGHER & THEN SWITCH TO TSH RESOURCES

ALSO TAKE SOME PROFIT FROM THPLANT AND KEEP SOME THPLANT FOR HIGHER PRICES

THEN SWITCH TO TSH RESOURCES

ALWAYS SELL INTO STRENGTH & BUY THE LAGGARDS!

IN THIS CASE TSH RESOURCES IS THE LAGGARD

AND CAN BUY EVEN MORE TSH RESOURCES WHILE STILL SO VERY CHEAP

IT IS ONLY A MATTER OF TIME TSH RESOURCES WILL ALSO RISE UP TO JOIN THE OTHERS

"SUCCESS BEGETS SUCCESS"!

1 week ago

Post a Comment

Featured Posts

Open a Moomoo Account Today and Win an Apple iPad Air*!

Apps

Top Articles

1

AmInvest Research Reports

2

3

4

6

7

save malaysia!

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

calvintaneng

Definitely

Now Fcpo over Rm4,000

Cost of Cpo production for Tsh Resources & Km Loong only Rm2,000 to Rm2200 MT

So the gross profit is 90% to 100%

Plus Palm oil is a basic necessity used in so many many things like toothpaste, cooking oil & 50% of all Supermarket Items

Few Industries can even earn 20% to 30% gross

Go for Palm oil Stocks now is no brainer!

Just buy a basket of undervalue Palm Oil companies in Pure Upstream

https://klse.i3investor.com/web/blog/detail/www.eaglevisioninvest.com/2024-02-22-story-h-188275986-WHY_WHEN_CPO_PRICES_ARE_HIGH_UPSTREAM_PALM_OIL_PLANTERS_WILL_DO_FAR_BET?_gl=1*1rpvh4g*_ga*MjQzMzEyNDgyLjE3MTMzODg5OTg.*_ga_MNBHX2J50S*MTcxMzM4ODk5OC4xLjEuMTcxMzM4OTYxMy41NS4wLjA.#google_vignette

1 week ago