CEO Morning Brief

Top Glove Bled Heavier Than Analysts Expected in 3QFY2023

edgeinvest

Publish date: Tue, 20 Jun 2023, 08:45 AM

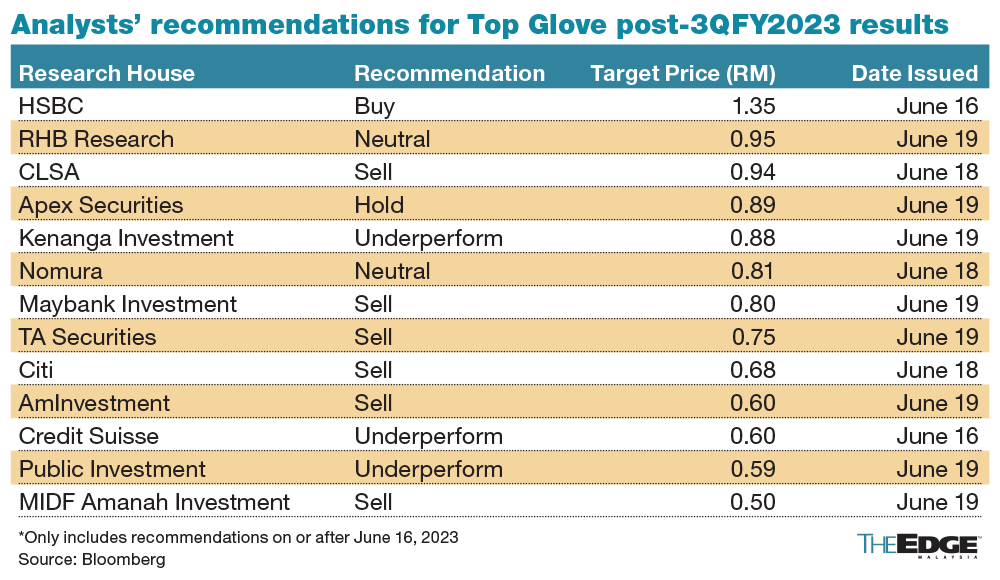

KUALA LUMPUR (June 19): Analysts across the board have downgraded their target prices (TPs) on Top Glove Corp Bhd, after the glovemaker's net loss for the third quarter ended May 31, 2023 (3QFY2023) came in heavier than expected.

Kenanga Research analyst Raymond Choo Ping Khoon said the 3QFY2023 net loss miss marked a nine-month (9MFY2023) net loss of RM464 million, which already exceeded both the research house's full-year net loss estimate of RM450 million and consensus forecast of RM461 million.

“The variance against our forecast came largely from a weaker-than-expected sales volume and cost escalation,” he noted.

In view of the forecast miss, Choo said Kenanga Research widened its FY2023 forecasted net loss for Top Glove by 26% to RM568 million but maintained its expectation for the glovemaker to return to the black with a RM41 million forecasted net profit in FY2024.

Choo said that while Top Glove is hopeful for glove replenishment activity to pick up in the second half of 2023 (2HCY2023), premised on depleting customers’ inventory, the analyst is sceptical for sales volume to increase in subsequent quarters, taking a cue from the industry’s guidance for persistent oversupply in the market.

“Taking stock, the group has received mixed response in terms of customer inventory levels. Some customers are still stuck with high inventories while others are beginning to slowly re-stock,” Choo said.

“Generally, there is no urgency for buyers to place sizeable orders or hold substantial stocks as supply is plentiful and readily available,” he added.

Choo reiterated his “underperform” call on Top Glove with a lower TP of 88 sen (previously 90 sen) based on 1.4 times FY2024 forecasted book-value-per-share (BVPS), at a 20% discount to the glove sector’s average of 1.7 times seen during the previous downturns in 2008 to 2011 and 2014 to 2015, as he believes the current downturn could go down in history as “one of the deepest ever”.

Likewise, Top Glove’s 9MFY2023 net loss also exceeded Citi Research analyst Megat Fais' full-year forecast of RM411 million.

However, the research house underlined that on the positive, average selling price (ASP) rose 6% quarter-on-quarter (q-o-q) — albeit at the expense of volume, which dropped 21% q-o-q.

“Given the implication on volume, tone on ASP was more guarded, although tailwinds from lower feedstock and favourable foreign currency exchange should continue to underpin sequential improvement,” Megat said, adding, however, that management made it clear that returning to the black is unlikely in the near term.

The Citi Research analyst widened his forecast for Top Glove’s FY2023 net loss to RM566 million, and expects the glovemaker to return to profit in FY2024 with a forecast net profit of RM63 million, and subsequently forecasts a RM254 million net profit in FY2025.

“Maintain ‘sell’, our TP moves to 68 sen on an unchanged one-time average calender year 2023 and 2024 estimate book (rolled-over), which implies a FY2025 estimated PER (price-to-earnings ratio) of 22 times,” he added.

Glove ASP hike limited by pricing competition from players in China

Likewise, PublicInvest Research analyst Thye May Ting also set an “underperform” call on the stock with a lower TP of 59 sen, based on two-year average forward earnings, pegged to a five-year average PER of 30 times.

In Thye’s view, Top Glove’s 9MFY2023 core net loss of RM420.4 million was within the house’s expectations at 71.3%.

She maintained her FY2023 net loss forecast of RM559.6 million, but cut its net profit forecast by an average of 12% to RM118.8 million for FY2024 and RM232 million for FY2025, to factor in expected lower sales volume.

The PublicInvest Research analyst said that in line with the prolonged glove oversupply environment, Top Glove has taken steps to decommission two old production lines with five billion pieces capacity annually, and temporarily shut down 17 out of 49 factories which run 35 billion pieces capacity annually.

“This will shave off around 40% of the total capacity from 100 billion to 60 billion pieces per annum,” Thye noted.

“While management believes that ASP has bottomed out and has implemented a turnaround plan to raise ASP by about 3% to 5%, we reckon that its ability to do so will be limited by the intense pricing competition from China glove players,” she added.

The higher-than-expected net loss in 3QFY2023 also pushed Apex Securities Bhd analyst Alman Kamil to raise his FY2023 forecasted net loss for Top Glove to RM550.9 million, from RM120.2 million previously.

“Additionally, we have lowered our forecast for FY2024 net profit to RM132.3 million, anticipating a slower sales volume in the future due to higher ASP and the presence of unforeseen operating costs in a competitive market environment,” he added.

Overall, Alman maintained a "hold" call on the stock with a lower TP of 89 sen (previously 90 sen), pegged at 54 times FY2024 forecasted earnings per share (EPS) of 1.7 sen, which is lower than the five-year +2 standard deviation (SD) of 59 times PER but higher than its five-year +1 SD of 40 times PER.

“We believe that the ascribed PER multiple is justified by its (i) current market share and its industry positioning, (ii) utilisation rate, (iii) Top Glove Turnaround Plan long-term growth plans, and (iv) financial performance,” he added.

At the time of writing, Top Glove shares were down two sen or 2.05% at 95.5 sen, giving the group a market capitalisation of RM7.8 billion.

Read also:

Top Glove's 3Q net loss narrows q-o-q on higher selling prices, cost optimisation

HLIB does not anticipate Top Glove to return to black anytime soon

Source: TheEdge - 20 Jun 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on CEO Morning Brief

Digital Nasional Names Senior Telco and Tech Leaders as New Directors

Created by edgeinvest | Apr 26, 2024

Indonesia's Prabowo Closes in on Parliamentary Majority After Rival Party Pledges Support

Created by edgeinvest | Apr 26, 2024

Palm Oil Producers Urges EU to Delay Deforestation Rules for Small Businesses

Created by edgeinvest | Apr 26, 2024

Thailand to Appoint Former Energy Executive Pichai Finance Minister — Reuters

Created by edgeinvest | Apr 26, 2024

Asia’s Hawks Get Put on Alert After Indonesia’s Shock Rate Hike

Created by edgeinvest | Apr 26, 2024

Malaysia Needs RM10 Bil for Next Three Years to Upgrade Water Infrastructure — SPAN

Created by edgeinvest | Apr 26, 2024

Land Use Planning for Food Source Areas Master Plan Approved — KPKT

Created by edgeinvest | Apr 26, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Apps

Top Articles

1

2

save malaysia!

4

BFM Podcast

5

BFM Podcast

6

BFM Podcast

7

Good Articles to Share

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....