HLBank Research Highlights

Destini - Negatives Priced In; Potential Downtrend Reversal

Destini’s (Non-rated) share prices slid 40% in 3 days post GE14 amid fears of the new PH government would review the on-going and upcoming projects. We opine that the selling was overdone as Destini’s 6.3x FY19 P/E (36% below its average 10-year P/E of 9.8x) and 0.59x P/B (55% lower than 10-year average of 1.3x) could have priced the potential business uncertainty, supported by its high barrier to entry businesses and decent orderbook coupled with an anchor shareholder, MoF.

An Established Integrated Solutions Provider With Global Presence. Destini is a one-stop engineering solutions provider with diverse interest in the aviation, marine, land transport as well as O&G sectors. With a core business in ensuring safety and survival equipment efficiency in these industries, the Group excels in being one of the leading maintenance, repair and overhaul (MRO) service provider in the regions. To date , Destini has expanded its geographical footprint over the Asian, Australian, Middle East and European regions. In FY17, the marine divisions contributed 52% to revenue while the rest were from aviation (40%), O&G (4%) and land & transport and others (4%). Currently, Destini’s single largest shareholder is Dato’ Rozabil Abdul Rahman (Group MD) with a 24.8% stake, followed by Aroma Teraju (17.3%), a wholly-owned subsidiary of the Ministry of Finance.

Values Emerge After Recent Rout. Destini’s share prices slumped 40% from RM0.43 on 8 May to RM0.26 yesterday on the back of knee-jerk selling activities. We opine that the selling was overdone as Destini’s 6.3x FY19 P/E (36% below its average 10- year P/E of 9.8x) and 0.59x P/B (55% lower than 10-year average of 1.3x).

Destini’s core business of maintenance, repair and overhaul (MRO) safety and survival equipment for the Royal Malaysian Arm Force (RMAF) is defensive and has high barrier of entry and its orderbook of ~RM930m could provide earnings visibility for FY18-19. With the group’s proven expertise and experience as well as good track record and competitive pricing, we see there are good chances of success in new helicopter supply, vessel construction orders and rail related contracts. Many of the existing and new contracts will also provide MRO service opportunities.

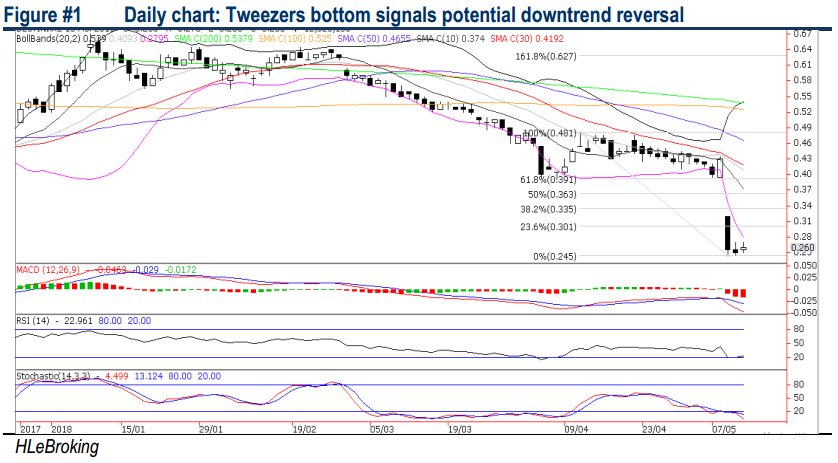

Potential Downtrend Reversal. Technically, the positive Tweezers bottom could signal potential downtrend reversal after recent slump. Moreover, significant downside risks are limited amid steeply oversold indicators. A decisive breakout above RM0.30 (23.6% FR) will spur share prices higher towards RM0.335 (38.2% FR) before reaching our LT objective at RM0.36 (50% FR). Conversely, immediate supports are RM0.245 (14 May low) and RM0.24. Cut loss at RM0.225.

Source: Hong Leong Investment Bank Research - 17 May 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-11-15 16:40:00

EMA 5

10 Mins

BUY

2024-11-15 16:40:00

ADX

10 Mins

BUY

2024-11-15 16:40:00

TURTLE SYSTEM 20

10 Mins

BUY

2024-11-15 16:40:00

EMA 5

5 Mins

BUY

2024-11-15 16:40:00

ADX

5 Mins

BUY

Apps

Top Articles

1

2

3

Mercury Securities Research

4

BFM Podcast

5

BFM Podcast

7

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....