Ipodkaki's blog

WTK - My 2 cents on the Quarterly Results and Others

Summary

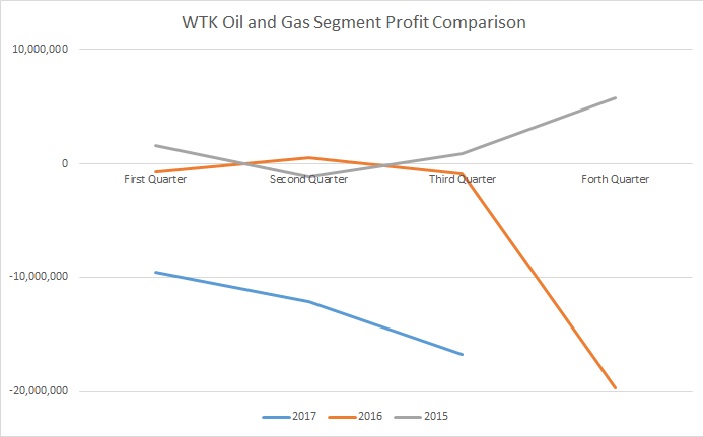

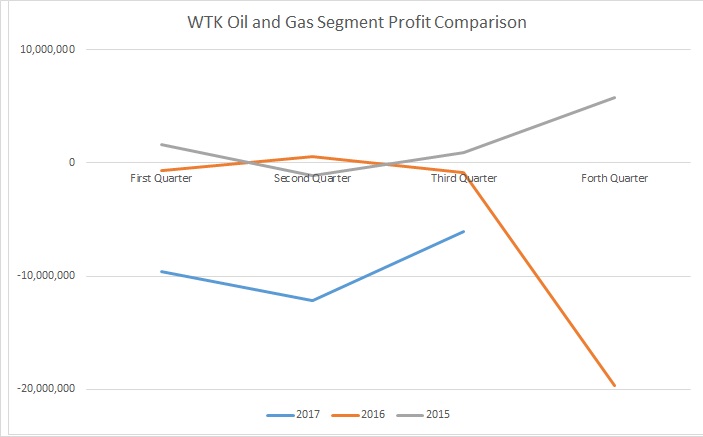

- WTK recorded 17 million of loss in quarter of 30-06-17 to 30-09-17

- 10 million Impairment loss and the project status in Oil and Gas segment

- Impacts of the hike of hill timber premium rate to Timber segment

- New Palm Oil Mill commisioning is complete and will contribute in the coming quarters

- What is next?

Yes, The Result is bad despite of Revenue up 15%

As a share holder of WTK holdings, yes I was disappointed when I saw the result. If you are not a new share holder, you probably already know that is because of the oil and gas segment. WTK recorded 17 million of loss in this quarter.In fact, this is the greatest loss quarter in the last 11 years.

According to the management, it is due to the 10 million impairment loss in the trade receivable in oil and gas.

I am not sure if Market is expecting they will be profitable in Oil and Gas this quarter but I personally think it has pretty much already priced in. WTK share price has been beaten down for very long time

I know right? Oil and Gas Segment Again!

"The higher loss before tax in the current quarter was mainly due to allowance for impairment loss on trade receivable of RM10.0 million provided on a more prudent basis and share of loss of an associate company for having to continue to incur charter fee and operation costs to maintain its vessels in the ready state of deployment despite these vessels were off-hired due to temporary project deferment. Besides, the loss before tax also took into account the amortization of intangible assets of RM0.7 million embedded in investment in the associate company."

Main culprit of the loss - the impairment loss and amortization of intangible assets in Oil and Gas - 10.7 million.

I am not an account expert and will welcome any expert to join the discussion and provide insights. From my understand, it seems like they have some bad debts due to some clients have to defer the project. Thus, they decided to allow this one time impairment loss in receivable?

Finally, they provided more insights in their oil and gas segment status.

- Compared to last quarter's surprising/embarrassing 0 revenue, this quarter they somehow managed to engage the Alanya Marine Ventures Sdn Bhd and have 12.1 million charter fee.

- The last two off work vessels are STILL waiting on Petronas.

- They managed to get some work under Petronas's general umbrella project

- They managed to offload the vessels to other majors in August and September.

Although it is not enough to make it profitable but at least the oil and gas are progressing. Hopefully with the oil price comes back in $58 (about 20% higher than the average oil price in July 1 to September 30), they will do better and Petronas will soon assign some projects to them. And if this impairment loss in receivable is considered one time shot in a long time, the actualy loss in Oil and Gas is around 6 million.

Cost of Timber Segment Rise

Timber and Plantation - Combined revenue up ~40 million, about 25%. But hike of hill timber from RM0.80 per cubic meter (“M3”) to RM50.00 per M3 costs the timber segment. That's why this quarter Timber only contributes 2.58 million profit.

To be honest, unless the Sarawak Government revises this crazy hikes or else those upstream Timber companies in Sarawak will continue to see their profit flat or decline. Maybe WTK should use her 400 million cash to move faster to the downstream of the industry or buy some furniture company to offload its log with better profit margin.

Good future of Plantation

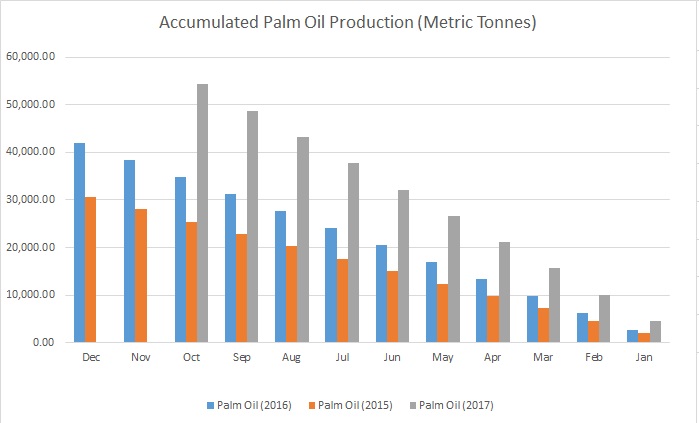

If if you have following its monthly plantation report, you can see the exponential growth of their palm oil sector. The Group’s total mature area to 6,100 hectares as at 31 December 2016 (2015: 4,600 hectares), and if taking the same rate in 2017, it will be 7600 hectares.

Also, if you compare their palm oil production month by month and year by year, it has been increasing exponentially.

That's why despite off the falling of palm oil price (about 15% lower compared to 2nd quarter) Compared to last quarter, revenue doubled from 8.3 million to 17.7 million. Despite higher revenue, higher loss before tax at due to the inclusion of preoperating expenses of its POM.

Their 40 million Palm Oil Mill is complete and expected to contribute in the coming quarters as the initial commissioning performance was promising and within our expectations

CASH and Valuable Asset. What is next?

Honestly, 3rd quarter is not a good quarter for WTK. I hope the management continue to work out options for Oil and Gas segment and have to work out the alternate client base other than Petronas. Also worth to note that WTK is holding 403 million cash on hand, even after debt deduction it is still a 150 million net cash company.

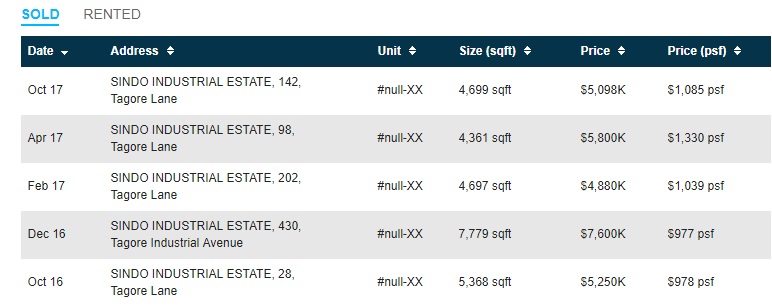

I also noticed that WTK is holding some valuable asset, the one really attracts me is the Tagore Lane Industrial Estate buildings and land. Those are 19000 ft freehold property in SINGAPORE. The netbook value per annual report is around RM 10.5 million but It was probably never been revalued since its purchase 33 years ago as the land and housing prices hike drastically.

For example according to srxproperty site, the price per squareft in Tagore industrial area is between SGD980-1300. Even If we take the lower side, WTK's asset overthere is easily = SGD 980 * 19000 = SGD 18.6 million, which is around RM 56.7 million (5 times of the current book value). Not to mention other undervalue asset like the 98000 sq ft land in Lumut.

However no matter how valueble are the asset that WTK have and how cash rich they are, that won't turn to be profit unless the management turn the oil and gas division around and reduce cost of lumber division. Of course, the internal family issue needs to be sorted out. Then spend the cash in some strategic areas and we will see WTK rises again with the plantation growth.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

Discussions

1 person likes this. Showing 13 of 13 comments

Dato Calvintan specialist in providing free Holland ticket but himself didn't buy it. He just lonely and you guys attentions only.

2017-12-01 08:20

not easy to be terbalik king. even monkey has 60 percent winning rate but terbalik king has 0%.

2017-12-01 12:11

yes David you are damn right. lonely old fark just here to talk cock. u listen to him u die.

2017-12-01 12:12

the wtk management has made a damn wrong decision in venturing into o&g business, it is killing the company in the long run, the only way to turn around is to drop o&g business immediately

2017-12-01 15:21

@ipodkaki

an old eagle who non stop talking craps and liked his own post every day and yet fails to beat the worst performing Asian market

2017-12-01 15:54

Holland tickets for us to make Holland babies in Holland who would then enjoy the assets invested by grandpa 10-20 years earlier in Bursa

2017-12-01 15:55

Don't forget this is also on top of sifu KC recommendation. So, if you have faith in KC and many would, then should keep WTK

2017-12-01 15:59

ironically you will be making a fortune if you buy the stocks that King of Terbalik defined as " crap stocks ".

2017-12-01 16:01

@beso,

I agree partially with you. If you consider the recent hike of the timber premium rate from 0.80 to RM 50, long term they need to diversify the business. Plantation of palm oil was a great move. Entering oil n gas could have been a great move as well, just their timing was horribly wrong. They entered when the oil price was peak n it was the ending of that oil bull run. Its all about timing and now it is up to them to decide want to painfully maintaining the oil n gas business till the price back to good time or just sell away.

I think share holder also the same, they have multiple problems like family issues and oil n gas at the moment but you cant deny their base n asset, they have cash, the palm oil division gonna contribute.

2017-12-01 16:11

Just chop off oil and gas , company will be save, otherwise company going to Holland, cannot keep loss making company

2017-12-03 09:36

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Apps

Top Articles

3

Chaos Stock

4

save malaysia!

5

6

Bull Run Stock for Year 2024

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

John Lu

Another holland stock from Dato Calvin

2017-12-01 07:46