HLBank Research Highlights

Traders Brief - Anticipate a mild relief rally

MARKET REVIEW

Asian stocks were significantly lower with the negative political turmoil backdrop in the Italy, coupled with the uncertain actions by Donald Trump in the trade war developments. The Nikkei 225 fell 1.52%, while Shanghai Composite Index and Hang Seng Index declined 2.53% and 1.40%, respectively.

Tracking bearish sentiments on the regional and Wall Street, stocks on the broader market ended mostly lower. The FBM KLCI plummeted 3.18% to 1,719.28 pts. Most of the construction stocks headed for another round of selling activities after the new government decided to scrap HSR/MRT 3 rail projects for now to strengthen its financial positions. Market volumes stood at 3.60bn, worth RM4.46bn and market breadth was weak with losers outpaced gainers by a ratio near to 7-to-1.

US stocks soared overnight, rebounding from the previous day’s rout, as energy shares bounced back amid a rally for oil prices (WTI +2.2%) and worries over Italy’s political crisis faded. The Dow surged 1.26% or 306 pts at 24,667, taking back most of Tuesday’s 392-point drop.

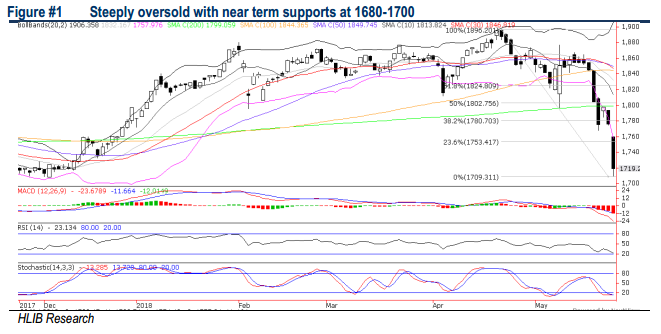

TECHNICAL OUTLOOK: KLCI

In wake of bearish Wall Street and regional markets performance, KLCI gapped down to 1,759.6 (-16.3 pts), and sliding further to an intra-day low at 1,709.5 (-66.3 pts) before narrowing the losses to 56.6 pts at 1,719.3. Following 3.2% plunge, the MACD has expanded negatively below zero, while the RSI and Stochastics oscillators are dipping further into oversold territory. Taking cues from Dow’s 1.26% rebound overnight, KLCI may stage a long awaited relief rally today after nosediving 6.9% or 127 pts in 12 trading days. Upside targets are situated at 1743/1753/1780 while supports are located at 1700/1680.

As the lift from robust global demand is less assured in 2018 and downside risks are heightened amid elevated trade tensions between the US-China, rising geopolitical risks, soaring bond yields, coupled with the still unresolved Italy political crisis, KLCI near term outlook would remain volatile. Sentiment will be further dampened in view of the renewed concerns of 1MDB scandal and piling national debts as well as awaiting more policy pipeline from the new PH regime, following a landmark shift for Malaysia from the six-decade rule of the BN.

TECHNICAL OUTLOOK: DOW JONES

The Dow’s bearish engulfing reversal pattern was spotted after hitting monthly high of 25,086 (21 May) from a low of 23,886 (3 May). Subsequently, the index plunged 3.5% to a low of 24,247 (29 May) before staging 306 pts rebound to 24,667 overnight. We expect consolidation to prevail unless the index can surpass downtrend line at 24.8k decisively. Higher upside targets are 25.0-25.5k while supports fall on 24.0-24.2k

On the Dow outlook, ongoing concerns on trade war and the focus on US-North Korea summit coupled with unresolved political turmoil in Italy (although risks had eased) could spark interim volatility towards the stock markets. We expect Dow to trend range bound within 24k-25.3k in the short term, prior to the 12-13 June FOMC meeting.

TECHNICAL TRACKER: FRONTKEN CORPORATION

At RM0.41, Frontken is trading at 10.3x FY18 P/E (against 5-year average of 20x). Excluding its net cash with RM96m or 9.1 sen per share, valuation is even more compelling at 8x P/E. Downside risk is limited, as sentiment is boosted by recent USD strength (vs RM), potential triangle breakout and company‘s recently approved share buy-back exercise.

Source: Hong Leong Investment Bank Research - 31 May 2018

More articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

2

3

4

Mercury Securities Research

5

BFM Podcast

6

BFM Podcast

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....