HLBank Research Highlights

Traders Brief - Mildly Positive, But Upside Limited

MARKET REVIEW

Key regional benchmark indices ended higher, taking cues from overnight Wall Street performance, coupled with better-than-expected jobs report last week. The Nikkei 225 and Hang Seng Index gained strongly by 1.37% and 1.66%, respectively. Meanwhile, lingering trade concerns limit the upside potential of Shanghai Composite Index at 0.52%.

However, sentiment on our local bourse was mixed and the FBM KLCI traded marginally lower by 0.07% to 1,755.17 pts. Market breath, however was slightly positive with 477 gainers vs 444 losers, accompanied by 2.77bn shares traded for the session, worth RM2.82bn. Sectors such as technology and construction sector bucked the KLCI trend as ringgit is traded near the RM4.00/USD level, while some bargain hunting activities were spotted among oversold construction stocks.

Wall Street brushed off the trade tensions and focused on the economy and jobs data, resulting in most of the technology giants such as Apple and Amazon hitting all-time-highs. Also, retail stocks like Walmart and Target were traded higher. The Dow and Nasdaq gained 0.72% and 0.69%, respectively.

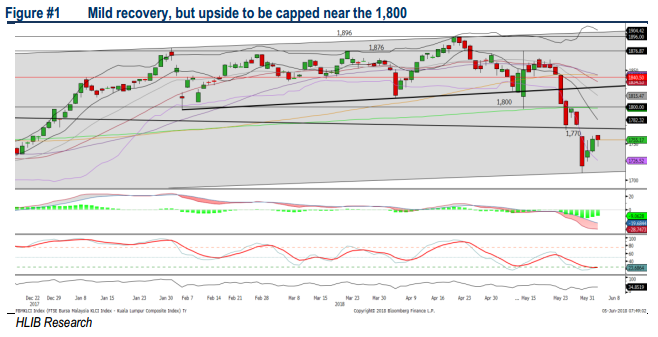

TECHNICAL OUTLOOK: KLCI

The FBM KLCI has recovered from the recent low of 1,710. Also, the MACD Histogram is recovering mildly but still below zero. However, the RSI and Stochastics oscillators are moving out of the oversold region. Hence, we believe there could be a slight recovery of the key index towards 1,770 and next resistance will be envisaged around 1,800. Support will be pegged around 1,710-1,730.

With the positive overnight performance of Wall Street, we may anticipate slight rebound of the FBM KLCI towards 1,770. However, the concerns on 1MDB and uncertain growth outlook for Malaysia as some of the mega construction projects have been axed as well as the national debt worries may limit the upside of the KLCI around 1,800 for the near term.

TECHNICAL OUTLOOK: DOW JONES

The Dow continues to hover above the SMA200 level, forming a flag breakout. The MACD indicator trended higher for the session, accompanied by improving momentum oscillators such as RSI and Stochastics. Hence, the Dow may revisit the 25,000 psychological level. Support will be located around 24,000.

We think the near term trading tone will still be positive as investors focused on the fundamentals of the economy. However, should there be any negative comments related to trade issues by Donald Trump in the G7 summit that will be held this week, it may send cautious signals towards the markets.

TECHNICAL TRACKER: POWER ROOT

Decent dividend yield to cushion the downside risk. Power Root (PWROOT) registered a core PATAMI of RM23.8m for FY18 (vs. RM34.8m in FY17) due to weaker sales from export and domestic sales and higher amount of expenses incurred from structural exercise, but dividend yield remain attractive at 6.3%. Also, we think the zero-rated GST and stable ringgit trend may support sales from domestic and exports. PWROOT is building a base near the RM1.40-1.50 levels and could poise for a sideways breakout.

Source: Hong Leong Investment Bank Research - 5 Jun 2018

More articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

2

3

4

Mercury Securities Research

5

BFM Podcast

6

BFM Podcast

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....