HLBank Research Highlights

Tradersbrief - Technical Rebound in for FBM KLCI

MARKET REVIEW

Asia’s stock markets were spooked by the arrest of Huawei’s CFO, Meng Wanzhou in Canada, which led to severe selloffs in technology stocks across the region; the Nikkei 225 dived 1.91%, while Hang Seng Index and Shanghai Composite Index plunged 2.47% and 1.68%, respectively.

Meanwhile, stocks on the local front traded mostly lower, tracking the weaker regional sentiment; the FBM KLCI fell 0.29% after rebounding from an intraday low of 1,670 level. Market breadth was still bearish with 588 decliners vs. 259 advancers, accompanied by 1.96bn of shares traded, valued at RM1.86bn. However, we noticed selected O&G related stocks such as PCHEM, CARIMIN and SAPNRG were traded higher ahead of the OPEC meeting.

Initially, stocks on Wall Street fell sharply (Dow plunged near to 800 points) amid continuing concerns over US-China trade developments as well as the fear over a potential economic slowdown. However, the sentiment rebounded strongly after news related to the Federal Reserve to tighten monetary policy at a slower-than-expected pace after the December hike. The Dow and S&P500 closed 0.32% and 0.15% lower, respectively, but Nasdaq added 0.42%.

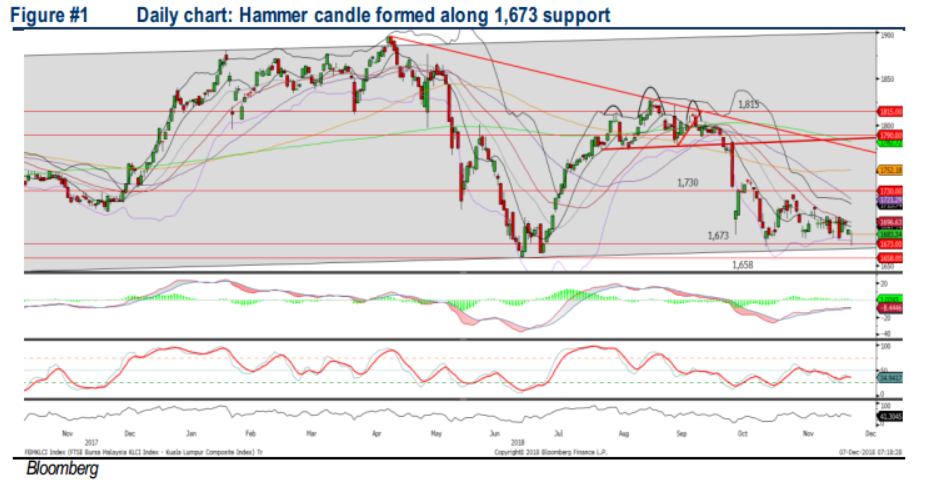

TECHNICAL OUTLOOK: KLCI

The FBM KLCI traded towards the intraday low before recovering higher to close at 1,683 level. The MACD Line is still staying flattish below the zero level, while both RSI and Stochastic oscillators are hovering below 50. Nevertheless, we believe the FBM KLCI could perform a technical rebound, tracking the positive sentiment from Wall Street. With the slightly negative technical readings, the upside may be capped along 1,700-1,704. Meanwhile, support will be located around 1,673, followed by 1,658.

On the local front, we may anticipate a positive rebound after the Dow recouped more than 700 points from the intraday low (24,242.22 pts). Also, traders may be focusing on the members (Top Glove, TM, KLCCP and Ambank) of KLCI after the index review statement was released yesterday. Besides, O&G sector may still trend sideways as the uncertain OPEC and non-OPEC in production cut still persists, which dampened the Brent oil prices overnight.

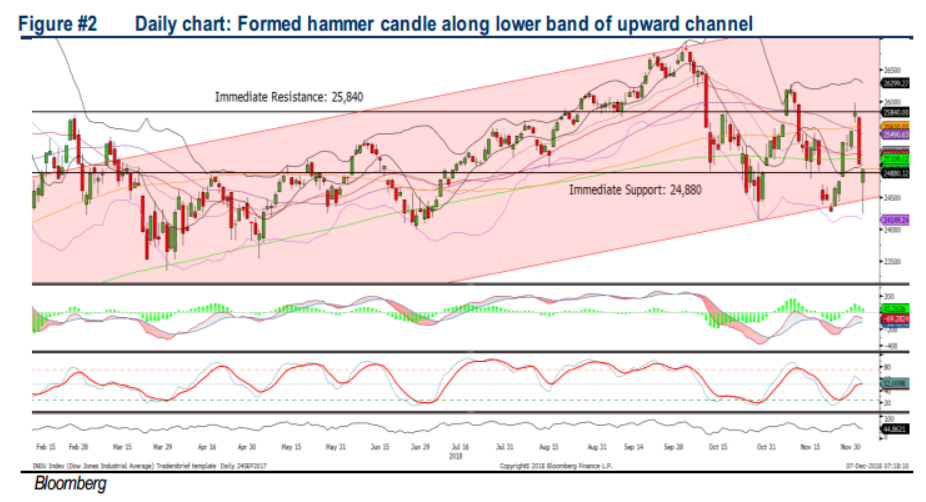

TECHNICAL OUTLOOK: DOW JONES

The Dow resumed trading and plummeted towards an intraday low of 24,242.22 pts before rebounding more than 700 pts, forming a hammer candle above the lower band of the upward channel and closing above the support of 24,880. The MACD Line and Histogram turned slightly negative, while the RSI is hovering below 50. Resistance will be pegged around 25,840, while support will be located around 24,880, followed by 24,500.

Sentiment is likely to stay positive after the strong rebound yesterday with the fresh information from the Fed; this could boost markets higher at least for the near term. However, the uncertain and lacking of details on the trade developments between the US and China, coupled with the inversion of yield curve (3-year and 5-year bond yield) will continue to cap the upside potential on Wall Street. Meanwhile, market participants will need to monitor closely on the upcoming FOMC meeting (18-19 Dec) and Powell’s statement.

Source: Hong Leong Investment Bank Research - 7 Dec 2018

More articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

BFM Podcast

2

4

BFM Podcast

5

BFM Podcast

6

BFM Podcast

7

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....