HLBank Research Highlights

Traders Brief - Local Bourse May Rebound on ECRL Newsflow

MARKET REVIEW

Asia’s stock markets ended mostly lower without any fresh developments on the US -China trade discussions. Also, following the release of the Fed’s March FOMC meeting minutes, which revealed that the Fed officials are leaving room for possible interest rate hikes by the end of the year (currently not expecting to make any changes). Meanwhile, further uncertainty in the Brexit as both EU and UK leaders agreed to a “flexible” Brexit extension until 31st of Oct. The Shanghai Composite Index and Hang Seng Index declined 1.60% and 0.93%, respectively, while Nikkei 225 rose 0.11%.

Meanwhile, sentiment on the local front was negative; the FBM KLCI dipped 0.93% to 1,624.23 pts dragged by Tenaga. Market breadth turned negative with 620 decliners outpacing 275 advancers. Market trade volumes stood at 3.58bn, worth RM2.27bn. We noticed most of the construction and building material stocks underwent profit taking activities.

Despite slight optimism on the trade front, where China agreed to open its cloud computing sector to foreign companies, Wall Street trended mixed as investors traded on a cautious tone ahead of the releasing of US corporate earnings. Also the Brexit deadlock situation continues to dampen the sentiment on the stock markets. The Dow and Nasdaq slipped 0.05% and 0.21%, respectively, while S&P500 traded flat.

TECHNICAL OUTLOOK: KLCI

The FBM KLCI has breached below the support of 1,626 forming the third time of lower low formation over the past one year. The MACD Indicator has expanded negatively, but the RSI and Stochastic oscillators are suggesting that the key index is oversold. Nevertheless, the key index is likely to stay on the negative trend, unless the key index surges above the resistance around 1,650. Support will be pegged around 1,600-1,614.

We believe the negative sentiment could be overdone at this juncture and may warrant a tehcnical rebound on the FBM KLCI. Meanwhile, with the green light given on ECRL, trading activities on the construction-related stocks are likely to increase over the near term. Besides, we see potential upside on building material (steel and cement related), at least for the near term on the back of this news flow.

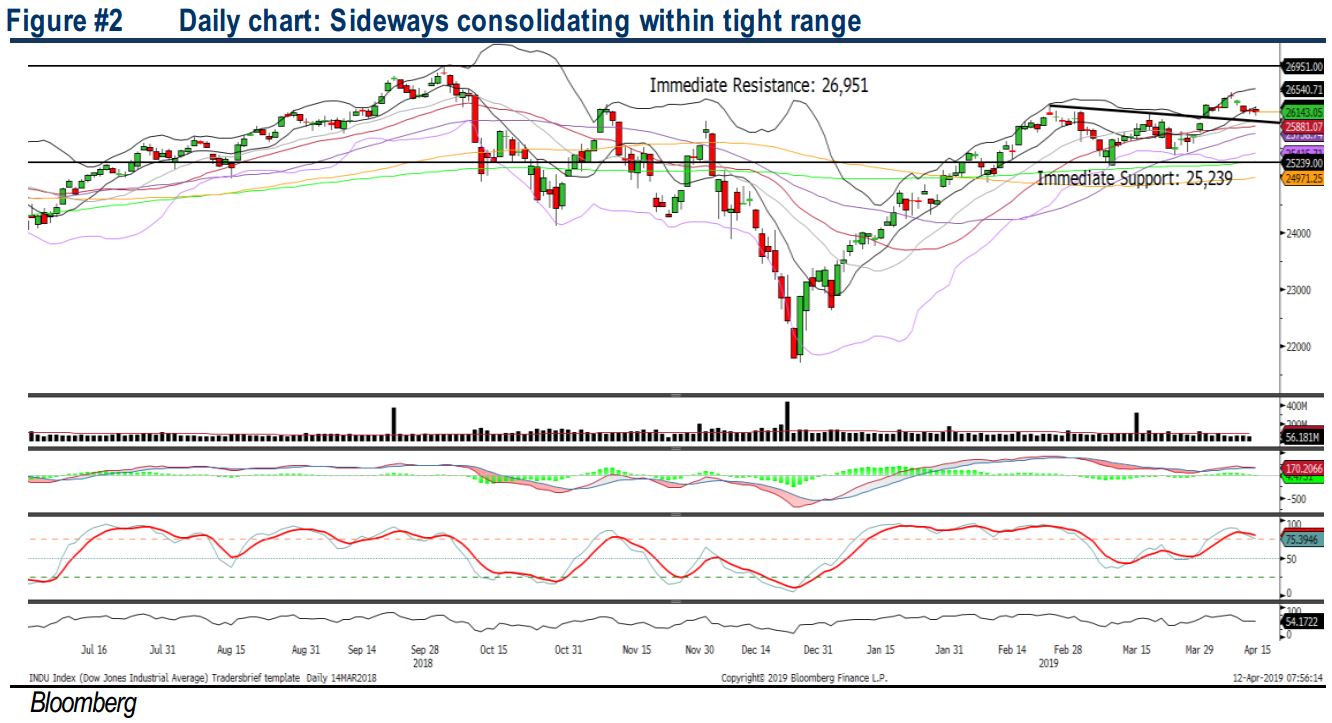

TECHNICAL OUTLOOK: DOW JONES

The Dow continues to trend sideways over the past two weeks. The MACD Indicator has turned flattish, while the stochastic oscillator is overbought. Meanwhile, the RSI is hovering above 50. As most of the indicators are suggesting mixed signals, we believe the Dow may further consolidate between the 26,000-26,500 levels over the near term. Should the Dow violates below the 26,000, next support will be at 25,239.

Without any fresh impetus in the markets, especially on the trade developments between the US and China, we opine the upward move is likely to be limited. Market participants will be focusing on the upcoming US corporate earnings in order to reassess the business performances and the outlook by the corporates. At this juncture, the Dow’s resistance will be located around 26,500-26,951.

TECHNICAL TRACKER: CYPARK

Beneficiary of positive regulatory framework to boost RE. We are positive on Cypark given its steady 10% FY19-21 EPS CAGR following the commissioning of the 20MW waste-to energy (WTE) and large-scale solar one & two (LSS1&2) plants. Cypark plans to bid for a capacity of 100MW (expect to generate RM50-60m revenue pa) in the LSS3 scheme and it is well positioned to score the job, in view of its cost leadership in RE and high success rate in the past two LSS schemes. We like Cypark for: (i) cheap valuation at 9.1x FY20E P/E (9.8% and 31% below its 3Y mean and peers), (ii) improving net margins; (iii) healthy earnings visibility with the inclusion of the two RE projects in the pipeline; (iv) well positioned for LSS3 scheme and (v) defensive play amid external headwinds as >90% of its projects are based in Malaysia (it has ~RM600m order book and RM1bn tender book).

Source: Hong Leong Investment Bank Research - 12 Apr 2019

More articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

3

BFM Podcast

5

BFM Podcast

6

BFM Podcast

7

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....