HLBank Research Highlights

Tex Cycle Technology - Values Resurface After Recent Selldown

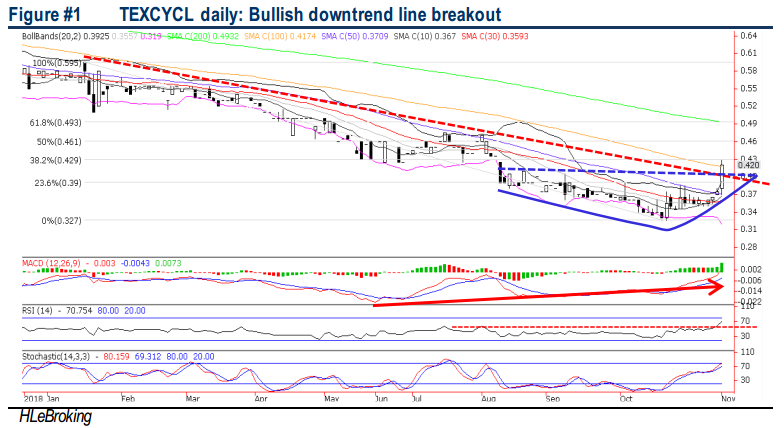

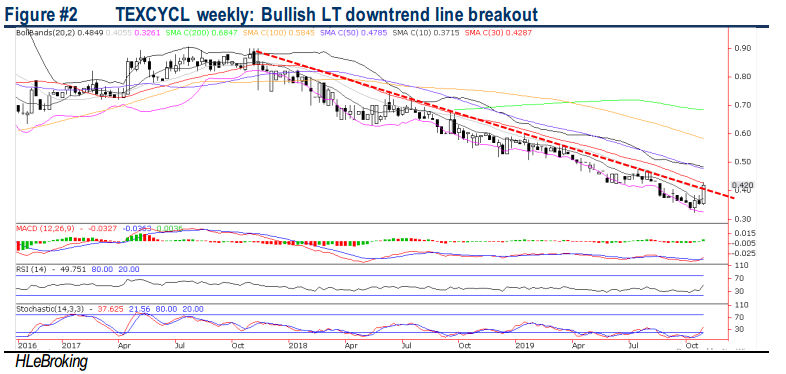

TEXCYCL’s outlook is bright, supported by its bread-and-butter waste management division as well as the eventual kick-start of its Teluk Gong and UK Renewable Electrical Energy Plant (REEP). Moreover, the potential listing to the Main Market would provide TEXCYCL to access to a wider pool of institutional investors and enhance its reputation. After tumbling 28% from YTD, valuation has become more palatable at 16x trailing P/E (vs peers’ 33x) and 1x P/B (10Y average of 1.6x). Technically, the stock is poised for further advance towards RM0.46-0.535 levels after staging a bullish daily and weekly downtrend line breakouts last Friday.

From trash to cash. TEXCYCL (listed in July 2005) is primarily engaged in an environmentally friendly waste management and recycling business that collects soiled rags, cotton fabrics, rubber, gloves, activated carbon and wood, mainly from the E&E, engineering, automobile, oil & gas and printing industries. It also supplies specialized products for the defense industry and further endow chemical products for oil & gas, agro-cultural and chemical related industries. Basically, most of the scheduled wastes collected for treatment are naturally bio degradable, consisting of cotton fabrics, rubber, activated carbon and wood. These wastes, when decontaminated, will be manufactured into fuel pellets which may be consumed as a renewable energy fuel source.

Source: Hong Leong Investment Bank Research - 7 Nov 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 1 of 1 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-11-15 16:40:00

TURTLE SYSTEM 55

5 Mins

BUY

2024-11-15 16:30:00

EMA 5

30 Mins

BUY

2024-11-15 16:25:00

EMA 5

5 Mins

BUY

2024-11-15 16:25:00

ADX

5 Mins

BUY

2024-11-15 16:25:00

TURTLE SYSTEM 20

5 Mins

BUY

Apps

Top Articles

1

3

4

BFM Podcast

6

BFM Podcast

7

BFM Podcast

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

speakup

fund waiting to exit

2019-11-07 15:12