HLIB ‘overweight’ on O&G Sector; Bumi Armada, Wasco and Velesto Top Picks

Date:

2023-12-19

Firm:

HLG

Stock:

Price Target:

0.71

Price Call:

BUY

Last Price:

0.66

Upside/Downside:

+0.05 (7.58%)

Firm:

HLG

Stock:

Price Target:

1.27

Price Call:

BUY

Last Price:

1.04

Upside/Downside:

+0.23 (22.12%)

Firm:

HLG

Stock:

Price Target:

0.25

Price Call:

BUY

Last Price:

0.19

Upside/Downside:

+0.06 (31.58%)

Firm:

HLG

Stock:

Price Target:

3.07

Price Call:

BUY

Last Price:

1.84

Upside/Downside:

+1.23 (66.85%)

KUALA LUMPUR (Dec 18): Hong Leong Investment Bank (HLIB) Bhd has maintained its "overweight" call on the oil and gas (O&G) sector, as the research firm anticipates that oil price will persist within the range of US$85-US$80 per barrel in 2024.

The projection is premised on ongoing production cuts by the Organization of the Petroleum Exporting Countries, aimed at preemptively addressing potential reduced demand stemming from economic uncertainties until at least mid-2024, increased risk premium on crude oil due to geopolitical uncertainties, diminishing supply growth from the US and restocking drive from the US Strategic Petroleum Reserve.

“Our Brent Crude oil forecast for 2024/2025 remains at USD85/80 per barrel. Downside risks to our projections include (i) reactivation of spare capacity from Opec in the near-term, (ii) de-escalation of geopolitical conflicts, (iii) China’s slower-than-expected oil demand growth and (iv) further deterioration of global economic conditions in 2024,” it said in a note on Monday.

At the time of writing, Brent crude oil was trading up 0.69% to US$77.08 per barrel.

Despite the recent pullback in oil price to US$75 per barrel, HLIB views that sector fundamentals and outlook remain intact, especially for oil and gas services and equipment (OGSE) players, which are well-positioned to ride on the ongoing upstream capex upcycle.

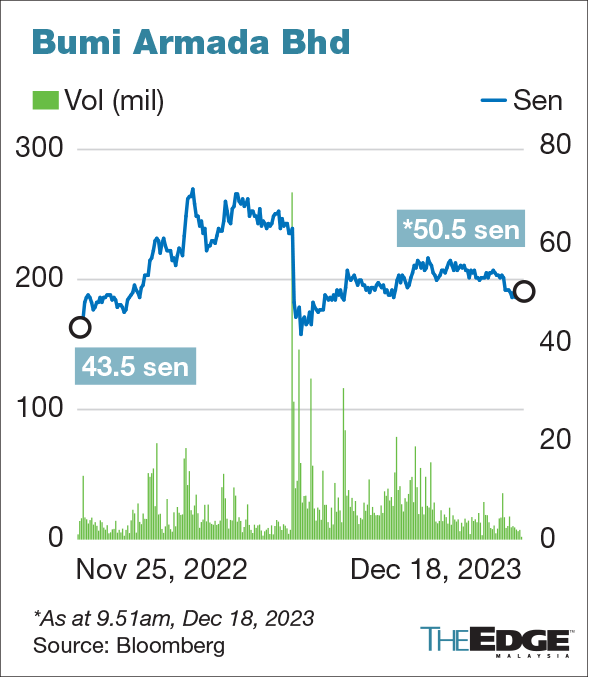

The research house selected Bumi Armada Bhd as its top pick — assigning a "buy" call and target price (TP) of 71 sen — due to the group’s favourable outlook for floating production storage and offloading players.

Additionally, Bumi Armada has an undemanding valuation — forward price-earnings (PE) of five times based on the forecasted earnings for the financial year ending Dec 31, 2024 (FY2024) — in anticipation of bumper earnings in FY2024 as contribution from Armada Sterling V sets in.

It also favours Wasco Bhd (previously known as Wah Seng Corp Bhd) for the group’s niche expertise of being one of the only few pipe coaters in the world, which is well-positioned to capitalise on the rising demand for pipe coating services spurred by ongoing O&G upstream capex upcycle. It has a "buy" call and TP of RM1.27 for the stock.

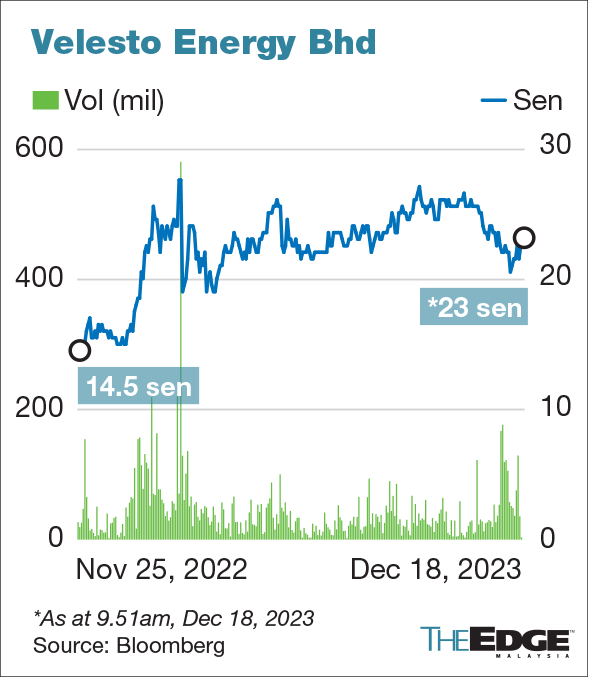

“We replace Hibiscus (‘buy’; TP: RM3.07) with Velesto (‘buy’; TP: 25 sen) as one of our top picks in view of the latter’s expected strong earnings growth in the coming quarters attributed to robust utilisation and charter rate of its JU (jack-up) rigs,” HLIB added.

At the time of writing, Bumi Armada’s share price slipped half a sen or 0.98% to 50.5 sen, giving it a market value of RM2.99 billion. Velesto rose 2.22% to 23 sen, valuing it at RM1.85 billion.

Wasco was last traded on Friday at RM1.02 with a market capitalisation of RM790.39 million.

Source: TheEdge - 19 Dec 2023

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Dragon Leong blog

2

Stock Market Enthusiast

Feng Shui Market Outlook for FBM KLCI in the Year of the Wood Snake (2025)

3

Stock Market Enthusiast

3 Resilient Stocks That Defied Malaysia’s Market Slump in January 2025 - #GCB, #ABMB, #CDB

4

The Alpha Trader

5

Kenanga Research & Investment

Oil & Gas - Dissecting Petronas and Trump's Impact on the Sector (OVERWEIGHT)

6

Rakuten Trade Research Reports

7

TA Sector Research

8

MQ Market Updates

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....