ATTA: Excellent Quarter, Low PE of 5.63, Forgotten Steel Stock

ATTA: Excellent Quarter, Forgotten Steel Stock, PE 5.63

Background:

This company operates in three segments: manufacturing, which is engaged in the manufacturing of metal-related products; trading, which is involved in trading of metal-related products, and others, which is engaged in letting of industrial and commercial assets and provision of management consultancy and corporate services. In Malaysia, the Company's areas of operation is the manufacturing and trading of metal related products.

Recent quarters;

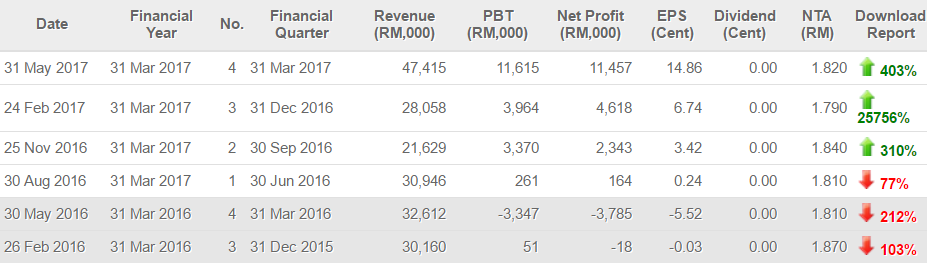

Steel counters have been registered very good profit and this company is no exception. This company registered improvement quarter by quarter and today announced quarter registered a whopping EPS 14.86 without any one off gain.

Rolling 4 quarter EPS: 20.77

PE: 5.63

NTA:1.569

ROE:13.24

DY:7.83

Par value:1.0

At current price of 1.17, its PE only 5.63. Let's do the math by applying only PE of 8. The price would be 1.66. What if they would register consistent quarters of EPS 7.5 (discount of half lower than latest quarter of 14.86) moving forward. With PE 8 and total four quarters of EPS 7.5, price would be 2.40. There is no guarantee but what I am trying to say is it has huge potential.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

Discussions

Be the first to like this. Showing 14 of 14 comments

They benefit from raising steel price. As long as the price is good, they should be doing well.

2017-05-31 22:38

@probability is right. It is from other operating income. I believe it is ICULS. Next quarter will be back to low figure.

2017-05-31 23:07

@gohkimhock refer to A4 Segmental Reporting in quarter report, other operating income is around 20% of total net profit, the rest is from real manufacturing income. I give discount of 50% from latest EPS still get valuation of 2.40.

2017-05-31 23:50

but latest EPS is dominated by other income, without other income net profit is very much lower, even lower than your 50% discount.

2017-06-01 00:30

There's a big contribution from 'other income' lah. Until management clarifies what is this, whether they are recurring or not is anybody's guess.

2017-06-01 05:58

The increased in profit mainly contributed by other operating income already happened 3 quarters continuosly. Don't believe you can see these yourself.

4th 2017

The Group made profit before tax of RM11,615 Million for current quarter compared to profit before tax of RM3,963 million for the preceding quarter. The significant increase in profit mainly contributed by higher profit margin in manufacturing segment and other operating income.

3rd 2017

The Group made profit before tax of RM3,964 million for the 3rd quarter ended 31 December 2016 compare to profit of RM0,051 million for the preceding year corresponding quarter The increased in profit mainly contributed by metal recycling division and other operating income.

2nd 2017

The group made profit before tax of RM3.370 Million for current quarter compared to profit before tax of RM0.261 million for the preceding quarter. The increased in profit mainly contributed by other operating income.

So conclusion, sustainable lah.

2017-06-01 07:33

full year wise, other income contributed a huge huge portion of its pbt. should we be worry about that?

2017-06-01 08:19

Earning dilution by the LA, WB, WC and EOS is HUGE.

Atta only 94 million shares, but outstanding LA alone is already 184 million (conversion at 1.00) !

2017-06-01 10:02

1LA+90Sen cash can convert to 1 mother share...The nominal face value of the LA is 10sen ..

2017-06-02 14:16

Hi allwin, thanks for the great write up. Would wb or La be a better buy? Altho La has greater volume today, wb seems to be less volatile.

2017-06-02 21:12

Hi AnnH, La would be better buy now. Both very much depends on mother price. Both volumes high and can be volatile. I won't rule out got shark so apply tight stop/cut loss if you are in.

2017-06-03 07:54

Post a Comment

Featured Posts

Latest Videos

.png)

Apps

Top Articles

1

https://dividendguy67.blogspot.com

2

Stock Market Enthusiast

CIMB: Uptrend Continues - Is the Best Yet to Come? (Uptrend + Bullish) - KingKKK

3

https://dividendguy67.blogspot.com

4

Good Articles to Share

Pacific leaders remove Taiwan from communique after China complaint

5

https://dividendguy67.blogspot.com

6

Good Articles to Share

Harris calls Trump cemetery visit disrespectful 'political stunt'

7

Good Articles to Share

Thousands of Australians without power as heavy rain, damaging winds lash Tasmania

8

Good Articles to Share

Five Ukraine-launched drones downed in Russia's Tver region near Moscow, governor says

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

probability

Current Net Profit margin seems unrealistic...may not be sustainable

2017-05-31 22:25