Big Croc That Rob Bursa - Who Are They?

富达公司兵败如山倒,季度亏损4千4百万,内情揭秘。Losses widen. Protasco Bhd (5070) loss -RM44mil in 4Q, QoQ -5,473.91%, YoY -614.54%. What is Exceptional items?Truth unveil.

CrocCaptured

Publish date: Thu, 28 Feb 2019, 09:45 AM

CrocCaptured

0 9

When you though you were “diverted” to look at right, you forgot the elephant on the left. Who is the big elephant in Protasco Bhd self-gratification drama?

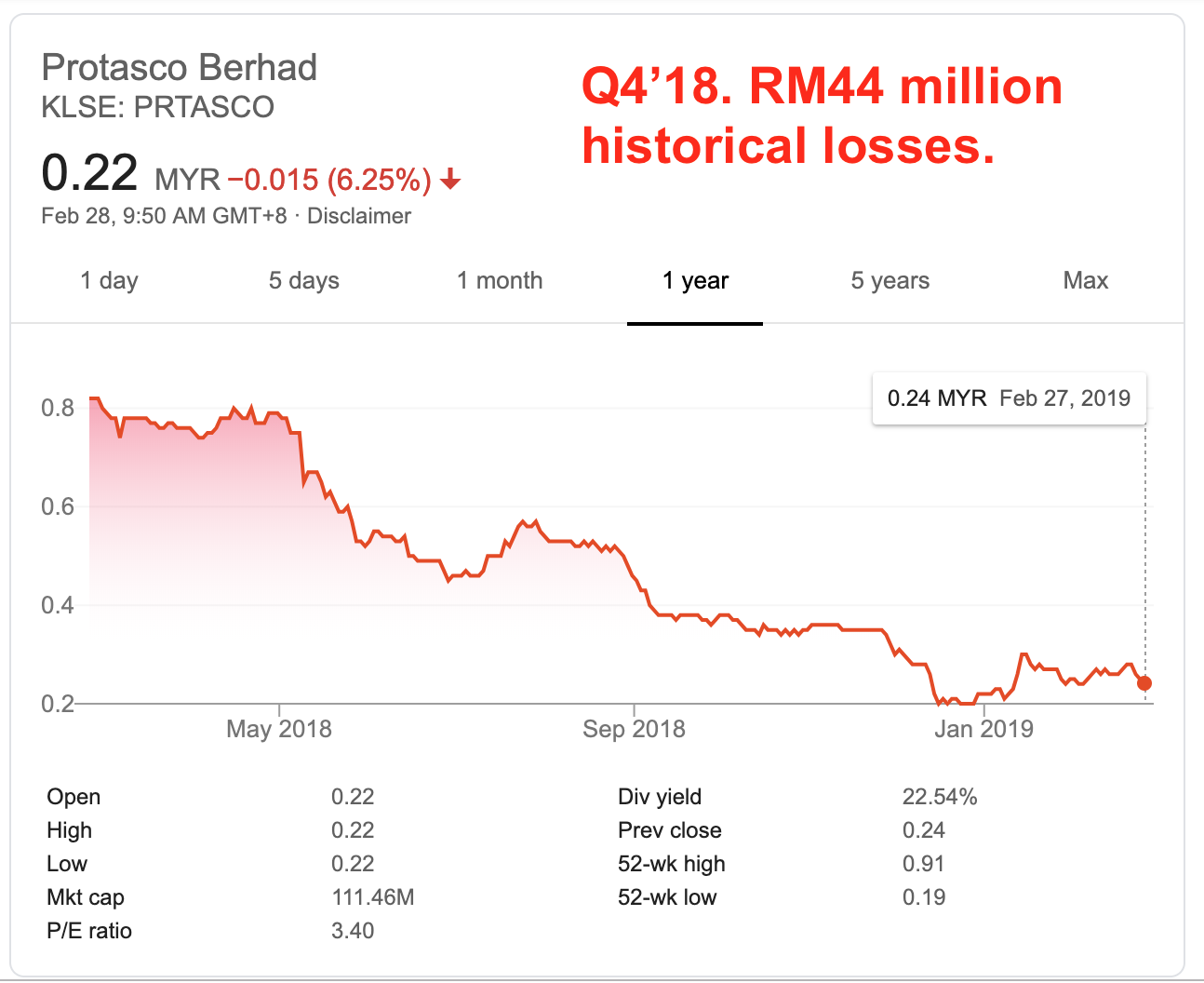

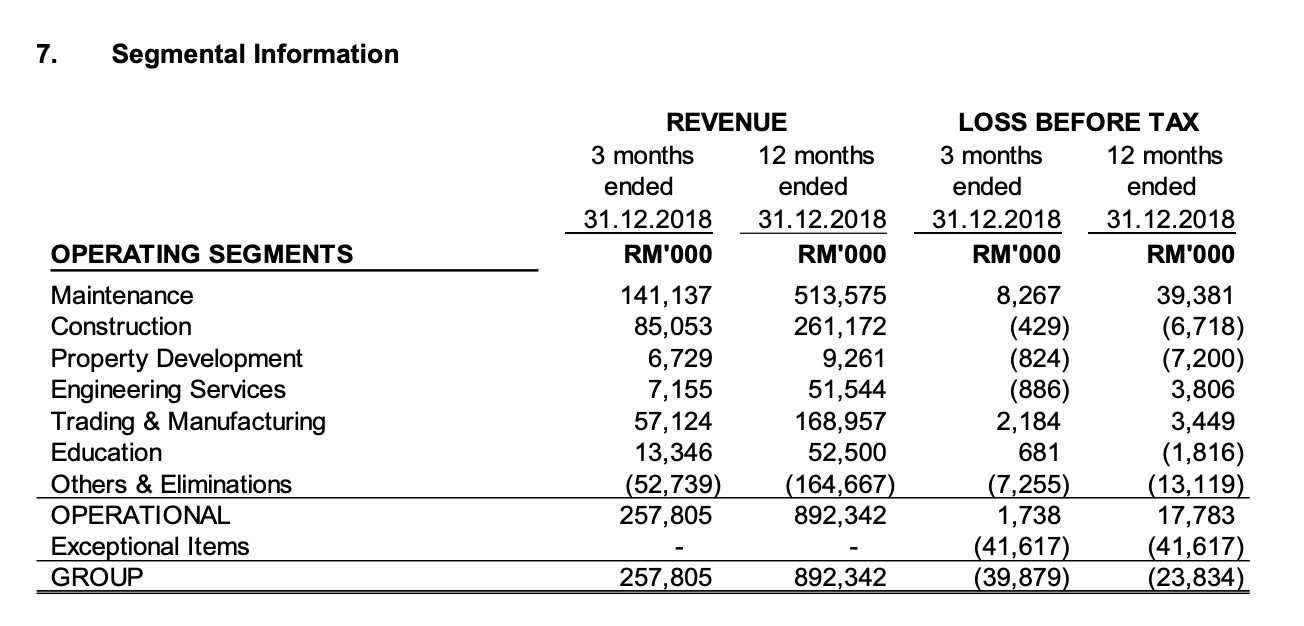

27 February 2019, Kajang, Selangor - Protasco Bhd (5070), the road maintenance oligopoly legacy left over from former government suffers another huge quarterly losses under current management supervision, lead by Group Managing Director Dato' Sri Chong Ket Pen.

The losses widen to -RM44,647 million in 4th quarter, or comparable QoQ -5,473.91%, YoY -614.54%, the worst financial quarter and total disaster caused by current management team. Protasco Bhd senior management and board of directors fees trippled from RM3mil to over RM10mil since the year 2014, which is the highest paid civil servant taking salaries from the people of Malaysia thanks to the passive caretaker role riding on JKR road maintenance contracts.

Financially "Engineered Profit" Evidence Cover Up

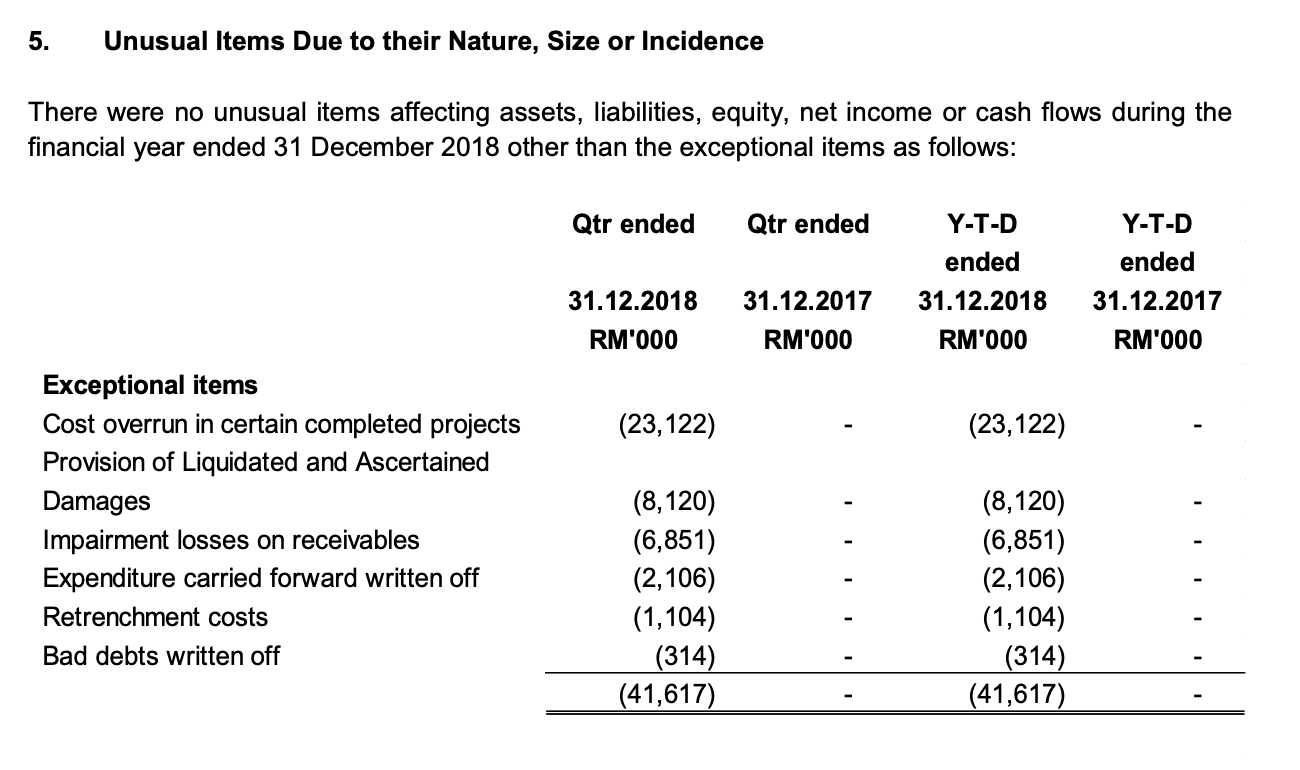

Most perculiar in this latest financially engineered quarter report is the "Exceptional items". What is hidden inside the Exceptional items that Chong Ket Pen's management trying to cover up? According to the notes in the latest quarterly report item number 5 especially the "Cost overrun in certain completed projects", the cover up seems to be fooling MIA, Bursa Malaysia and Securities Comission, as well as SPRM and IRB all together on 1 particular failure - PPA1M camouflage. Here are the items:

Assume that Protasco for the sake of reporting a "profit" to justify bank-borrowing to pay dividend, had overlooked the "cost overrun in certain completed projects", as well as "Provision of Liquidated and Ascertained Damages", plus "Impairmet losses on receivables" and "Ependiture carried forward written off", bundled with "Retrenchment costs", etc, resulted in RM41.617 million of unusual loss items. These material losses where impact is more than 5% of earlier quarterly reporting difference, may trigger Bursa Malaysia and SC alert and reprimant on all Protasco bhd directors for careless in reviewing the suspected false quarterly report. Such false report were resulted in higher bank borrowing and paid out RM25 million dividends in the year 2018 (evidence in next paragraph).

Wishfully, such cover up might fool the ordinary investors, but not the authorities. What do you think?

Financially "Engineered Dividend" Evidence Exposed

The Construction business is Protasco Bhd's current management desperate idea to proof themselves not a failure in running other business except being crown as civil servants taking care of JKR road maintenanc contracts. To fulfil one man's plan to make Construction Business his own legacy, dubious PPA1M contracts were signed and huge construction loan from UOB Bank was obtained. The result of such is the chance for Protasco Bhd management to get close for former Prime Minister, Dato' Sri Najib bin Tun Razak in hope to secure further road maintenance contracts. In deed, the lost making PPA1M show project paid off, with the secure of RM4.2 billion JKR contract on 4 April 2018, or 1 months before Malaysia General Election.

The supposedly "lost making" PPA1M project turns "profitable" in the year 2016 and 2017, with sophisticated payments paid to sub-contractors, suspected transfer pricing and accounting massage which magically spring out "profits" on the account. This "profits" becomes the excuse for Protasco Bhd to borrow more bank money and paid the cash out through "Dividends", and the cash magically landed in major shareholder's coffer - Dato' Sri Chong Ket Pen to be more precise.

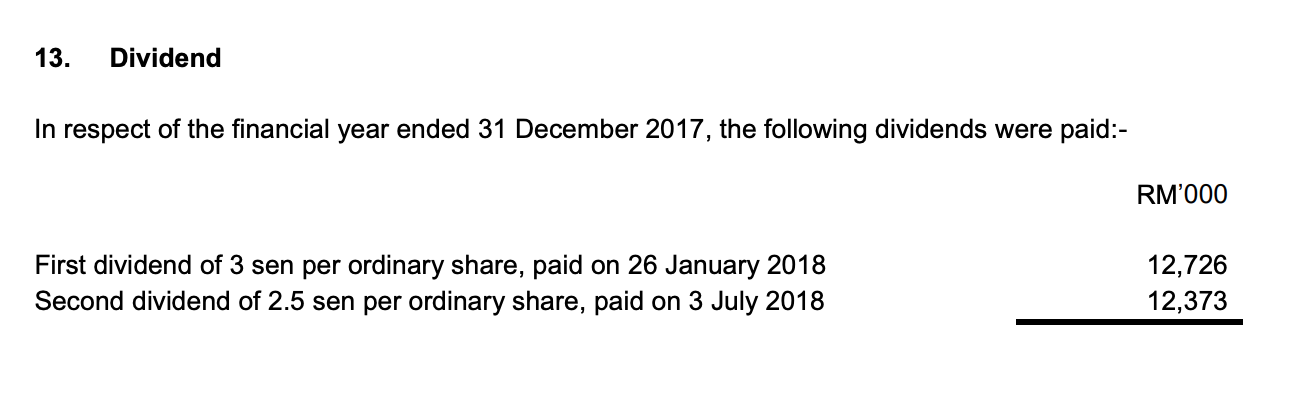

The financial engineering impact took place in the year 2014 and lasted until the year 2018, evidence from this quarterly report notes No.13 as follows:

While the company suffer huge losses, earlier financially engineered "profit" numbers fooled everyone and Protasco paid out RM25,099 million so called dividend, which suspected "half" went to substantial shareholder.

The "Cost overrun in certain completed projects" of RM23,112 million compared to the RM25,099 million "Dividend" looks bizarre as if the money siphoning exercise took place on 1:1 match!

Fake Profit > Bank Loan > Dividend > Write Off?

Such questionable cash looting exercises raises alarming issue in the Malaysia corporate governance standard. The rusty governing system inherited from former government where law makers are not up to par to spot and procecute potential sophisticated corporate crime, giving birth and space for such corporate hooligans to repeatedly raking (illegal) personal gain at the cost of public shareholders and the people of Malaysia.

Except Road Maintenance, Chong's are Total Losers

The Chong's era, means after the year 2014 and spill over to February 2019 today, count Dato' Sri Chong Ket Pen and his 3 sons Chong Ther Nen, Chong Ther Shen, and Chong Ther Vern were brought in and are still sitting inside Protasco Bhd apparently not delivering any results except burdening Protasco Bhd management cost.

Here are various sectors the Chong's finger prints are all over, except self-automated Road Maintenance sector:

According to Bursa Malaysia, UOBM Nominees pledged securities account of Penmacorp Sdn Bhd, an investment holding company belonging to Chong Ket Pen, his wife Datin Hoo Chit Neo, and their sons Chong Ther Nen, Chong Ther Zern, Chong Ther Shern and Chong Ther Vern.

In March 2013 Chong suddenly emerges as the substantial shareholder of 28% through series of share purchase using margin loan, notably from UOB Bank. The need to find money to cover share margin loan is obviously seen in series of money-taking schemes. The financially engineered "profits" during the year 2015-2017 followed by bank-borrowed dividend; Chong Ket Pen's RM4.2 million yearly salary rise from RM600k per year before he dramatically took Protasco board control; as well as sudden lost of profit margin in Road Maintenance business suspected under probe for transfer pricing, are among the obvious evidence. Road maintenance business margin is unlikely to have material change considering the industry nature, where the amount of money paid out in tens of millions every year went "un-noticed". At least in the eyes of certain authorities.

Disaster Outcome - Sinking Assets and Share Plunge

The investors were fooled, so as the authorities. Protasco Bhd share price plunges from RM2.10 at the peak (before split), to RM0.19 at recent low.

With the management fees as shown in latest quarterly report still the same, and the losers still running the show inside Protasco Bhd, the company is as good as circus operated by clowns. The real motive and objective of Chongs which cost Protasco Bhd’s unfortunate fall, might be just started to unfold.

What can public investors do about it despite the obvious being exposed?

As for those who held tight to the "(fake) dividend stock", since you already bought the ticket and there is nothing you can do about it, just enjoy watching the monkey show burning your money in the circus. Don't worry, the senior management are well paid. To artificially support share price, they will keep buying Protasco shares using the (ill-gotten) money.

= FInancial Number Crunch =

SUMMARY OF KEY FINANCIAL INFORMATION

|

|

INDIVIDUAL PERIOD

|

CUMULATIVE PERIOD

|

||||

|

CURRENT YEAR QUARTER

|

PRECEDING YEAR

CORRESPONDING QUARTER |

CURRENT YEAR TO DATE

|

PRECEDING YEAR

CORRESPONDING PERIOD |

||

|

31 Dec 2018

|

31 Dec 2017

|

31 Dec 2018

|

31 Dec 2017

|

||

|

$$'000

|

$$'000

|

$$'000

|

$$'000

|

||

| 1 | Revenue |

257,805

|

286,116

|

892,342

|

939,277

|

| 2 | Profit/(loss) before tax |

-39,879

|

24,993

|

-23,834

|

70,327

|

| 3 | Profit/(loss) for the period |

-41,527

|

12,976

|

-37,029

|

46,423

|

| 4 | Profit/(loss) attributable to ordinary equity holders of the parent |

-44,647

|

6,578

|

-48,548

|

28,063

|

| 5 | Basic earnings/(loss) per share (Subunit) |

-9.02

|

1.55

|

-9.81

|

6.62

|

| 6 | Proposed/Declared dividend per share (Subunit) |

0.00

|

3.00

|

2.50

|

3.00

|

|

AS AT END OF CURRENT QUARTER

|

AS AT PRECEDING FINANCIAL YEAR END

|

||||

| 7 | Net assets per share attributable to ordinary equity holders of the parent ($$) |

0.6735

|

0.9336

|

||

Definition of Subunit:

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Big Croc That Rob Bursa - Who Are They?

富达公司 vs SAPURA 能源 。EPF指标可靠吗?Protasco Bhd vs Sapura Energy Bhd. EPF finger print bullet proof?

Created by CrocCaptured | Dec 08, 2017

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-09 16:40:00

EMA 5

5 Mins

BUY

2025-01-09 16:40:00

ADX

5 Mins

BUY

2025-01-09 16:10:00

EMA 5

5 Mins

SELL

2025-01-09 16:00:00

ADX

5 Mins

SELL

2025-01-09 16:00:00

TURTLE SYSTEM 20

5 Mins

SELL

Apps

Top Articles

1

THE INVESTMENT APPROACH OF CALVIN TAN

US 60% TARIFF ON CHINA: CHINA FDI INTO MALAYSIA & INDONESIA WILL BENEFIT THESE STOCKS, Calvin Tan

2

Mercury Securities Research

3

Good Articles to Share

Tariff policy done well can help grow the economy, GOP senator says

4

M+ Online Research Articles

JB-SG Special Economic Zone (JSSEZ): 1+1 > 2: Harnessing the Multiplier Effect

5

Mercury Securities Research

6

Mercury Securities Research

7

Good Articles to Share

It appears TikTok could really get shut down, says Jim Cramer

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....