KCTrader's Blog

Gloomy or Hopeful Hibiscus?

Due to the hike in interest rate that causes Brent Oil price to drop, with addition to the current KLSE selloffs, Hibiscus is one of the stocks that has received a huge beating. Uncertainties, worries of recessions, possible lower demand for commodities, China lockdown, undoubtedly Hibiscus won't be able to survive on its previous support line. We have seen about 20% drop in share price in the past few weeks, so the question now is, does Hibiscus still have potential to go up? Let's see...

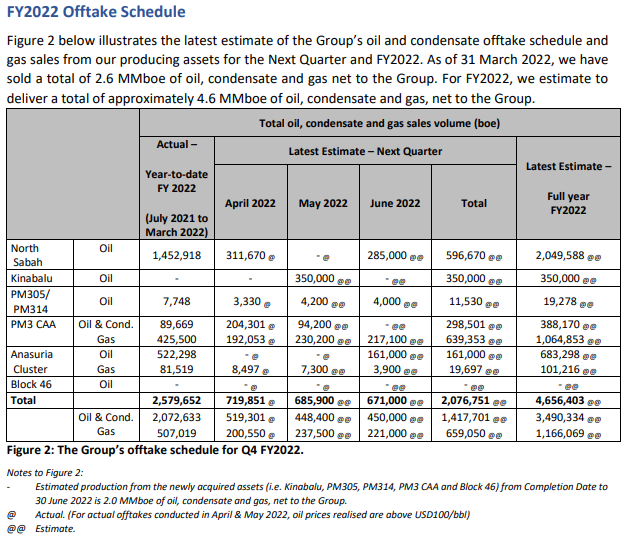

If we see from this table as provided by Hibiscus, if it happens to be about 80% accurate, assuming JUST FOR THE OIL that will be sold in this upcoming quarter, which amounts to 1,417,701 barrel of oil. To be CONSERVATIVE, let's assume they will be able to sell about 1,134,160 barrel, on an average oil price of USD109 over the price of 3 months oil, that'll be about USD124mil. To convert, let's take a conservative rate about USD4.3, that'll be almost RM533mil in revenue itself, about 80% increase in revenue. For this I haven't include the amount of gas sold, and all figures above are purely conservative.

As for profit I think it would be very subjective as there are many OPEX to be included, hence I'll take the average historical profit margin %, about conservative 18% P.M. We would see a net profit about RM95million, a 96% increase compared to Q2FY22. As for YoY%, we can see an increase of 111% and 92% on both revenue and profit respectively.

Note, all these amount are super conservative due to unexpected circumstances, and not including the gas that will be sold. Hence, is the future of Hibiscus gloomy, or hopeful?

#Hibiscs #5199

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on KCTrader's Blog

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

.png)

MQ Trading Signals

Time

Signal

Duration

Type

2024-09-26 16:00:00

OBV

Hourly

SELL

2024-09-26 15:00:00

OBV

30 Mins

SELL

2024-09-26 09:05:00

EMA 5

5 Mins

SELL

2024-09-26 09:00:00

EMA 5

Hourly

SELL

2024-09-26 09:00:00

EMA 5

10 Mins

SELL

Apps

Top Articles

1

AmInvest Research Reports

2

3

Rockstone Investment

Binastra Corp Bhd – A Promising Investment in Construction in 2025

4

save malaysia!

5

8

CEO Morning Brief

China Probes Calvin Klein Parent Over Suspected Xinjiang Boycott

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....