Is Ranhill still worth investing?

Is Ranhill still worth investing?

The company had announced their full year result for financial year 2021, and I must say is not the best number but not the worst as well.

On a quarterly basis, top and bottomline performance had a huge jump yoy but I suspect is due to a low base effect. However, on a full year basis, its bottomline result was mediocre.

According to a shareholder’s email to the management and was told mainly due to “HQ overhead and Corporate sukuk interest expenses”. (you may check on the comment section)

That said, I trust the overall declining profit could potentially reach its bottom. Moving forward, I believe its profit would be on an uptrend mainly driven by contribution from its services segment and better overall sentiment from the recovery from Covid-19.

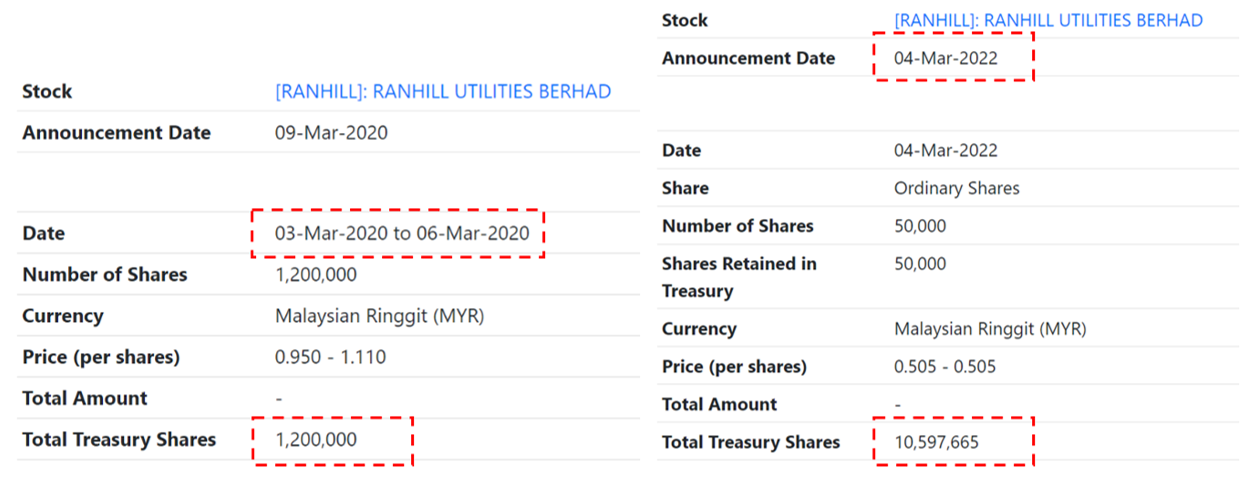

On top of that, the company had been consistently buying back its shares (roughly about 9 million shares) since the beginning of the first MCO in March 2020 till March 2022. A huge positive indication, suggesting the management remains very bullish towards the company’s future prospect.

Underlying opportunities

Here’s a recap on the potential catalysts that are still in play:

- Source to tap water supply in Indonesia - Increasing Ranhill source to tap water by almost 40%

- Future / ongoing RE tender projects - Potential future bidding for projects such as LSS, WTE, geothermal

- Completion of Sabah East-West Transmission line - Improve their utilisation, hence better economies of scale

- New NRW projects from other states - Leveraging their track records and strong competency in NRW technologies and skill

- A natural ESG selection - The current major investment group (the likes of your EPF, PNB, KWAP) focus heavily on ESG – and Ranhill business nature is strategically focus on that

- High oil price potentially benefiting Ranhill Worley - The current oil barrel price is hovering around USD100, which potentially lead to more jobs / business activities from upstream O&G companies

- Macroeconomics conditions improving - The reopen of the economy would provide other business sectors to slowly resume operational at higher capacity, which would translate better job opportunities to Ranhill in terms of infrastructure / construction works

Technical point of view

On the technical side of things, it seems the price has bottom out. In terms of risk reward, this could potentially present a good opportunity for traders or long-term investors to have some position in their portfolio. However, this is not a financial advice – just my personal opinion.

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Dragon Leong blog

2

save malaysia!

3

Follow Kim's Stockwatch!

4

5

save malaysia!

6

save malaysia!

7

Good Articles to Share

The 'Fast Money' traders share the stocks they are thankful for this holiday season

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....