Kenanga Research & Investment

Daily technical highlights – (POHUAT, EG)

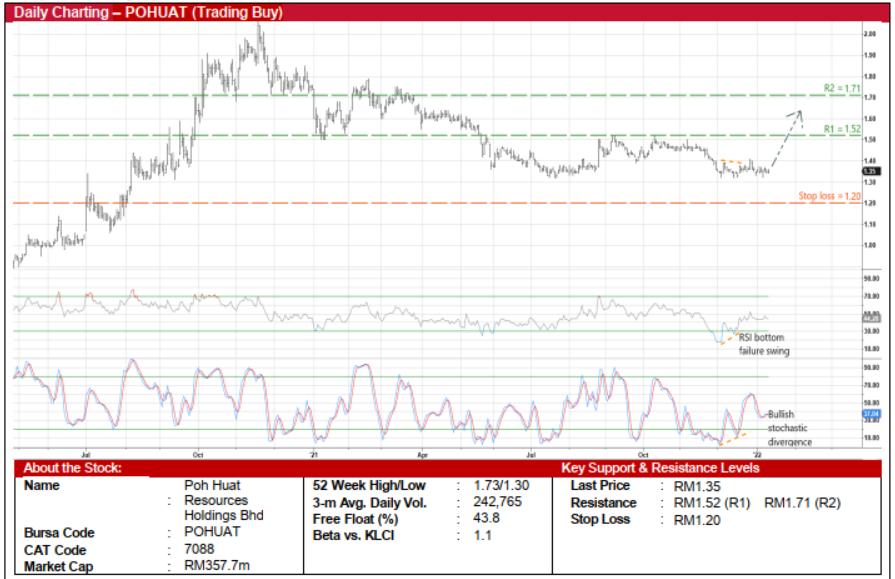

Poh Huat Resources Holdings Bhd (Trading Buy)

• POHUAT’s share price is set to break away from a tight sideways trading range based on recent positive technical signals.

• Essentially, the presence of a RSI bottom failure swing and a bullish stochastic divergence pattern – as both indicators have formed rising bottoms in the oversold area while the stock was drifting listlessly – suggest an upward shift is on the cards.

• On the way up, the stock could climb towards our resistance thresholds of RM1.52 (R1) and RM1.71 (R2), implying upside potentials of 13% and 27%, respectively. Our stop loss price level is seen at RM1.20 (or an 11% downside risk).

• Business-wise, POHUAT is one of the leading furniture manufacturers and exporters in South East Asia, making both office furniture and home furniture from its manufacturing bases in Malaysia and Vietnam.

• With a customer base in more than 30 countries, the group derives the bulk of its sales from the US and Canada markets (which contributed approximately 76% and 20% of FY20’s total sales, respectively).

• As the group’s sales proceeds are predominantly billed in USD, POHUAT is a net beneficiary of a strengthening USD against the Ringgit.

• For FY October 2021, POHUAT posted net profit of RM32.2m (-38% YoY) as its performance was hit by the Covid-19- triggered prolonged lockdowns, which in turn had disrupted the group’s manufacturing operations in Malaysia and Vietnam.

• Nonetheless, the worst is probably over as consensus is forecasting a rebound in net earnings to RM54.7m in FY22 and RM60.9m in FY23. This implies undemanding forward PERs of 6.5x this year and 5.9x next year, respectively.

• Its balance sheet is in a financially stable position with net cash & short-term investment holdings standing at RM146.4m (or 55.2 sen per share which translates to ~40% of the existing share price) as of end-October last year.

EG Industries Bhd (Trading Buy)

• After clearing a descending trendline that stretches back to February last year, a trend reversal may be already in progress for EG shares as the stock could break away from a symmetrical triangle pattern.

• With the stochastic indicator climbing out from an oversold territory and the momentum indicator on the rise from the zero line, this could lift the shares towards our resistance targets of RM0.67 (R1; 15% upside potential) and RM0.77 (R2; 32% upside potential).

• We have placed our stop loss price level at RM0.50 (or a 15% downside risk from its last traded price of RM0.585).

• Fundamentally, as a leading Electronic Manufacturing Services (EMS) and vertical integration provider for global brand names of consumer electronic and data storage products for several industries (such as ICT, medical, automotive and telecommunications), EG offers full turnkey solutions for completed final products assembly (box-build), printed circuit board assembly and modular components assembly.

• Following its announcement in May 2021 to manufacture complete box-build 5G routers in a venture with a US-based customer, EG is well-positioned to benefit from the global 5G network rollouts.

• Earnings-wise, after registering net profit of RM14.0m in FY June 2021 (a turnaround from the net loss of RM13.6m in FY20), the group posted net earnings of RM1.9m (-56% YoY) in 1QFY22.

Source: Kenanga Research - 12 Jan 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Kenanga Research & Investment

Bond Weekly Outlook - MGS/GII likely to rise amid ongoing US economic resilience

Created by kiasutrader | Nov 22, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

2

4

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

5

6

7

BFM Podcast

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....