Some snippets:

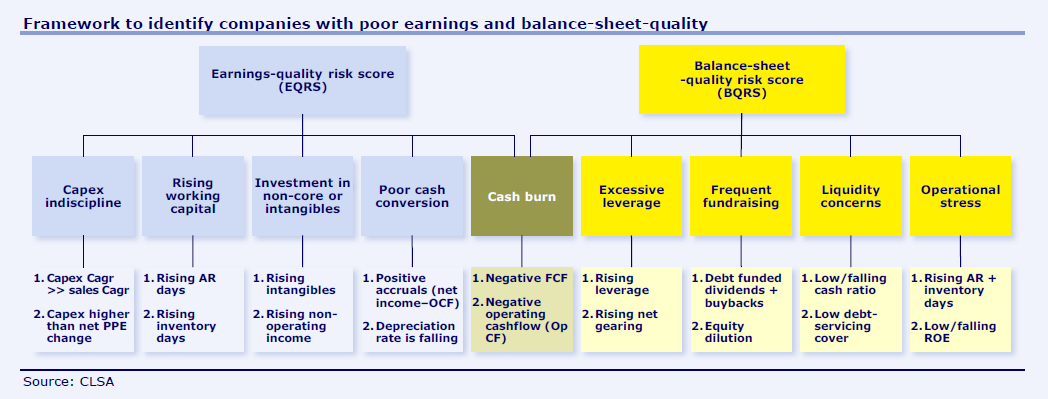

One of the long-term themes that we have discussed at length is the strength of Asian balance sheets and how this manifests into a growing dividend culture among corporates with substantial cash hoards. While these companies steal the limelight, there are also a growing number that stay under the radar while trying to succeed through unconventional means. Sadly, this is further fuelled by a new breed of analysts whose imagination doesn’t stretch beyond quarterly forecasts and analysis that mirrors company guidance. Over the past decade, cases of accounting manipulation have multiplied, and this year, the proportion of value destroyers in Asia has also reached an all-time high of 38%. In the current low-return environment, avoiding such accounting blow-ups overwhelms all other considerations. With capital preservation becoming the focus, we create our earnings-quality and balance-sheet-quality risk scores, using ideas from the CLSA U Blue Book on forensic accounting, titled Financial fingerprints.

This report highlights two sets of scores including the earnings-quality risk score (EQRS) and balance-sheet-quality risk score (BQRS), which use 10 financial indicators each to identify issues related to earnings and balancesheet quality. Our backtests show that companies with high EQRS scores have underperformed by 7% per annum since 2000, while those with high BQRS have underperformed by 18% per annum.

Ownership issues add to the complexity as Asia is marred by an unusually high insider-holding ratio (53% on average), which could lead to numerous instances of related-party transactions as majority shareholders retain strong management control. High government ownership is also common, and while such companies are less likely to enter bankruptcy, they are dominated by value destroyers.

Companies flagged under the EQRS score are:

- Olam (SG), "Consistently negative FCF with high debt"

- Gamuda (MY), "Companies with rising inventory days"

- Yanlord (SG)

- Yinson (MY)

AirAsia (MY) was flagged under the BQRS score.

Separately, companies flagged under a single criteria where:

- Noble Group (SG), "Companies with diverging profit and cashflow"

- Petronas Chemicals, "Capex indiscipline"

- Sembcorp Ind (SG), "Dividends funded through debt"

- Maxis (MY), "High and rising leverage"

- Malaysia Airports (MY), "Value destroyers with high government ownership"

- Golden Agri (SG), "Value destroyers with high insider holding, low independence"

- SapuraKen (MY), "Key management changes over last one year"

Needless to say, a single indicator might not mean that much, the company has to be analysed in its totality. Also, the above companies are from the universe that CLSA tracks, in general the larger listed companies in Asia. The fact that a company is not mentioned doesn't mean anything, CLSA might not track it.

sell

Trading in any stocks is done very fast. If need to analyse stocks using above criteria better place money in FD.

2015-09-04 06:37