Mercury Securities Research

Malayan Cement (3794) - Best Proxy to Construction Boom

MercurySec

Publish date: Thu, 26 Sep 2024, 11:01 AM

MercurySec

0 512

An official blog in i3investor to publish research reports provided by Mercury Securities Research team.

All materials published here are prepared by Mercury Securities Sdn. Bhd.

Mercury Securities Sdn. Bhd.

L-7-2, No.2, Jalan Solaris,

Solaris Mont Kiara, 50480, Kuala Lumpur

Tel: 603-6203 7227

Email: mercurykl@mersec.com.my

All materials published here are prepared by Mercury Securities Sdn. Bhd.

Mercury Securities Sdn. Bhd.

L-7-2, No.2, Jalan Solaris,

Solaris Mont Kiara, 50480, Kuala Lumpur

Tel: 603-6203 7227

Email: mercurykl@mersec.com.my

Stock Highlights

Vibrant construction activities. MRT Corp’s recent public display for the MRT 3 Circle Line signals a potential revival of the RM45bn mega project, adding to other existing large-scale infrastructure projects like the Penang LRT, Penang Airport expansion, and the speculated KL-Singapore High-Speed Rail. These developments are expected to further boost the construction sector, which has also seen strong job flows related to data centres and semiconductor industry from the private sector.

Cement players to benefit. MCement likely to benefit the most as it is the largest cement producer in Peninsular Malaysia, holding a 60% market share. The current situation is quite reminiscent of the 2011-2013 period when large-scale infrastructure projects (such as KLIA2, LRT extension, and MRT1) drove significant re-ratings of cement players. Although the sector subsequently underperformed due to price wars resulting from massive capacity expansion, we argue that current industry dynamics are more favourable now following the merger between Malayan Cement and YTL Cement since 2019. The recent strengthening of the Ringgit would also help a lot to lower USD-denominated key input costs for cement production, such as coal.

Still has leg to run. Based on consensus forecast (which we think has room for upward revisions), MCement is currently trading at 18.4x fully-diluted CY25 P/E (dilution from ICPS). We believe this has yet to fully reflect the sector’s upturn and premium for being Malaysia’s largest cement producer. Historically, MCement’s valuation has traded up to 20-22x forward P/E (+1 SD) during previous upcycles. With positive newsflows from the construction sector and strong earnings delivery, we believe it is just a matter of time before the stock re-rates further.

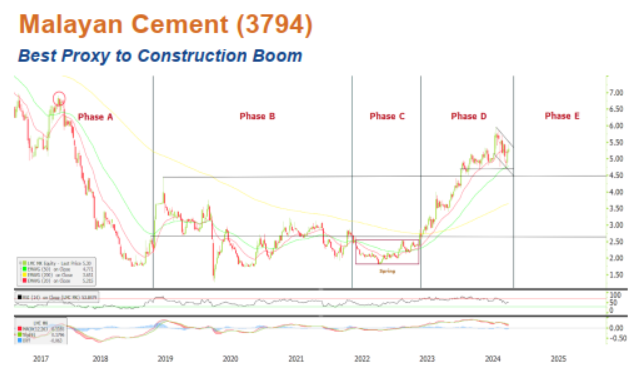

Classic Wyckoff accumulation pattern. The stock is in the final stages of Phase D, with resistance breached and increased volume, indicating a potential move to Phase E for a stronger uptrend. The current support level is RM4.71, a critical zone where the stock has bounced back multiple times. Additionally, a bull flag has formed, suggesting further bullish momentum. The first resistance at RM5.47 coincides with the bull flag’s resistance, and a breakout here could lead to a sharp rally. On the downside, a break below RM4.54 could trigger a correction to RM3.67, where high volume has previously locked in in this zone.

Source: Mercury Research - 26 Sept 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Mercury Securities Research

Kawan Renergy (0307) - Potential Breakout Beyond Resistance Zone

Created by MercurySec | Jan 22, 2025

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

3

4

HLBank Research Highlights

5

CEO Morning Brief

Bangkok Urges People to Work From Home as Air Pollution Worsens

6

CEO Morning Brief

US Bonds Rise as Tariff Respite for China Eases Inflation Fears

7

CEO Morning Brief

New World Offers US$15 Bil for Loan Collateral as Stress Grows

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....