British-American Tabacco(BAT) is one the world largest tobacco manufacturer penetrating more than 60 markets worldwide. With such a gigantic network, the company is able to leverage on economic scale upon manufacturing all the products. This put BAT ahead of its competitors in terms of company size and cost saving advantages. Despite launches of e-cigarettes products, the adaptation of traditional cigarettes is still maintained and hence no harms are done by technological advancement to the industry. Aside of that, not much innovations are needed for the tobacco industry in order to survive. Furthermore, BAT controls heavy-weight international brand such as Pall Mall and Dunhill which have well established brand positioning to the existing consumers. This leads to repetitive sales and directly contributes to the company's revenue.

From the paragraph above, I evaluated the ability of the company to generate growing revenue in the future. When we change our perspective to the humane side, we know deep down that smoking is harmful to not only our own body but also to the surrounding including mother nature due to minorities' addiction. Hence, the company need to spend a tremendous amount of money in corporate social responsibility each year to recover the damages by smoking.

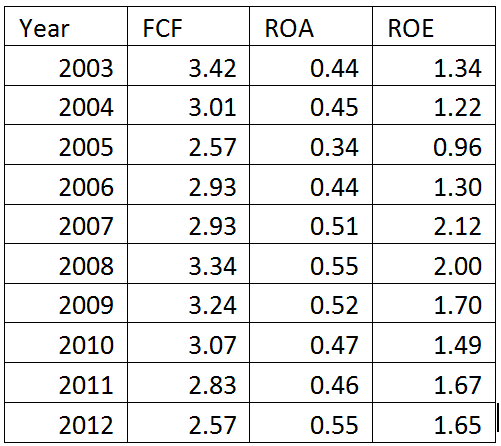

According to the free cash flow in the past ten years, the current year level is lower than 3.42 level in 2003. With strict government regulations, cigarettes prices are deemed to be increased year by year where it should reflect a higher cash inflow but instead, failure to raise cash inflow is a big concern to me. Besides that, the company includes RM400 million worth of goodwill inside its balance sheet representing 30% of total assets where it is not impaired for even a single time in the past ten years. Surprisingly, book value to current market price is (60.8/1.31=46) where to me, it is extremely overpriced. In short, this company is operationally fine but I don't see too much good through its financial performance with substantial movement within the cash flow.

Stock: BAT Code: 4162