Airasia - Time to Buy Now

Airasia - Time to Buy Now!

Revisit back to past independent analysis report Davidtslim, Airasia does has a big tremendous opportunity to hit TP 6.00 or beyond (+ include upcoming dividend payout of AAC 75sen & Expedia 11sen payout). With current slight USD vs RM strengthen, dividend payout money from sell-off BBAM of total USD$1.085 Billion cash out earning will increase to 85sen & above (if time by current rate 4.07, AA shareholder will get RM4.41 Billion cash)

Even after post AAC & Expedia dividend payout by end 2018, Airasia right now is moving toward big corporate structure change to become the First NET CASH airline company in the world with lower finance cost (low cost maintenance to maintain airline after sell to BBAM), dividend policy of 20%, higher revenue from airline fleet expansion, ancillary income (digitalization) & online good purchase. With current low share price, Airasia definitely is a good undervalued, strong financial & rapid growth low-cost airline company in the world that have huge potential growth in 2018 & beyond.

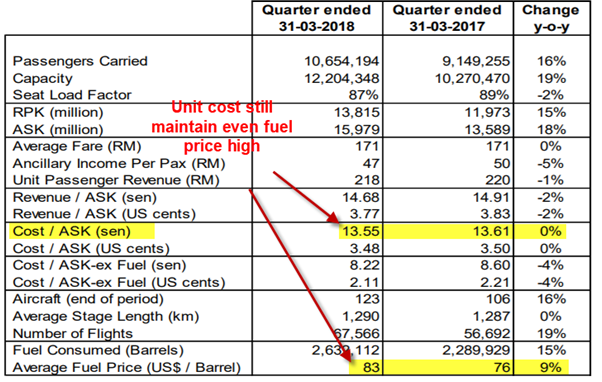

In term of investors worry of high jet fuel price effect on Airasia profit; actually investor are over-worry. Airasia mgmt. have ways to mitigate the fuel cost by increasing its carried capacity (more aircrafts, more available seat, lower cost per unit). If to relook onto comparison of 1Q18 & 1Q17 financial report in term of Cost/ASK (sen) vs Average fuel price (US$/Barrel), there is no cost increase wherease in fact Cost/ASK (sen) reduce from 13.61sen to 13.55sen even through average fuel price/barrel had increased from $76 to $83 (increased 9%). For more detail, please refer to attached link to better understanding.

--------------------------------------------------------------------------------------------------------------

Be a smart investor NOT an emotional investor!

Happy Investing!

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Discussions

1 person likes this. Showing 5 of 5 comments

oh easy ma. ask tf the ticket price put high as mas then get more profit lo..

2018-08-12 07:18

The author seems to want to focus on the real thing, so I say as below:

1. Expenses is increasing at a faster pace than revenue.

2. The world has changed (to be more honest), but TF hasn't.

3. While most subsidiaries still unprofitable, Airasia wants to venture into building airports again. I believe selling most of that businesses and focus in principal activity is the right move. Airasia was in the right direction (since 8501) for about two years and now going in multiple direction again.

4. Now is August 2018, the special dividend of RM0.82 to RM1.02 supposed to be distributed this month, however it is unlikely to be materialized. (A lot of) people has been waiting for close to three years.

5. Efficiency is a comparative thing, and also a continuous process. Airasia is slowing down....The moment you stop to be creative, your share price stop too....

2018-08-12 10:57

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-10 15:50:00

EMA 5

5 Mins

BUY

2025-01-10 14:35:00

EMA 5

5 Mins

SELL

2025-01-10 12:15:00

EMA 5

5 Mins

BUY

2025-01-10 12:00:00

ADX

5 Mins

SELL

2025-01-10 11:15:00

EMA 5

5 Mins

SELL

Apps

Top Articles

1

Kenanga Research & Investment

Technology - Export Restrictions and Tariff Threats (OVERWEIGHT)

2

Initial Public Offering (IPO)

3

Good Articles to Share

CEOs are 'overall optimistic' on US economy under Trump: Boston Consulting Group

4

5

THE INVESTMENT APPROACH OF CALVIN TAN

US 60% TARIFF ON CHINA: CHINA FDI INTO MALAYSIA & INDONESIA WILL BENEFIT THESE STOCKS, Calvin Tan

6

Good Articles to Share

7

RHB Investment Research Reports

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

ivy88_

Good to recalled back on past AA analysis report. That's true. If investor patience, we will reward handsomely per Warren Buffet's invest strategy.

2018-08-10 12:19