AmInvest Research Reports

Stock on The Move - SDS Group

AmInvest

Publish date: Thu, 10 Nov 2022, 09:10 AM

AmInvest

0 9,374

An official blog in I3investor to publish research reports provided by AmInvest research team.

All materials published here are prepared by AmInvest. For latest offers on AmInvest trading products and news, please refer to: https://www.aminvest.com/eng/Pages/home.aspx

Tel: +603 2036 1800 / +603 2032 2888

Fax: +603 2031 5210

Email: enquiries@aminvest.com

Office Hours

Monday to Thursday: 8:45am – 5:45pm

Friday: 8:45am – 5:00pm

(GMT +08:00 Malaysia)

All materials published here are prepared by AmInvest. For latest offers on AmInvest trading products and news, please refer to: https://www.aminvest.com/eng/Pages/home.aspx

Tel: +603 2036 1800 / +603 2032 2888

Fax: +603 2031 5210

Email: enquiries@aminvest.com

Office Hours

Monday to Thursday: 8:45am – 5:45pm

Friday: 8:45am – 5:00pm

(GMT +08:00 Malaysia)

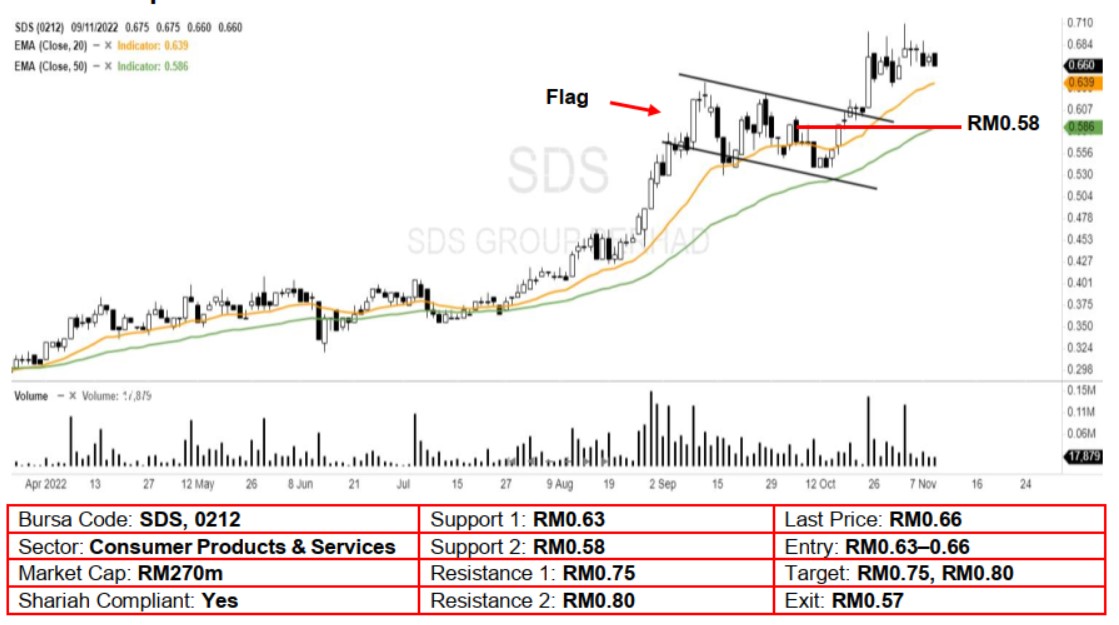

Technical Analysis. We believe the buying interest for SDS Group is back after it pushed out from the bullish flag pattern with a long white candle on 25 October. With the stock trading near its all-time high, supported by its rising EMAs, likely indicates that the upward momentum may be picking up. A bullish bias may emerge above the RM0.63 level, with a stop-loss set at RM0.57, below the 50-day EMA. Towards the upside, the near-term resistance level is seen at RM0.75, followed by RM0.80.

Company Background. SDS Group Berhad and its subsidiaries are primarily involved in the manufacturing and retailing of bakery products since 1984. It grew from its Johor homebase throughout Peninsular Malaysia with its 3 brands, namely the retail brand “SDS” and two wholesale brands, “Top Baker” and “Daily’s”.

Prospects. (i) Retail segment: Expanding in the Central Region of Peninsular Malaysia for new retail outlets and upgrading its online store and platform to offer a wide range of products (ii) Wholesale segment: Growing its geographical footprint and logistic fleets across Malaysia with new distribution centres - currently the wholesale distribution network is covering 10 states in Peninsula Malaysia. (iii) The R&D arm of the group continues to introduce new F&B offerings to meet customers’ tastes and expectations.

Financial Performance. In 1QFY23, the group posted a higher revenue of RM60.9m (+53.1 YoY) with a net profit of RM4.5m (11x YoY) due to higher influx of customers (re-opening of borders between Malaysia and Singapore) and same-store sales growth. In FYE22, the group recorded a healthy revenue growth of RM198.3m (+14.1% YoY) with a PAT of RM10.6m (+46% YoY). This was mainly attributable to the increase of footfall in the retail channel and increased of demand for wholesale channel.

Source: AmInvest Research - 10 Nov 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on AmInvest Research Reports

Banking - Limited sector ROE expansion with moderated earnings growth

Created by AmInvest | Nov 18, 2024

UOA REAL Estate Investment Trust - Lower occupancy rate for Menara UOA Bangsar

Created by AmInvest | Nov 15, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-11-20 16:50:00

EMA 5

5 Mins

BUY

2024-11-20 16:50:00

ADX

5 Mins

BUY

2024-11-20 16:50:00

TURTLE SYSTEM 20

5 Mins

BUY

2024-11-20 11:00:00

EMA 5

Hourly

SELL

2024-11-20 11:00:00

TURTLE SYSTEM 20

Hourly

SELL

Apps

Top Articles

1

2

3

save malaysia!

4

5

7

8

AmInvest Research Reports

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....