AmInvest Research Reports

Stock Idea - CARIMIN PETROLEUM

AmInvest

Publish date: Fri, 12 Jan 2024, 10:18 AM

AmInvest

0 9,502

An official blog in I3investor to publish research reports provided by AmInvest research team.

All materials published here are prepared by AmInvest. For latest offers on AmInvest trading products and news, please refer to: https://www.aminvest.com/eng/Pages/home.aspx

Tel: +603 2036 1800 / +603 2032 2888

Fax: +603 2031 5210

Email: enquiries@aminvest.com

Office Hours

Monday to Thursday: 8:45am – 5:45pm

Friday: 8:45am – 5:00pm

(GMT +08:00 Malaysia)

All materials published here are prepared by AmInvest. For latest offers on AmInvest trading products and news, please refer to: https://www.aminvest.com/eng/Pages/home.aspx

Tel: +603 2036 1800 / +603 2032 2888

Fax: +603 2031 5210

Email: enquiries@aminvest.com

Office Hours

Monday to Thursday: 8:45am – 5:45pm

Friday: 8:45am – 5:00pm

(GMT +08:00 Malaysia)

Company Background. Carimin Petroleum (Carimin) is an oil & gas service provider specialising in onshore/offshore major maintenance and hook-up & commissioning services. The group’s core business segments are: (i) construction, hook-up & commissioning, and topside major maintenance (CHUCTMM), (ii) manpower, and (iii) marine services. It deploys marine vessels such as work barges, accommodation vessels, crew boats and anchor handling tug supply vessels. The group also provides sub-sea underwater inspections, repair, maintenance works and services for the oil & gas industry.

Prospects. (i) Global prospects of the oil & gas industry remains optimistic. Domestically, major oil companies are initiating an increasing number of tenders, reflecting Petronas' positive outlook, (ii) Kemaman yard is set to be completed by 1QFY24, allowing for the execution of projects with enhanced cost efficiencies and increased capacity, and (iii) Venturing into sub-sea activities is expected to yield a positive earnings contribution, given associated higher margins. To recap, Carimin entered the sub-sea sector in 2019 through the acquisition of a 60% stake in Subnautica Sdn Bhd.

Financial Performance. In 1QFY24, Carimin reported higher revenue of RM84.7mil (+7.2% YoY) with a PAT of RM8.6mil (+22% YoY). This was mainly due to higher activities from topside major maintenance works for a gas cluster under the maintenance, construction, and modification (MCM) services as well as third-party services contributing growth within the CHUCTMM division.

Valuation. Based on Carimin’s 1QFY24 annualised net profit, the stock is trading at an attractive 2024F P/E of 6.4x, which is lower than its 5-year historical average of 12x and Bursa Energy Index’s 5-year forward average of 14.6x. As a comparison, Icon Offshore, involved in oilfield services & equipment, trades at a much higher FY24F P/E of 12.5x.

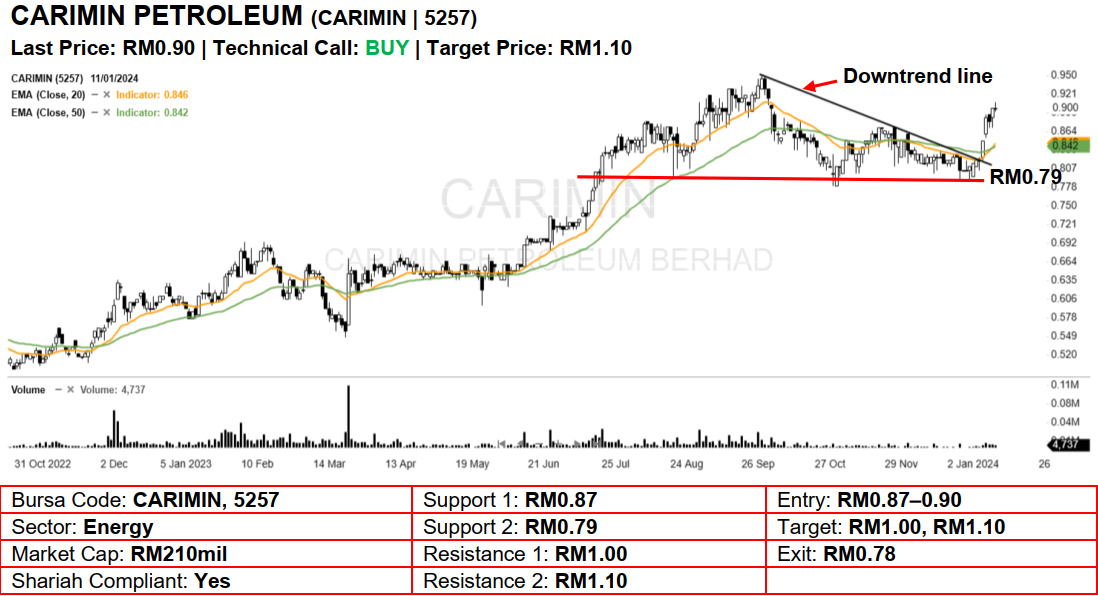

Technical Analysis. We expect further upside for Carimin given that it took out the 3.5-month downtrend line a few sessions ago. As the 20-day and 50-day EMAs have established a bullish crossover lately, the current upward momentum may persist in the near term. A bullish bias may emerge above the RM0.87 level, with stop-loss set at RM0.78, below the 50-day EMA. Towards the upside, nearterm resistance level is seen at RM1.00, followed by RM1.10

Source: AmInvest Research - 12 Jan 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on AmInvest Research Reports

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-10 08:00:00

EMA 5

Daily

SELL

Apps

Top Articles

1

Kenanga Research & Investment

Technology - Export Restrictions and Tariff Threats (OVERWEIGHT)

2

Good Articles to Share

CEOs are 'overall optimistic' on US economy under Trump: Boston Consulting Group

3

4

Good Articles to Share

5

RHB Investment Research Reports

6

Good Articles to Share

7

Good Articles to Share

8

Good Articles to Share

Indonesia, Japan leaders agree to boost defence, energy ties

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....