Intelligent Investing

APM Automotive Holdings: The rule of minimum valuation

Most valuation methods such as DCF, DDM etc are designed to answer the question "How much is the company worth?".

Whereas the rule of minimum valuation, or debt capacity valuation, seek to answer a different question - "What is the minimum value the company must worth?". Rather than finding out how much a business should worth, this valuation establish a 'floor'. Rather than making predictions, this valuation finds protection.

But what can be used to establish the 'floor'? - Corporate Bond.

Corporate bond is a type of debt instrument that's available to company to raise money through issuing debts to bondholders. Just like how company can borrow from banks or issue shares. Bondholders are generally being promised of a fixed percentage of interest payment over the length of the bond, plus the principal payment when it matures.

Bond is considered safer than stock because of its predictability and stable income but in exchange of that, bondholders is only eligible to receive a fixed interest payment and have a fixed, or limited claim of the company, i.e the principal amount.

On the other hand, stockholders have complete ownership of the entire company's assets, but bears a bigger risk (and bigger reward) because of exposure to stock market.

Now here is the kick. Because stockholders have complete ownership of the entire company, the equity cannot be less valuable than the bond which has limited claim on the same company.

If you find this a little confusing, we will use an example to illustrate.

Imagine that APM decides to issue bonds, the details are below.

Total bond market value: $455 mil

Interest rates: 5.5% p.a

Annual interest expense: $25 mil

APM plans to issue $455 mil worth of bond at an interest rate of 5.5% annually. From there, they will incur annual interest expense of $25 mil ($455 x 5.5%). Being a prudent investor, you want to make sure APM can deliver what they promise, that is paying that $25 mil to you and all other bond subcribers over the entire tenure. So you did some studies.

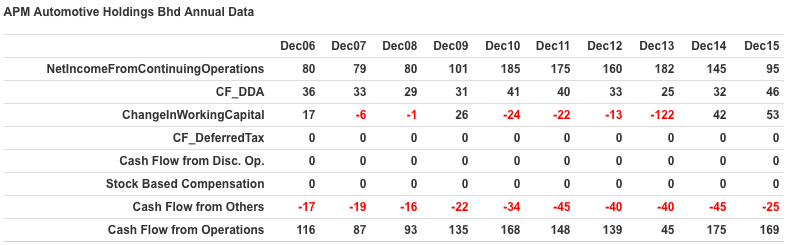

You notice over the past 5 years, average Cash Flow from Operations is $135 mil, and avg. $125 mil over 10 years. To be conservative, you decided to use $125 mil.

If APM can generate an average cash flow of $125 mil, that is 5x of the $25 mil that they promise to pay to bondholders. An interest rate coverage of 5x sounds reasonable for a cyclical industry like automotive. So that's a tick.

Next, you want to be sure the interest rate payment of 5.5% is fair to bondholders, so you dig around again. You went through APM's 2015 annual report. APM has $56 mil short term borrowings, pays $1.47 mil in interest expense or 2.6%. Not something you're really after because it is short term, but it is a good start.

You look at other company in similar industry and discover MBM Resources Bhd. They have long term borrowings at 5% interest.

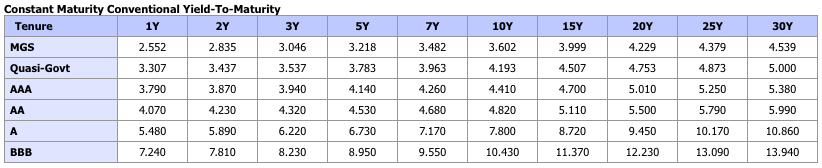

Lastly, you compare it with other types of bonds.

At 5.5%, it is higher than Malaysian Government Securities (MGS) and Quasi-Govt, even higher than entire Triple-A corporate bond yield, and sitting out at 20Y Double-A corporate bond yield.

After doing your research, you conclude that 5.5% yield is fair, APM has the capacity to take on the debt of $455 mil, meaning it would not have any problem repaying $25 mil a year to all bondholders due to its earning power of $125 mil. Which means, APM's earning power will need to deterioriate 5x before facing insolvency issue.

NOW. Stockholders have complete ownership of the entire company, therefore the equity cannot be less valuable than the bond which has limited claim on the same company. That means, APM has to worth at least $455 mil, which is the bond value.

Oh wait. While going through the annual report, you noticed APM has $56 mil of short term borrowings, and $295 mil in cash, or net cash of $239 mil.

Adding that to the bond value of $455 mil, gives you a total of $694 mil. With outstanding shares of 196 mil, that comes to $3.54 value per share, teenie weenie above current price of $3.51. You found the 'floor' price of APM.

Again, this valuation does not tell you how much APM should worth, but tells you how much it shouldn't go below.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Intelligent Investing

Discussions

Be the first to like this. Showing 16 of 16 comments

Shaun, you are right bondholders required return is fixed and lower than stockholders, and higher required return means lower equity value.

And no, equity doesnt become less valuable if a company is loaded with debts. Debt is a form of financial engineering and capital structure of a company does not affect valuation. Simple hypothesis, if APM is to borrow $700 mil today, equal to its market cap, and has to pay 5.5% interest or $39 mil a year, how much would you value APM? Zero?

And how about this, they borrow $700 mil and distribute all in special dividend, how much is APM worth again? Since you say loading debt makes equity worthless, maybe APM would have turn negative, but shareholders will get $3.55 in special dividend.

Then you are worry now, previously APM was net cash 250 mil, now after borrowing 700 mil, they are net debt 450 mil. Can APM possibly service $25 mil (450 mil x 5.5%) ? Yes, everything on the balance sheet that gives them the earning power of $129 mil a year still there. So would APM shares go to $0.00 if they borrow 700 mil?

2016-08-13 08:03

Exactly if loan doesnt create value, how would piling up debt decrease value? Im still eager for you to tell me how much APM equity should be if they borrow 700mil. Because it will be negative base on your deduction. The whole idea is for every stock, sits a safe bond within. How does one determine if a bond as safe? That has been presented on top. If apm can issue that value of bond safely, in this case 455mil, it sounds bizzare to me investors would consider current valuantion as 'unsafe'.

2016-08-13 10:28

Look, your hyperbolic 5 bil would not even make equity worth less than bond because 1. No one sane enough would approve such a debt against what apm has and 2. Bond would not come into existence in the first place.

So ure saying now you think the minimum value is less than 700m, after apm issue 700mil, it is worth 650mil, or 50mil reduction?

2016-08-13 11:40

Well Ben Graham wrote "An equity share representing the entire business cannot be less safe and less valuable than a bond having a claim to only a part thereof.” And you're not the first to disagree with him. Let me know next time if you find such scenario exist, ill be very interested to study

2016-08-13 15:57

high loan levels cannot be assumed to create value. it's very possible to destruct value when company overspend, make wrong investment decisions etc. So when the return from the investments (from loans) is lower than the interest expenses, that's when it destroys value. One of the reason behind merger acquisition arbitrage (where people long acquireee, short acquirer) is also because acquirer usually overpays and will leverage up so the pressure is on the acquirer to deliver returns that can cover the new loan expenses and generate incremental value

2016-08-13 19:10

and may I understand how you get the bond value of 455m? since this is used in your final valuation. and not to forget many academic theories assume perfect market but in reality it's not. APM may be able to raise 100m with 5.5%. but the next 100m maybe market will ask for 6% so on so forth. so it may not be as straightforward as your valuation implies. I have not seen the ben graham's quote before or anything like it. but sometimes the context in which the quote was written could be important, maybe u can share with us the topic he was discussing when he said that?

2016-08-13 19:15

You can get more here http://fundooprofessor.blogspot.com.au/2005/11/one-valuation-rule-two-paradoxes.html

2016-08-13 19:42

I think the statement in itself is misleading. in ben graham's context, the 'equity share' is referring to debt free company. so if the debt free company load itself up with debt, it's essentially the same underlying biz so there should not be any distinction between the two. this is very academic because there are a few assumptions 1) perfect market with perfect information. in reality, for highly levered company people probably prefer the bond over equity due to its security and priority claims 2) leverage recapitalisation. in ben graham's example, he essentially assumes that the debt free company takes on debts and distribute to shareholders. in reality, even if company takes on debts, they will probably keep most of it. theoretically it belongs to shareholders but they have no access over it. and when you have more cash than you need, cash slippage tend to occur

2016-08-13 22:36

I do understand the point you are trying to prove but market is often irrational. APM is relatively strong in cash generation compared to its lower earnings. using DCF, P/B or dividend model will probably also points to the company being undervalued. however PE wise it's expensive as earnings remain depressed. like many bursa companies, it is a value trap waiting for catalyst, which will be when the auto industry recovers. important question is when?

2016-08-13 23:03

Besides it is cyclical industry, you don't enter when PE is low, thats at the peak not trough

2016-08-14 03:50

of course u don't need to know if you are ok to leave your capital lying there, but I'm just suggesting. monitoring auto industry figures, upcoming launch schedules, PMI, IPI etc. these could give you a hint. but of course buy and patiently hold is another option. just my 2 cents

2016-08-15 13:01

Bollocks, the level of debt a company can take is independent of the equity value of the company. It does not represent a floor nor a ceiling level of a company's equity value

2016-09-15 21:46

of course how much debt a company can take, theoretically, is independent of EV, as long someone is willing to lent their money (where's customer yacht?). The article talks about 'safety', not the truth of floor or ceiling

2016-09-16 07:07

I suppose you mean floor when u talk about safety in the context of your write up

2016-09-17 23:14

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

2

3

TA Sector Research

4

Koon Yew Yin's Blog

5

Good Articles to Share

Le Pen makes new threat to withdraw support for French government

6

Good Articles to Share

7

Good Articles to Share

US lawmakers say Hong Kong is becoming hub for financial crime — report

8

Good Articles to Share

Global airfares set to rise yet again in 2025, Amex report says

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

shareinvestor88

APM was trading at 150 at its lowest point

2016-08-12 23:32