KlseTracker

Excel Force MSC (Defensive Yet Attractive)

Keithson Neoh

Publish date: Tue, 19 May 2015, 09:34 PM

Keithson Neoh

0 2

Disclaimer: This is a personal research that reflects personal views and opinion. The full content of this research paper, including any views or opinions presented should be treated for educational purpose only. The author shall not warrant or assume any legal liability or responsibility for the accuracy, completeness or usefulness of any information provided on this site.

Review

§ Excel Force MSC Berhad (EFORCE) is currently the market leader in Malaysia for the provision of financial services business solutions. With more than a decade of experience in offering information systems and services to the Banks and Stock-Broking Companies in Malaysia, EFORCE is the first IT Company in Malaysia to provide a total, comprehensive and market-proven business solution for the stock broking industry from Front Office to Back Office. Over the years, EFORCE have built up a considerable number of well-established Stock Broking customers as well as renowned Financial Institutions and have attained approximately 90% of stock broking Public Gallery Display System and 70% of Electronic Client Ordering System market share in Malaysia.

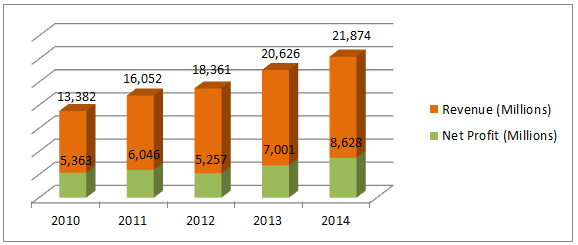

§ Eforce reported a full year FY14 Net Profit of RM8.6 million (-11.24% QOQ, +23.2% YOY). The decrease in net profit QOQ, mainly caused by the disposal of office amounting RM1.6 million (net expenses for bonus issue and warrants).

§ From previous year, Revenue rose to RM21.6 million (+5.8% YOY), mainly attributed by the increase in Application Service Provider (ASP) by RM1.61 million and Application Solution (AS) with a slight boost of RM424 K. On the other hand, Maintenance Segment revenue decreases by RM787 K.

§ Eforce revenue and profit have been growing steadily over the past 5 years in despite of the market volatility.

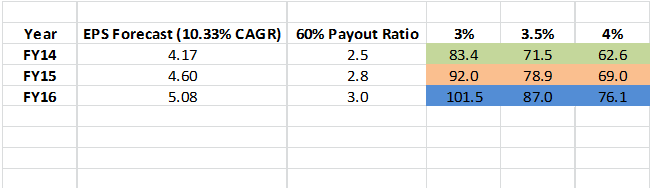

§ Eforce has been lying on a comfortable growth of average 10.33% CAGR over the past 5 years, and estimated to continue on a modest growth over the coming years.

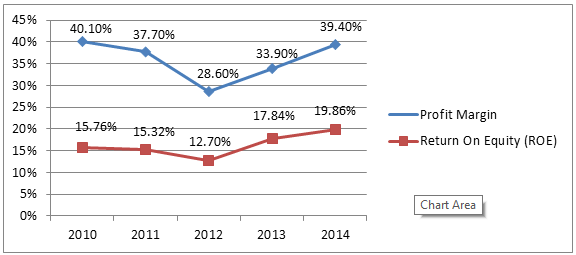

§ With an improving operational efficiency over years, EFORCE registered a 39.4% profit margin and 19.86% ROE closing FY14 with a tremendous improvement.

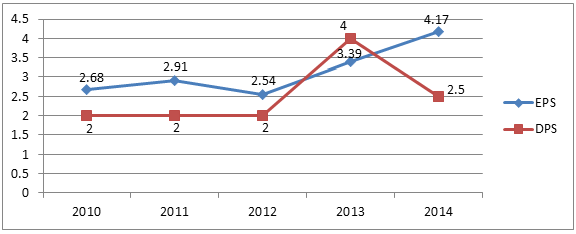

§ With the Current Payout Ratio of 60%, and DPS of 2.5 cent for FY14 the estimated Dividend Yield (DY %), is 4.1% based on current price of (RM0.605).

(EFORCE Balance Sheet, figures extracted from Annual Report)

|

Key Statistic (Millions) |

2012 |

2013 |

2014 |

|

|

|

|

|

|

Cash and Equivalent |

26.33 |

24.04 |

20.55 |

|

NCAV |

33.1 |

28.8 |

26.9 |

|

Total Asset |

47.4 |

43.5 |

54.5 |

|

Borrowings |

1.8 |

1.3 |

7.2 |

|

Shareholders Fund |

40.4 |

39.1 |

43 |

|

Book Value Per share |

0.20 |

0.19 |

0.21 |

|

Net Cash |

24.53 |

22.74 |

13.35 |

|

Total share outstanding |

206.77 |

206.77 |

206.77 |

|

|

|

|

|

|

|

|

|

|

Outlook

§ Existing EFORCE customer (Alliance Investment, Bimb Securities, Hong Leong Investment, Jupiter Securities, Kenanga Investment, Maybank Investment, Malacca Securities, Public Investment, RHB Investment, UOB Kay Hian) already captured 70% market shares of the Electronic Client Ordering System in Malaysia.

§ After a successful penetration in Thailand and Vietnam, next EFORCE will be focusing on the penetration of other Asian region (Hong Kong, Taiwan, Indonesia & China)

§ A bright prospect, as company in focus on enhancement, development, and implementation of their product to existing and new clients.

§ Eforce is sitting on a comfortable economic moat, a sustainable competitive advantage against its competitor N2N Connect.

§ Defensive business model, as changes in economic settings will not have a significant impact on company earnings.

Valuation

§ Target Price based on Dividend Discount Model Valuation

Current Price: RM0.605

Target Price 1: RM0.69

Target Price 2: RM0.79

Target Price 3: RM0.92

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on KlseTracker

Discussions

3 people like this. Showing 15 of 15 comments

set objective to be capital or dividend play for eforce.selling decision rests on the objective.a good sharing.

2015-05-19 22:04

Keithson Neoh ,did u buy alot eforce?This is your first sharing.never see u here b4..now after go up so much..u say u cover this.U never contribue here before.now u want ti be the boss!!!

2015-05-20 00:24

Rosmah, don't know don't comment. Your comments no use at all. If got please show us your calculation

2015-05-20 06:47

Good sharing. However, cash is decreasing and borrowing is increasing. Mind sharing what they use the cash and borrowing for? But overall the BS is still neat and healthy.

2015-05-21 10:31

for technology company is very common... high expenditure on R&D. especially now during their expansion period. hopefully they are able to balance their gearing ratio...

2015-07-02 23:13

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

2

My Trading Adventure 2025

3

https://dividendguy67.blogspot.com

4

Double Swords 双剑论股

5

Double Swords 双剑论股

6

Double Swords 双剑论股

7

My Trading Adventure 2025

8

Double Swords 双剑论股

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Keithson Neoh

http://klse-analytical.blogspot.com/

2015-05-19 21:37