Maybank Outlook

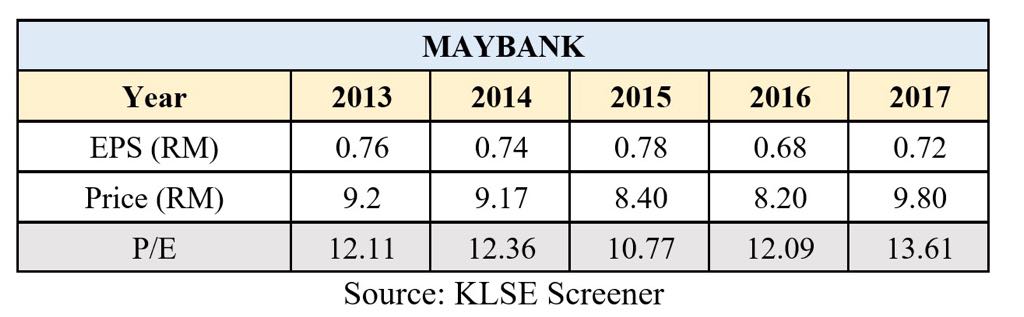

MayBank PE analysis

Towards the year 2020, Maybank has given a big priority for the bank to become digital first as they are realized the traditional banking business would be eliminated and replaced by the modern banking system with the faster and efficient service to customers. They are also expected to strengthen their current position in ASEAN across all the financial service and to become the leading retail and commercial financial services provider in ASEAN.

Maybank also have shown it potential for futhrther growth as it has been consistently reported growth in its operating revenue for the past 10 years. Its operating revenue have grown from RM15.2 billion in 2007 to RM45.6 billion in 2017. This growth is contributed by the overall growth in its net interest and non-interest income. This is backed up by it cashflowm which have been generating positive cashflow over the past five. It has been on an upward trend since 2008 from RM5.6 billion to RM11.7 billion in 2017. This shows that Maybank is able to generate sufficient cashflow to fund or maintains its operation over the past ten years.

Overall, based on the past 5 years data, Maybank PE ratio is on upward trend. This shows that the market is valuing the company more than it used to, as the market believed that Maybank will do good in future.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Discussions

Be the first to like this. Showing 11 of 11 comments

Not true loh...!! Price to book value loh...!!

Like pbb the best the most valuable bank or overvalue bank based on price to book value loh....!!

But why people pay so high leh ??

Bcos of quality of assets, growth, dividend, roe and conservative dynamic management loh.....!!

2019-02-09 15:55

Hmmmm.... Anyone who simply just uses p/e as a valuation measure of banks is either a new investor, or someone who didn't know how to value banks. You have to look at it's book value, and the quality of it's book. As most banks are very closely related to a high degree, you have to be more discerning in the metrics you use to measure.

2019-02-09 16:02

I give you chance to explain why I bought public bank since 2012. I give you hint, deposits and loan assets quality. You know how to measure those?

2019-02-09 16:19

thats why it is a good opportunity for u to tell all on pbb success mah..!!

Posted by (S = Qr) Philip > Feb 9, 2019 04:19 PM | Report Abuse

I give you chance to explain why I bought public bank since 2012. I give you hint, deposits and loan assets quality. You know how to measure those?

2019-02-09 16:27

One measures the float, the " free money" a bank has that allows them to give loans on free money.

The other measures the risk of their loans, how high the risk of being caught naked when the tide come out.

Book value is important, but measuring based on a single metric of price versus book value is just as bad as measuring based on earnings alone.

If you knew that you would probably have bought more Hong leong raider.

2019-02-09 16:28

But I'm sure you also bought your Hong leong based on pe ratio also back in 1998, or am I talkcock also?

2019-02-09 16:31

The starting point to look at the Bank's quality is their credit rating.

Strong credit rating will helps in favourable loan pricing, attracts more sticky deposits (e.g. during crisis times, u will notice a flight to safety, deposits flowing to Singapore banks for example), assess to cheap source of funding/ample liquidity. It's about credit spread, managing liquidity and capital position.

Relevant financial ratios to look at are ROE, NIM, LCR, NSFR, LDR,capital ratios.

Banks will only go bust due to 2 things - liquidity crunch or lack of capital.Banks are required to meet certain thresholds (1. LCR for 30 days liquidity position. if u cant survive the first 30 days u will go bust. 2. minimum capital ratios. on top of that regulators also require to build up capital buffer during normal times to survive in the event of economic crisis).

In terms of risk management, you can read their Basel Pillar 3 Disclosures in the Annual Report. 3 main Pillar 1 risks - credit, market and operational risks. There are other Pillar 2 risks that regulator look at to such as interest rate risk in banking book.

Are there any excessive risk taking? look at return on risk weighted assets (instead of ROE).

2019-02-09 18:02

how about credit quality? look at NPL ratios.

how to know if the Bank is being conservative? look at its loan loss coverage.

anyway, if u intend to invest in a Bank, pls note that those old days of high ROE is gone.

with Basel reform (stringent rules on liquidity, structural funding profile, maintaning adequate capital buffer) and new accounting standards (new loan provisioning methodology), it is inevitable that Bank's ROE and NIM to trend lower.

2019-02-09 18:12

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-07 16:20:00

OBV

5 Mins

SELL

2025-01-07 16:15:00

EMA 5

5 Mins

BUY

2025-01-07 16:10:00

EMA 5

5 Mins

SELL

2025-01-07 15:40:00

EMA 5

10 Mins

BUY

2025-01-07 15:35:00

EMA 5

5 Mins

BUY

Apps

Top Articles

1

2

AmInvest Research Reports

3

CEO Morning Brief

Oriental Kopi to Raise Menu Prices Amid Rising Raw Material Costs

4

Kenanga Research & Investment

5

Kenanga Research & Investment

6

PublicInvest Research

7

8

南洋行家论股

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Fabien Extraordinaire

What;s the point of this article?

1) Do u know that Banks are not valued based on PE but rather P/BV? The main determinants to prescribe the P/BV multiple is the Bank's ROE.

2) You can;t look at operating CF basis to determine the Bank's healthy liquidity position. For liquidity, u should assess its LCR. Alternatively, u still can look at the traditional LDR ratio.

2019-02-09 10:31