M+ Online Research Articles

Suria Capital Holdings Bhd - Rewarding Shareholders

MalaccaSecurities

Publish date: Wed, 05 Dec 2018, 10:31 PM

MalaccaSecurities

0 3,683

An official blog in I3investor to publish research reports provided by Malacca Securities research team.

All materials published here are prepared by Malacca Securities. For latest offers on Malacca Securities trading products and news, please refer to: https://www.mplusonline.com.my

Malacca Securities Sdn Bhd

Hotline: 1300 22 1233 / 06-336 5178 (office hours: 8.30am - 5.30pm)

Tel : +606 - 337 1533 (General)

Fax : +606 - 337 1577

Email: support@mplusonline.com.my

All materials published here are prepared by Malacca Securities. For latest offers on Malacca Securities trading products and news, please refer to: https://www.mplusonline.com.my

Malacca Securities Sdn Bhd

Hotline: 1300 22 1233 / 06-336 5178 (office hours: 8.30am - 5.30pm)

Tel : +606 - 337 1533 (General)

Fax : +606 - 337 1577

Email: support@mplusonline.com.my

Highlights

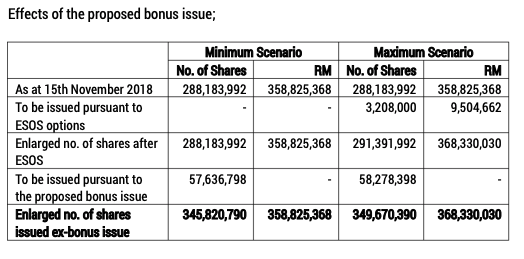

- Suria Capital Holdings Bhd’s (Suria) has proposed a bonus issue of up to 58.3 mln new shares on the basis of one bonus share-for-every five existing shares held on the entitlement date to be determined later.

- As at 15th November 2018, Suria's share capital stood at RM288.2 mln comprising 288.2 mln shares and 3.2 mln outstanding options granted under the employees’ share scheme (ESOS). Assuming all the outstanding ESOS options are exercised prior to the implementation of the proposed bonus issue, 58.3 mln bonus shares will be issued.

- This will result in an enlarged issued share capital of up to RM368.3 mln comprising 349.7 mln shares. (see below). The proposed bonus issue is expected to be completed by 31st January 2019.

Valuation And Recommendation

We are positive on the proposed bonus issue announcement. The aforementioned corporate exercise serves as a reward for Suria’s existing shareholders and it will also improve the trading liquidity of Suria’s shares. Current 3-months average daily traded volume stood at 27,448 shares, representing an average of only 0.01% of the total no. of shares in issue.

There are no changes made to our earnings forecast. Therefore, we maintain our BUY recommendation on Suria with an unchanged target price of RM2.20 (ex-bonus adjusted price of RM1.83). We continue to like Suria for its position as the leading port operator in Sabah, having secured long-term concession agreements with Sabah State Government until 2034 (with an option to renew for another 30 years) and a relatively large-scale expansion plan in the pipeline.

We value Suria through a sum-of-parts (SOP) approach as we valued both its port operations and property development segments on a discounted cash flow approach (key assumptions include a WACC of 8.5%, terminal growth rate of 1.5%) to reflect its ability to generate recurring revenues and steady earnings growth over the longer term.

Source: Mplus Research - 5 Dec 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on M+ Online Research Articles

UOA Real Estate Investment Trust - Earnings Came In Within Expectations

Created by MalaccaSecurities | Nov 15, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-11-18 11:30:00

EMA 5

30 Mins

SELL

2024-11-18 09:00:00

EMA 5

30 Mins

BUY

Apps

Top Articles

3

4

save malaysia!

5

6

Good Articles to Share

BlackRock's Rieder: The technicals are 'crazy good' for stocks

7

Good Articles to Share

Germany's Scholz defends call to Putin ahead of snap elections

8

Good Articles to Share

Nigeria and India agree deeper ties in maritime security, counter-terrorism

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....