M+ Online Research Articles

Market Chat - 4Q22 Outlook & Strategy

MalaccaSecurities

Publish date: Mon, 03 Oct 2022, 08:48 AM

MalaccaSecurities

0 3,682

An official blog in I3investor to publish research reports provided by Malacca Securities research team.

All materials published here are prepared by Malacca Securities. For latest offers on Malacca Securities trading products and news, please refer to: https://www.mplusonline.com.my

Malacca Securities Sdn Bhd

Hotline: 1300 22 1233 / 06-336 5178 (office hours: 8.30am - 5.30pm)

Tel : +606 - 337 1533 (General)

Fax : +606 - 337 1577

Email: support@mplusonline.com.my

All materials published here are prepared by Malacca Securities. For latest offers on Malacca Securities trading products and news, please refer to: https://www.mplusonline.com.my

Malacca Securities Sdn Bhd

Hotline: 1300 22 1233 / 06-336 5178 (office hours: 8.30am - 5.30pm)

Tel : +606 - 337 1533 (General)

Fax : +606 - 337 1577

Email: support@mplusonline.com.my

Navigating the weak ringgit and high interest rate landscape

- Downside risks still prevail on the global markets given the (i) hawkish tone by the US Fed, (ii) ongoing tension between Ukraine-Russia and (iii) recession fear.

- However, there are some bright spots in the Malaysia’s market with the upcoming (i) Budget 2023, (ii) around-the-corner GE15 and (iii) rebounding Malaysia GDP.

- Thus, we like potential budget beneficiary sectors like solar, construction and telco. Meanwhile, for the export-oriented segments we favour plastic, selected technology, medical and chemical.

- For domestic related sector, we may focus on automotive and furniture.

Covid-19 entering the endemic phase

- Treating Covid-19 as a normal flu. Covid-19 indicators are stabilising and our MoH’s directive has been clear that the relaxation of SOPs is likely to continue (i.e. removing mask mandates and social distancing measures).

- Travellers are back. Since we reopened our travel borders in Apr-2022, tourists have been growing consistently over the past few months. We expect another surge in tourist if China citizens are able to leave their country. Generally, China tourists will record around 200k per month.

- Business activities heading for solid recovery. Based on the recent GDP numbers, Malaysia economy expanded 8.9% YoY in 2Q22, supported by normalising economic activity as the country moved towards endemicity and reopening of the international borders. Also, in the recent 2Q reporting season, we noticed some companies were able to register positive growth, albeit undergoing rising inflationary pressure.

Economic review and outlook

- Aggressive interest rate hike... The US Federal Reserve is maintaining an aggressive stance to combat the elevated inflation towards the target of 2% (August CPI stood at 8.1%). Currently, the Fed fund rate is at 3.00-3.25% after hiking 75 basis points last month. Still, the Fed is expected to continue with its hawkish tone and the consensus is looking at 4-4.25% at end-2022.

- …and unwinding of balance sheet. The US central bank has been tapering USD47.5bn (USD30bn in Treasuries and USD17.5bn in MBS) per month starting in June and has stepped up the unwinding to USD95bn (USD60bn in Treasuries and USD35bn in MBS) from September onwards.

- USD index rallied to 20-year high. Perceived aggressive interest rate hike going forward has contributed to the strong rally in the Dollar Index towards a 20-year high. In turn, it has caused an extensive selling across the commodity markets as demand for raw materials decline.

- Bloomberg commodity index (BCI) has peaked around 140, after the start of the Ukraine-Russia war and has been trending lower towards 111 since end-2Q22 as the market is adjusting accordingly to the Fed’s hawkish tone. We believe the BCI may extend its downtrend move to around 100 amid declining demand for commodity.

- Hawkish tone from the Fed is causing a hard landing? The market is pricing in a possible scenario where the US economy may head for a hard landing. Hence, Wall Street have been trending lower, trading ahead of the possible event.

- Bank of England surprised move in the bond market by buying long-dated government bonds to prevent “material risk” to UK financial stability. This may steer the market to think that the US Feds may shift their stance, but we opine that the Fed is committed to bring down inflation at all costs.

- Recovering Malaysia economy. On our local front, we opine that the reopening of borders and full resumption in business activities should continue to chart stronger growth for the rest of 2022. Despite rising input costs, selected companies are able to weather the tough environment at this juncture with the government subsidies (fuel and electricity). We believe Malaysia still has the edge in providing products and services in the global arena with the weak ringgit situation. Based on the consensus, Malaysia’s GDP could grow by a rate of 6.9% and 4.4% in 2022-2023. Also, IMF has upgraded our Malaysia’s GDP to 6.4% for 2022.

Market review

- MSCI World Index and S&P500 are at discount, trading at the PE multiples of 17.9x and 15.8x vs. their respective 10Y avg PE of 20.3x. Meanwhile, the FBM KLCI is trading at 15.5x PE vs. the 10Y avg PE of 17.7x. We believe the market could be pricing a slowdown in economic activities at this juncture.

- Trading activities remained soft as compared to the last year with the YTD ADTV standing at RM2.10bn vs. RM3.54bn in 2021. However, foreign funds are net buyer valued at RM6.7bn on a YTD basis.

- Mostly negative 3Q22 performances. In 3Q22, the FBMKLCI, FBM Small Cap and FBM ACE were down 3.4%, 3.6% and 2%, respectively. All the 13 sectors were in the negative territories, with the top 3 losing sectors include the healthcare (-11.9%), industrial products (-6.5%) and plantation (-6.2%).

4Q22 Outlook & Strategy

- Recovery theme is on the cards. Following the full reopening of business activities and travel borders, economic activities have been recovering as shown in the recent Malaysia’s GDP data. Also, we noticed most of the consumer related companies are having decent growth. We should be able to capitalise on this trend at least for the rest of 2022. We favour the tourism and consumer segments.

- Budget 2023 beneficiaries. In view of the upcoming Budget 2023, we advise traders to position on some related sectors ahead of the event. Given the MoF has provided statements on focusing on ESG, automation and digital technology. Under this segment, we like the solar and EV sectors for the ESG initiatives and technology companies that cater for the automation and digital technology. Also, we believe the budget allocation for the healthcare segment will continue to grow; hence the medical services segment will be on our radar. Besides, in the previous budgets, the construction sector should be one of the beneficiaries under the Malaysia budget.

- Weak ringgit position… As the Federal Reserve is superbly hawkish on their monetary policies, it has driven the Dollar index into the strongest position since 2002. In turn, this has contributed to the decline of ringgit by 10.34% YTD. It could contribute to higher overall input costs for certain companies that only provide products and services in the domestic scene, while benefits export oriented companies. With that, traders may look at the export-oriented segment, such as plastic packaging and selected technology stocks in 4Q2022.

- …and high interest rate environment. Moving forward, high interest rate may stay as a norm. With the interest rate environment, we think believe investors should opt for either stocks with high net cash, low gearing, or stable dividend track record to weather through this tough situation.

- High backlog orders in the automotive segment. Due to chip shortages after the Covid-19 outbreak and Ukraine-Russia war, it was indicated by the finance minister that the backlog orders stood at 264k vehicles on 20th of June, excluding those that rushed to book their vehicles prior to the expiration of the SST exemption on 30th of June. We believe the delivery of the new cars is within a waiting period of 6-12 months, which will contribute automakers’ earnings in the next few quarters. Also, MAA reported that vehicle sales in Malaysia jumped to 66,614 units in Aug-22 (+36% MoM, +272% YoY). Thus, we like automakers, automotive-related companies such as leather upholstery or car accessories.

ATECH – One-stop solution EMS provider

- One-stop solution of Electronic Manufacturing Services (EMS) provider that is moving up the value chain by incorporating Industry 4.0, which involves the automation of its production lines and automated material handling to increase productivity as well as improve production efficiency.

- New manufacturing plant expansion in the pipeline with total built up of 70,999-sqf will boost annual capacity of placement points to 5.87bn per annum by end-2023.

- Introduction of new product by partnering with third party for the development of lithium-ion battery pack system to tap into the green energy sector.

CCK – Resilient demand for food products

- CCK principally involved in poultry, prawn agriculture and prawn processing as well as retailing business that carried out primarily in Sarawak, Sabah and Indonesia.

- Acquisition of PT Bonanza in Apr-2022, a prawn processing business in Indonesia that derives most of the sales from exports to Japan (80%) and should bring business synergies and contribute to the group’s earnings from 3Q22 onwards.

- Operation in full capacity under endemicity. We should expect strong sales volume in its retail and wholesale channels underpinned by the overall recovery in consumer demand with the reopening of F&B outlets.

GAMUDA – One of the leading construction and property players

- Gamuda Bhd engages in engineering and construction, property development and water and expressway concessions. Completed infra projects include SMART, Ipoh Padang Besar, EDT, KVMRT1, LDP, SAE, SPRINT, SSP3 and Sg S'gor Dam.

- Outstanding orderbook stood at RM14bn as of end-Jul 2022, providing earnings visibility for another 3-4 years.

- Highway sale is nearing completion. KESAS, LDP, SPRINT and SMART are acquired by ALR and the deal is expected to be completed in mid-Oct 2022. With that, GAMUDA planned a special dividend of 39 sen and the RM1bn one off gain from the highway sale will be able to help lowering its net gearing.

HEXTAR – Expanding the agriculture and O&G segments

- Engaged in the manufacturing and distribution of agrochemicals, specialty chemicals and consumer products with 600 products registered domestically and globally. HEXTAR has expanded its operations to 30 countries.

- Diversification into the specialty chemicals business in FY21 is bearing fruit as the segment contributed around one-third of its revenue in 1H22, eyeing higher demand amid increasing industrial production and activities.

- To consolidate its foothold in the Australian and New Zealand oil & gas market, leveraging on Hextar Kimia Sdn Bhd’s core competencies in the O&G industry.

KGB – Sustainable orderbook in the tech sector

- Ultra-High Purity specialist in prime position to leverage onto the semiconductor supply chain as chip shortages may last beyond 2023.

- Outstanding orderbook of c.RM1.87bn, which represents a cover ratio of 3.6x against FY21 revenue, providing earnings visibility over the next 2 years.

- Industrial gas segment shifting into higher gear as liquefied CO₂ plant utilisation hits 80% in 1H22 and 10-year supply for an optoelectronics semiconductor giant in Kulim, Kedah will commence in 1Q23.

MYEG – Flagship e-government solution and servicers provider

- MYEG provides a complete range of major government services in the areas of immigration, automotive and others. Services include (i) check and pay road tax, (ii) renew driving license, (iii) renew maid & foreign worker permit permits and etc.

- Reopening of business activities and international borders. Business outlook turning positive with the full operation of MYEG’s E-services Centers, while the foreign worker segment should gain momentum as government has allowed the applications for foreign workers into various industries since Feb 2022 onwards.

- Budget 2023. Should the government re-instate the GST going forward, MYEG may benefit for its GST monitoring system given their role as the system provider earlier.

OPTIMAX – Leading eye specialist in Malaysia

- One of the leading eye specialist providers which operates an extensive network of 12 ACCs and 1 specialist hospital.

- Expanding to JB and Negeri Sembilan. Eyeing its first satellite clinic in Skudai, Johor, and a new ACC in Bahau, Negeri Sembilan, to be operational by end-2022.

- Projects in the pipeline that offer earnings visibility include (i) collaboration with Selgate for Optimax to operate full-eye services and (ii) collaboration with Sena and KESH whereby Sena will construct a private eye hospital in Kempas and rent it to Optimax, enabling the group to capture the rising demand for eye specialist services from Singapore upon completion of the RTS Link.

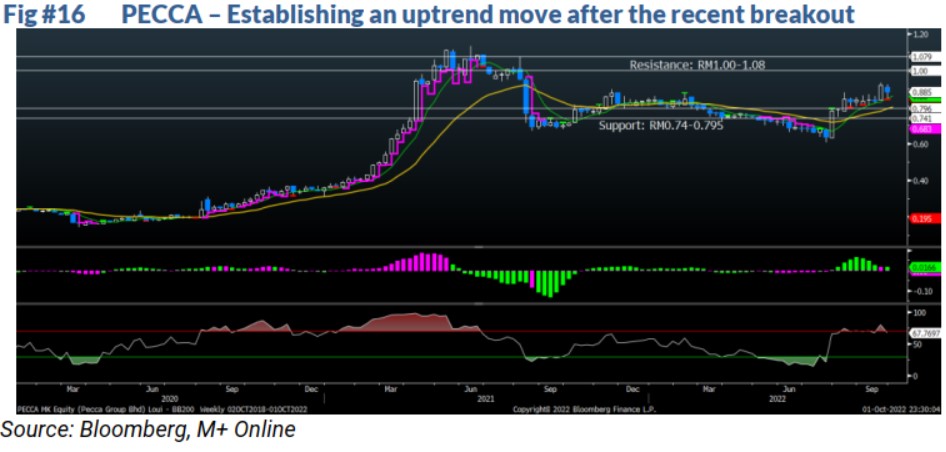

PECCA – Leader in automotive leather upholstery space

- Leading manufacturer of automotive leather seats for national marques such as Proton & Perodua and the group exports to prominent international auto makers such as Toyota, Honda, Mitsubishi, Volkswagen & Subaru.

- Acquisition of 4.3-ac land at Serendah, Selangor to house a new manufacturing plant, boosting production capacity to 40,000-50,000 seats per month by end-2023 (from 20,000-30,000 at present).

- Leveraging onto the strong automotive sales whereby the Malaysian Automotive Association (MAA) has forecasted total industry volume (TIV) to hit 630,000 units in 2022, mainly driven by the robust sales in 1H22.

SAMAIDEN – Rising adoption in the RE segment

- Renewable energy solution provider that involved in EPCC of solar PV systems and power plant, provision of renewable energy and environmental consulting services, as well as operation and maintenance services.

- Outstanding orderbook stood at RM358.0m as of 2Q22 is expected to contribute to the group’s profit over the next three years. Meanwhile, government’s initiatives via LSS projects coupled with increasing number of companies in private sector to install the solar PV systems will drive growth going forward.

- Ongoing regional expansions including incorporation of a new company in Vietnam, partnership with Aneka Jaringan Holdings Bhd to establish a joint venture company in Indonesia, and business collaboration agreement with Chudenko Corporation for overseas expansion leveraging on Chudenko’s network

SCOMNET – Flourishing in the medical segment

- New products in the pipeline under the medical segment with secured customer base that will come on stream in 4QFY22 and that would be the key revenue contributor for FY23f.

- Products pricing revision performed in August 2022 to keep margins intact to combat the inflationary pressure from the rising raw material costs.

- Demand for medical products and devices are likely to stay robust. Budget 2023 could expect greater allocation to the healthcare services sector following the higher number of incidences of non-communicable diseases.

SIGN – Outstanding orderbook to sustain earnings

- Leading kitchen cabinet and wardrobe manufacturer with a substantial presence across 15 countries in both retail and project segments.

- Outstanding orderbook remained promising at RM192.0m for Kitchen and Wardrobe System, RM255.0m for Aluminium and Glass segment, and RM165.0m for Interiors fit-out works as at end June 2022.

- Proposed acquisition of 23.7% equity interest in Fiamma Holdings Bhd (FIAMMA) offers a strategic opportunity for the group to gain foothold in the electrical home appliances and to leverage on FIAMMA’s network to cross-sell its products.

TGUAN – Bode well under easing resin price environment

- One of the largest plastic packaging manufacturers with existing manufacturing operations in Malaysia, China, and Thailand and with global presence in over 70 countries; revenue principally contributed by plastics packaging division (92.0- 95.0%) and manufacturing and trading of beverage (5.0-8.0%).

- Capacity expansion plan in 2022 includes the installation of six new production lines which will boost its annual production capacity by 50k tonnes.

- Resin price which is expected to hold steady following a downward trajectory since 2Q22 should bode well for the group’s margin, barring any unforeseen circumstances on the resin supply.

TIMECOM – Beneficiary of the 5G rollout

- Time Dotcom Bhd offers fixed-line and enterprise services, including data (broadband and wireless), voice, and data center services. Retail and enterprise deal with households and companies, respectively, while the wholesale segment provides backhaul services to Asia-Pacific and Malaysian telco companies.

- TIMECOM’s retail segment has been expanding supported by its growing base of customers upgrading to higher-speed plan. This quarter, it has rewarded shareholders with a dividend of 16.34 sen per share.

- 5G rollout to benefit TIMECOM as the wholesale segment provides backhaul services to Asia-Pacific and Malaysian telecommunication companies to transfer data and it is a mandatory pre-requisite in broadband/5G infrastructure build-up.

Source: Mplus Research - 3 Oct 2022

More articles on M+ Online Research Articles

UOA Real Estate Investment Trust - Earnings Came In Within Expectations

Created by MalaccaSecurities | Nov 15, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

BFM Podcast

2

3

4

5

Mercury Securities Research

6

BFM Podcast

7

BFM Podcast

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....