equitydiary.blogspot.com

Success Transformer - Profits shine through

equitydiary

Publish date: Fri, 28 Aug 2015, 07:43 AM

Link to official blog: www.equitydiary.blogspot.com

SUCCESS TRANSFORMER CORP BHD

Profits shine through

By the looks of things, profits of Success Transformer Corp (STC) being clouded by its subsidiary has come to an end.

With promising 2Q15 results released yesterday, this low P/E stock of decent quality looks like it’s on its way for a rerating.

Based on yesterday’s closing price of RM1.38 and an annualized 2Q15 EPS of 40.64 sen, the stock is trading at a prospective P/E of just 3.4x. If we apply a P/E of 6x to that annualized EPS, it would give the stock a value of RM2.44, or an upside of 77% to its last traded price.

To recap, STC’s 65% owned subsidiary, Seremban Engineering Bhd (SEB) posted heavy losses in 4Q14 and 1Q15 due to cost overruns of the Sabah Ammonia Urea project (which is more than 90% complete now). This clouded STC’s transformer and lighting profits as they were consolidated with SEB’s (see Figures 1, 2 and 3, highlighted in red).

Based on SEB’s 2Q15 report, it appears like the cost overruns had mostly been provided for in 1Q15 and will no longer be seen in SEB’s future financials.

Figure 1: SEB quarterly P&L

Source: Company quarterly reports

Figure 2: STC quarterly P&L

Source: Company quarterly reports

Figure 3: STC quaterly segmental profit

Source: Company quarterly reports.

Note: Segmental profits here are approximations as the company does not provide profit breakdown by segment in quarterly reports.

a Derived by subtracting b from c

b Operating profit/loss taken from SEB’s income statement.

c Operating profit/loss taken from STC’s income statement.

The latest 2Q15 results show SEB’s profit levels to be back in the normal range (albeit at the lower range due to a drop in sales), and as a result, STC’s transformer and lighting segment's profits are now shining through again.

The transformer and lighting segment showed decent margin expansion vs. in most recent quarters; revenue grew about 3% yoy while operating profit climbed 13%.

For the process equipment segment, sales dipped 32% yoy, but this didn’t affect STC’s overall profits much. Even if we stripped out or assume zero profits for this segment, STC’s net profit would have still been around RM10.5m or 9 sen EPS in 2Q15.

I have read some articles on STC’s business outlook especially on its LED lighting and I’m quite convinced. Could 2Q15 be a precursor to STC’s continuation in growth?

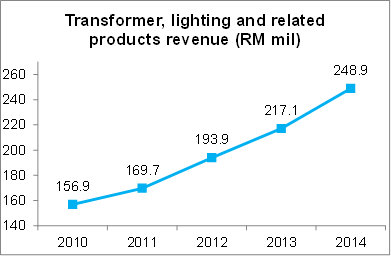

Figure 4: STC’s segmental results, 2010-2014

Source: Company annual reports.

Figure 5: STC’s transformer, lighting and related products segment revenue, 2010-2014

Figure 6: STC’s process equipment segment revenue, 2010-2014

I'm not too concerned about Success' capex levels as the company is in expansion/growth mode. I believe Success is taking the opportunity to expand fast while they can. If they're spending to expand an unprofitable business then that would obviously be bad, but this isn't the case for Success.

Once they've taken expansion to a good enough level, they would cut down on capex, and now with the higher profits from the expansion, the effect would be: strong cash flows, which would lead to debts going down and cash going up.

A good company from a long-term investor's point of view.

*********

“Currently we are actively exporting our lighting range to more than 40 countries, tapping the global market.”

– STC Annual Report 2014

Link to official blog: www.equitydiary.blogspot.com

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on equitydiary.blogspot.com

Discussions

2 people like this. Showing 3 of 3 comments

Thank you, I appreciate your feedback.

What stocks are you currently eyeing or think have good potential upside?

2015-09-29 11:41

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-11-26 15:30:00

ADX

5 Mins

SELL

2024-11-26 15:25:00

ADX

5 Mins

BUY

2024-11-26 14:30:00

OBV

30 Mins

SELL

Apps

Top Articles

2

save malaysia!

3

4

5

6

Koon Yew Yin's Blog

7

THE INVESTMENT APPROACH OF CALVIN TAN

8

Good Articles to Share

Le Pen makes new threat to withdraw support for French government

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

chonghai

Everything looks good until I saw that CAPEX is more than Depreciation. I will pass this.

2015-08-28 09:55