JP Morgan Stupid or what?

Glove is Bitcoin #Glovestronk!!

super_newbie

Publish date: Sun, 31 Jan 2021, 04:01 PM

Happy weekend everyone. I would like to share with you a report on disposable glove industry overview.

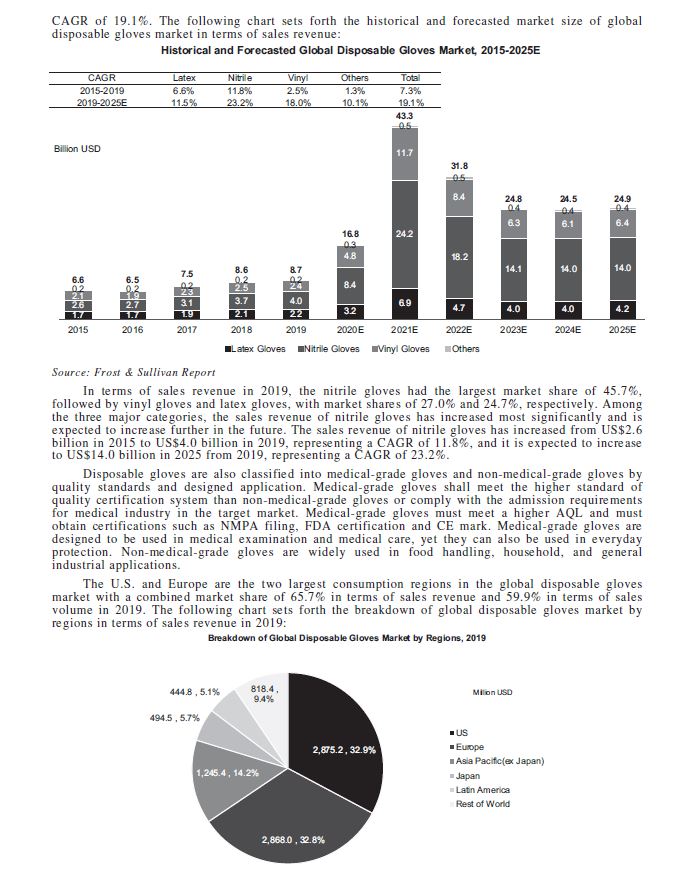

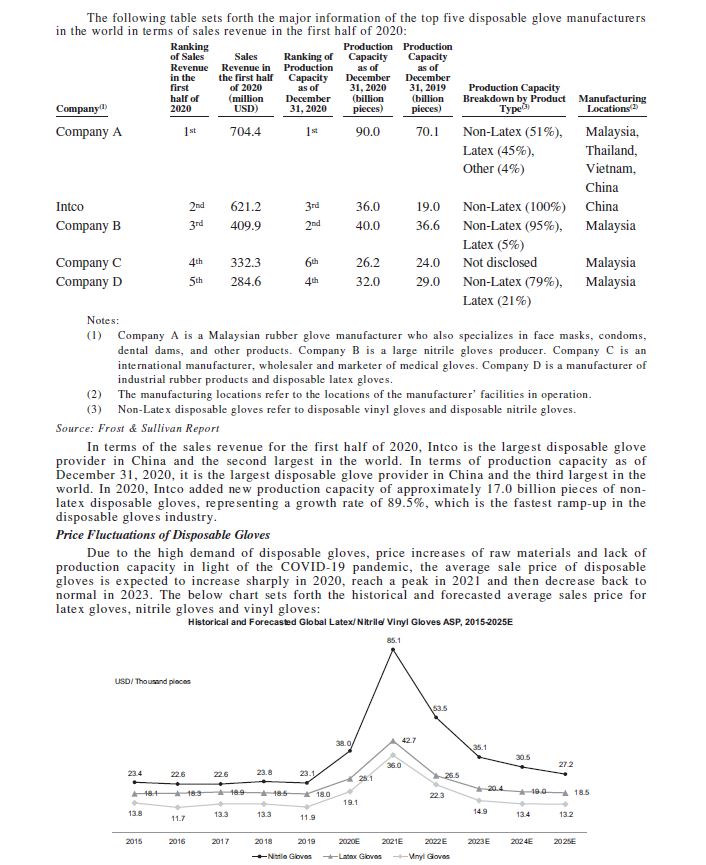

All in all, in terms of sales revenue, the global disposable glove market increased steadily from US$6.6billion in 2015 to US$8.7 billion in 2019, representing a CAGR of 7.3%. The global disposable gloves market is expected to grow from US$8.7 billion in 2019 to US$24.9 billion in 2025, representing a CAGR of 19.1%. JP Morgan stupid or what? Called sell on such a high growth sector among those in Bursa.

Nevertheless, Frost & Sullivan might overblow as well, so make your own judgement. Anyhow, happy reading everyone.

#GloveisBitcoin #Glovestronk!! #TopGlove #Hartalega #Supermax #Kossan

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2025-01-31

SUPERMX2025-01-27

KOSSAN2025-01-24

KOSSAN2025-01-24

TOPGLOV2025-01-23

CAREPLS2025-01-23

CAREPLS2025-01-23

CAREPLS2025-01-23

HARTA2025-01-23

HARTA2025-01-23

TOPGLOV2025-01-23

TOPGLOV2025-01-23

TOPGLOV2025-01-23

TOPGLOV2025-01-23

TOPGLOV2025-01-23

TOPGLOV2025-01-22

TOPGLOV2025-01-22

TOPGLOV2025-01-22

TOPGLOV2025-01-21

HARTA2025-01-21

KOSSAN2025-01-21

KOSSAN2025-01-21

TOPGLOV2025-01-21

TOPGLOV2025-01-20

HARTA2025-01-20

KOSSAN2025-01-20

KOSSANMore articles on JP Morgan Stupid or what?

Discussions

12 people like this. Showing 29 of 29 comments

Walao! Please send pampers to shorties! Somemore 2molo Msia market not open!!

2021-01-31 19:02

YES! Glove is BITCOIN in this time compared to past commodity or product called TULIP, chased by mad herd until the abattoir. All slaughtered good and proper.

2021-01-31 19:59

2021-01-31 20:11

If anyone want to follow JPMs trip to Holland strategy, sell at rm5+ tgen wait till neck long until the clouds for Rm3. 50.....lol.... Be my guest....

2021-01-31 23:25

JPM's TP (Rm3.50) is unlikely to happen in this year lah

Last time another joker IB UBS's TP Rm5.00 on 18 Sep 2020 (when TG was ard RM7.80 then) also never materialize.....

But Macquarie's controversial TP Rm5.40 on 10 Sep 2020 did happen....lowest Topglove price touched was RM5.23 on 04 Jan.

2021-02-01 06:43

Nevertheless, the current price of Topglove RM6.74 is certainly very much closer to UBS n Macquarie's TP rather than our local inv banks' TP (especially Affin Hwang'a TP RM100 before bonus or RM33.33 after bonus).....lol

Who's TP is more chun u see yrself lah

2021-02-01 06:48

Topglove share price went up 4x from 2015 till end of 2019 when the world overall grow 7.3% CAGR. Harta share price grow 3x ,kossan grow 2x and supermx no growth during this same period. With Frost and Sullivan forecast of 19.4 CAGR from 2020 till 2025,how much will Topglove share price grow? 4x, 6 x ,8 x or 10x ? If it is 4x, the TP is RM 8 ,If 6x , TP will be RM 12 and if 8x , TP will be RM 16 , 10x will be RM 20 by 2025. The growth rate of 19.4 % is 2.5x of 7.3 % CAGR.

2021-02-01 12:08

JP Morgan stated vaccination do not require gloves but most news report with photo shows healthcare professionals wearing gloves. Guess JPM must be embarrass now retaliate with 3.50

2021-02-01 12:30

Whether gloves used in vaccine or not is red herring

Even if entire world vaccinated using gloves - roughly 14bn pieces, that's only 4-5% of total annual glove usage

Much more gloves goes to general healthcare usage, Covid testing and now due to Covid gloves are required for use in a range of industries

Use of gloves for vaccines only adds to demand at the margin

Part of the reason gloves aren't being used for vaccinations in some countries is due to shortages due to no supply - so have to prioritize gloves for testing first

2021-02-01 14:00

JP Morgan is CORRECT.

The IB is referring to ASP normalisation from 2022 onwards

By 2023, ASP would have drop by half based on their forecast.

Do your math and you will appreciate their calculation

However, glove stocks will still enjoy good profit for at least the next 12mnths amid declining ASP GROWTH.

Thus, it depends whether investors willing to hold on for long term(>5yrs) or just ride this short term(<1yr) play till it's peak.

2021-02-01 14:24

Declining ASP growth? Hartalega just guided for another 50% quarter-on-quarter

2021-02-01 14:35

Exactly @calvin69... So retail investors must choose who they MUST listen to, to guide their buys & sells. Bankers or ppl in the biz themselves?

Btw in case we didnt know, responsible bankers get periodic update meetings from the ppl in the biz before they write their reports ya. On the other hand, some irresponsible bankers write their reports after happy hour at Four Seasons rooftop.

2021-02-01 22:49

@calvin69

Yes. It's declining ASP growth. The management guidance is 50% per quarter.

Previously most glove counters are having 30% ASP growth month on month.

Refer to news report from June 2020.

I guess you came on late

2021-02-02 18:18

KUALA LUMPUR (Feb 2): RHB Research Institute and Kenanga Research have trimmed their target prices (TPs) for Supermax Corp Bhd due to a lack of visibility of its average selling prices (ASPs) and execution risk of its US venture.

Kenanga Research analyst Raymond Choo Ping Khoon, who kept his "outperform" call, said the research house had cut its TP to RM9.05 from RM7.80 previously based on 12 times calendar year 2022 estimated (CY22E) earnings per share (EPS) as the research house rolled over its valuation base from CY21 to CY22.

This was due to execution risk of the company's US venture to manufacture medical gloves and other personal protective equipment (PPE) with an initial capital outlay of RM405 million, as well as the lack of ASP visibility, he noted.

Supermax previously noted that while ASPs had not peaked in the first quarter of 2021 (1Q21) yet, demand is expected to moderate with the roll-out of Covid-19 vaccines.

As at the time of writing today, shares of Supermax had risen seven sen or 1.03% to RM6.87, valuing the group at RM18.69 billion. It had seen some 15.97 million shares traded.

Meanwhile, RHB Research Institute, which maintained its "buy" call on Supermax, lowered its TP to RM10.60 (from RM13.25), with a 56% upside and an about 7% yield.

“Our TP reflects 8.3 times FY22F P/E (price-earnings forecast for the financial year ending June 30, 2022; a 20% discount versus peers). This discount is justified due to Supermax’s lower market capitalisation. Our ‘buy’ call is premised on stronger earnings prospects for 3QFY21 (the third quarter ending March 31, 2021), an expected positive news flow from its venture to build a manufacturing plant in the US and its dual listing on the Singapore Exchange (SGX).

“We lower our TP to RM10.60. [Our] long-term ASP [assumptions] have been lowered to US$47 (RM190.04)/box (from US$48) as higher near-term ASPs should result in stronger competition in the long run. Beta has been increased to account for higher share price volatility,” said RHB analyst Alan Lim.

To recap, the glove maker’s net profit for the latest quarter, 2QFY21, climbed 34% quarter-on-quarter (q-o-q) to RM1.06 billion from RM789.52 million for the preceding 1QFY21, while quarterly revenue surged to RM2 billion compared with RM1.35 billion for the preceding quarter.

On a yearly basis, net profit jumped by a whopping 3,142% from RM30.17 million a year ago, while revenue also surged from RM385.5 million for the previous year.

However, despite cutting their TPs for Supermax, both research houses raised their earnings forecasts due to higher ASPs seen for the coming quarters.

Kenanga said it likes Supermax for its original brand manufacturing (OBM) model, which enables it to extract higher margins from distributor pieces compared to original equipment manufacturer (OEM) models at lower factory prices.

“[We] raise [our] FY21E/FY22E net profit by 27%/16% after hiking our ASP [assumptions] from US$65/1,000 pieces and US$45/1,000 pieces to US$70/1,000 pieces and US$50/1,000 pieces respectively,” said Choo.

RHB also increased its forecast for FY21 by 36% due to a higher ASP assumption.

“However, we maintain our FY22F-23F earnings as we keep [our] ASP assumptions unchanged. Note that our FY21-23F blended ASPs of US$89, US$57 and US$48 already assume an ASP decline in the future once Covid-19 ends,” said Lim.

In the short term, Lim said RHB expects earnings for Supermax to continue to rise for 3QFY21.

“Beyond that, Supermax is a beneficiary of stable glove growth demand of 8%-10% annually. Our ESG (environmental, social and governance) score for Supermax is 2.89,” added Lim.

2021-02-02 20:04

Prime Minister Tan Sri Muhyiddin Yassin announced the National Covid-19 Immunisation Programme set to be rolled out at end-February, the country’s biggest vaccination effort ever.Muhyiddin said that 80% of the country’s population, or about 26.5 million people, were expected to receive the vaccine free of charge.

2021-02-07 12:04

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE INVESTMENT APPROACH OF CALVIN TAN

2

My Trading Adventure 2025

3

All Official Update

4

My Trading Adventure 2025

5

Bursa Stock Talk

6

Readers' Digest MY

Japan’s Telecommunication Boom: Innovation, Growth & the Future

7

My Trading Adventure 2025

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Lam Gerard

good

2021-01-31 16:36