HLBank Research Highlights

Trading idea: HIAPTEK: Anticipate a strong turnaround in FY18; Signs of bottoming up

- Business profile: HIAPTEK is primarily involved in pipe manufacturing and the trading of general steel products, supplying to multiple of industries including manufacturing, infrastructure, water, power plant, shipbuilding, oil & gas, as well as the construction market. Through Eastern Steel S/B, a 55%-owned joint-cont rolled entity (JCE) with Orient Steel Investment Co Ltd (40%) and Chinaco Investment Pte Ltd (5%), Hiaptek is also operating an integrated iron and steel mill at Kemaman, Terengganu.

- However, in view of the depressed industry outlook, soft demand and the increased volatility of foreign exchange rates, the jointly controlled entity (JCE) was temporarily suspended its trial production in Oct 2015 as part of the strategy to minimize losses. ESSB also holds an iron ore mining concessions in Bukit Besi, Terengganu.

- Nevertheless, given the more favourable industry outlook in the medium to long term, HIAPTEK will commence planning for the resumption of trial runs in 1HFY18 and earnings is likely to contribute from FY19 onwards.

- A new journey in FY2018 after a huge impairment loss in FY17. HIAPTEK FY17 operating profit surged 60% to RM170.8m, mainly driven by higher ASPs despite a 6% drop in revenue. However, following a hu ge RM215m impairment loss (non-cash item) in JCE, HIAPTEK’s net losses expanded 145% to RM103m. After the kitchen sinking exercise in FY17, we expect a strong turnaround year in FY18.

- Ascribing a conservative 15% growth in revenue to RM1.23bn in anticipation of rising domestic demand brought about by more contract awards for the high impact mega infrastructure and government development projects, we expect HIAPTEK to record a net profit about RM66.3m, riding on resilient EBIT margin of 11.5% amid steady RM/US$ and ASPs (which will cushion margin compression from rising raw material prices), narrower JCE losses and imputing a lower effective tax rate of 22%.

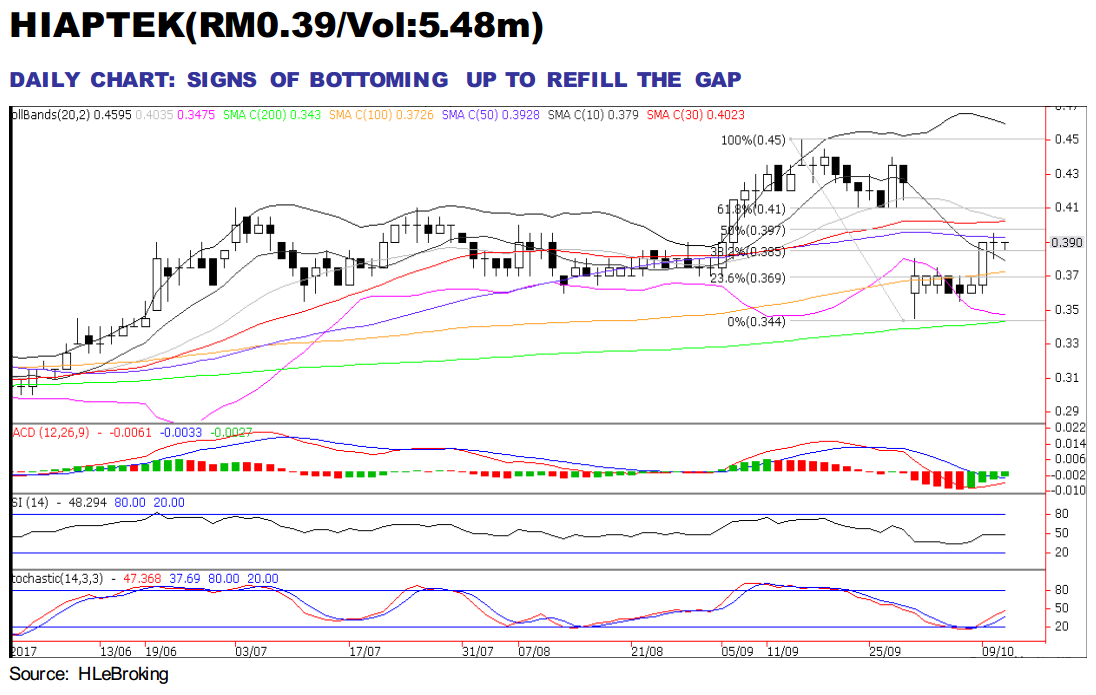

- Signs of bottoming up. At RM0.39, HIAPTEK is trading at undemanding 0.63x P/BV, which is 33% below its peers and supported by bullish outlook in the medium to long term. The stock was smashed down to a low of RM0.345 on 29 Sep after reporting a sluggish 4QFY17 results. Nevertheless, the stock managed to rebound steadily to close at RM0.39 yesterday in anticipation that the company will pose a strong turnaround in FY18. Given the long legged Doji on 29 Sep and the white candle on 9 Oct, more upside is in place to refill the RM0.38-0.425 gap. A successful refill of the gap will spur prices higher towards RM0.45 (52-week high) and our LT goal of RM0.475 (123.6% FP). On the flip side, failure to hold near RM0.365-0.375 levels may weaken share prices lower towards RM0.345. Cut loss at RM0.355.

Source: Hong Leong Investment Bank Research - 12 Oct 2017

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-30 16:50:00

EMA 5

5 Mins

SELL

2024-07-30 16:40:00

EMA 5

5 Mins

BUY

2024-07-30 16:35:00

EMA 5

5 Mins

SELL

2024-07-30 16:30:00

EMA 5

5 Mins

BUY

2024-07-30 16:25:00

EMA 5

5 Mins

SELL

Apps

Top Articles

1

https://dividendguy67.blogspot.com

2

Good Articles to Share

3

4

Good Articles to Share

5

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....