HLBank Research Highlights

Trading idea: PESONA: Riding on the strong orderbook of RM1.7bn; Building a base near RM0.50

- HLIB institutional research has a BUY rating with SOP TP of RM0.76, or 43% upside. Pesona (listed in Oct 2012 via the RTO of Mithril) offers investors exposure to a pure construction play with an incoming stream of recurring earnings from SEP (concessionaire of UNIMAP hostel). Its orderbook stands at a healthy RM1.7bn, translating to a 4.5x cover on FY16 construction revenue, supported by robust earnings growth (FY16- 19 earnings CAGR of 35%).

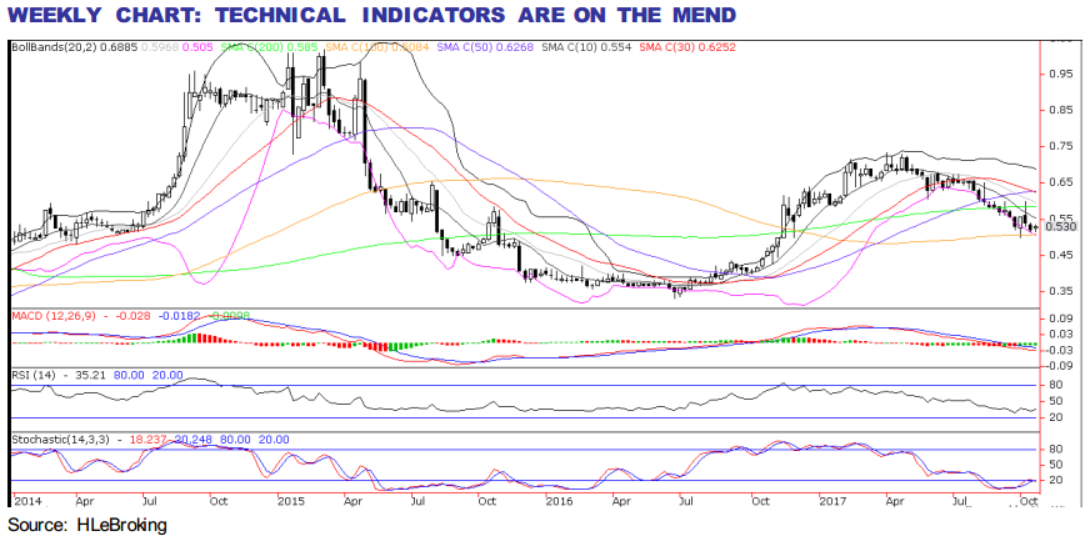

- Building a base near RM0.50-0.51 after sliding from 52-week high of RM0.735. PESONA’s share prices slid 32% from 52-week high of RM0.735 (5 Apr) to a low of RM0.50 (5 Oct) before closing at RM0.53 yesterday. The sluggish performance was attributable to slow jobs replenishment with nil secured YTD after losing out on 3 building jobs that it initially targeted for as the margins were too low for comfort. Nevertheless, the impending issuance of the remaining 12m shares at RM0.70/share (2 nd tranche acquisition of SEP-concessionaire of UNIMAP hostel) should set a new minimum benchmark valuation for the stock.

- Pending a downtrend line breakout. PESONA’s share prices are likely to stage a breakout above RM0.56 (50-d SMA) in the near term after building a base near RM0.50-0.51 territory in the last three weeks. A successful breakout above RM0.56 will spur prices higher towards RM0.59 (downtrend line) and our LT objective at RM0.635 (200-d SMA). Conversely, a breakdown below RM0.50 will trigger further selldown towards RM0.44-0.45 zones. Cut loss at RM0.49.

Source: Hong Leong Investment Bank Research - 27 Oct 2017

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-30 16:50:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-07-30 16:50:00

TURTLE SYSTEM 55

5 Mins

SELL

2024-07-30 16:40:00

EMA 5

5 Mins

BUY

2024-07-30 16:40:00

ADX

5 Mins

BUY

2024-07-30 16:40:00

MACD/RSI

5 Mins

BUY

Apps

Top Articles

1

https://dividendguy67.blogspot.com

2

Good Articles to Share

3

4

Good Articles to Share

5

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....