HLBank Research Highlights

Frontken Corporation - Attractively priced after recent rout

Following a robust 3Q18 results, our analyst remains confident of an encouraging 4Q18 results (albeit external headwinds), mainly driven by strong semiconductor divisions amid encouraging outlook (+15.9% to US$478bn 2018; +2.6% to US$490bn 2019; Source: WSTS Nov 2018) while O&G division continues to exhibit resiliency (IEA expects stable global oil demand growth at 1.4m bpd from 1.3m bpd in 2018). Downside risk is limited (-24% from all-time high at RM0.995), as sentiment is boosted by weak RM and a strong 16% FY18- 20 EPS CAGR coupled with solid balance sheet (net cash 10sen/share). At RM0.755, Frontken is trading at 14.5x FY19 P/E (15% discount to 1Y average of 17.1x). Ex-cash, the stock is trading at 12.5x P/E (27% below 1Y average).

HLIB institutional research has a BUY rating with TP at RM1.05 (+39% upside). Frontken is expected to experience multi-year growth ahead on the back of (i) bullish global semiconductor market outlook with the Asia Pacific region (contribute c.16% to revenue) is projected to expand 16% and 3.1% in 2018 and 2019, respectively, boding well for Frontken who services all major foundries in this region; (ii) robust fab investments by major foundries and migration to the 7nm/+ nodes (in the Dec release, SEMI said global sales of new semiconductor manufacturing equipment are projected to increase 9.7% to all-time high of USD62.1bn in 2018 (2017: USD56.6bn), and easing 4% to US$59.6bn in 2019 before growing 20.7% in 2020 to reach USD71.9bn) (iii) leading edge technology; (iv) resilient O&G; and (v) strong balance sheet.

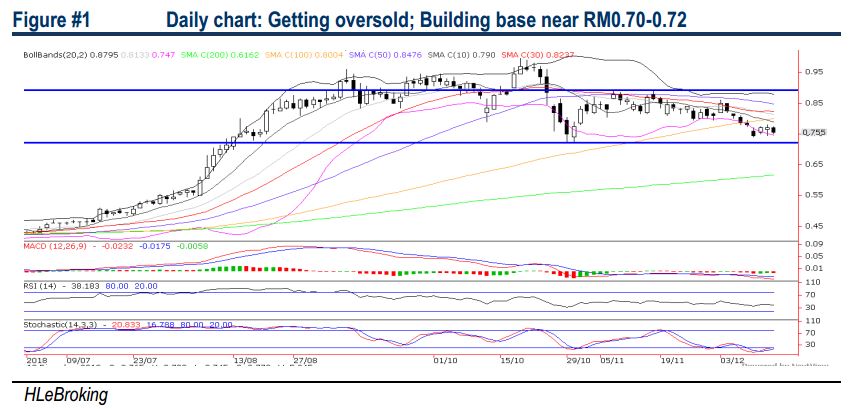

Poised for a relief rebound after building a base near RM0.72. Despite prevailing headwinds, we opine that Frontken’s 24% correction from all-time high of RM0.995 (18 Oct) has grossly discounted the concerns over mid to long term earnings uncertainty. Excluding its net cash with RM108m or 10sen/share, valuation is even more compelling at 12.5x P/E (27% below 1Y average). However, current wobbly sentiment may witness a sideways consolidation before a meaningful rebound later, with key supports at RM0.70-0.72 (30 Oct low). A decisive breakout above RM0.79 (10d SMA) is likely to lift share prices higher towards RM0.825 (30d SMA) before heading towards our LT objective at RM0.89 (18 Nov high). Cut loss at RM0.69

Source: Hong Leong Investment Bank Research - 14 Dec 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –26 September 2024 (High risk)

Created by HLInvest | Sep 26, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

.png)

MQ Trading Signals

Time

Signal

Duration

Type

2024-09-26 16:50:00

TURTLE SYSTEM 20

10 Mins

BUY

2024-09-26 16:50:00

TURTLE SYSTEM 20

5 Mins

BUY

2024-09-26 16:30:00

EMA 5

5 Mins

BUY

2024-09-26 16:20:00

EMA 5

5 Mins

SELL

2024-09-26 16:20:00

TURTLE SYSTEM 20

5 Mins

SELL

Apps

Top Articles

1

2

Rockstone Investment

Binastra Corp Bhd – A Promising Investment in Construction in 2025

3

AmInvest Research Reports

4

save malaysia!

5

8

CEO Morning Brief

China Probes Calvin Klein Parent Over Suspected Xinjiang Boycott

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....