HLBank Research Highlights

Traders Brief - Choppy Sessions Ahead Due to Ongoing Feb Reporting Season and Recession Fears From Covid-19 Epidemic

MARKET REVIEW

Regional stock markets ended mixed as investors continued to assess the potential economic fallout from the COVID-19 that has infected more than 73000 people and killed about 1800. Sentiment was also dragged by news that the Japan’s economy contracted at an annualised pace of 6.3% in the Oct-Dec quarter, shrinking at the fastest pace in almost six years and flagging a recession risk. Bucking the trend, SHCOMP and HSI jumped 2.3% and 0.6%, respectively as Beijing stepped up policy stimulus to cushion the economic impact from the coronavirus outbreak.

Tracking sluggish regional markets amid recession fears and expectations of a soft ongoing Feb reporting season, KLCI slid 7.3 pts to 1537.2. Trading volume increased to 2.91bn shares worth RM1.9bn as compared to Friday’s 2.67bn shares worth RM2.26bn, accompanied by negative market breadth of 413 advancers as compared to 444 decliners.

US financial markets were closed on Monday, in observance of Presidents Day. Despite easing 25 pts to 29398 last Friday, Wall Street posted back-to-back weekly gains with the S&P 500 and Dow rose 1.6% and 1%, respectively whilst the Nasdaq rallied 2.2%. Those advances come even as investors grappled soaring number of reported coronavirus cases.

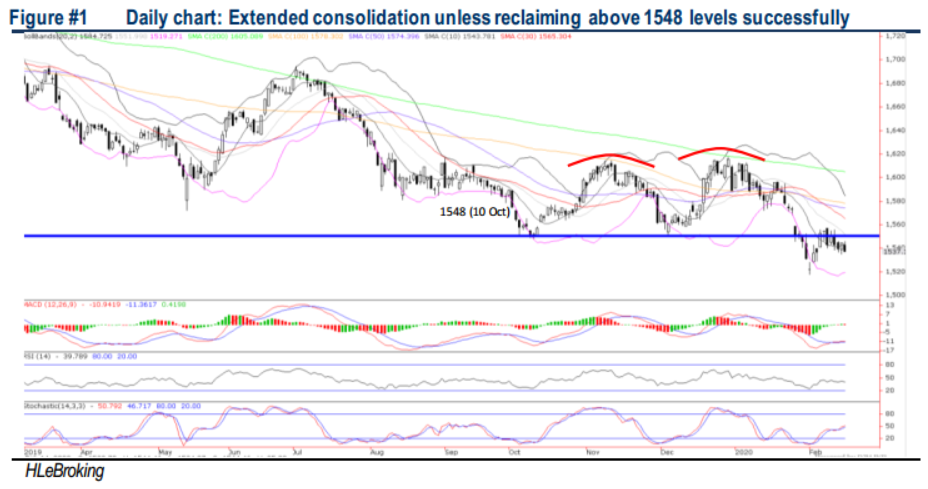

TECHNICAL OUTLOOK: KLCI

Following the double top patterns, KLCI tumbled 6.2% from 1617 (30 Dec) to 1517 (3 Feb), violating the neckline support of 1548. Although rebounding 2.6% or 40 pts to 1557 (10 Feb), the momentum tapered off as the index continued its downtrend to end 7.3 pts lower at 1537.1 yesterday, in wake of the flattish indicators, KLCI is expected to lock in consolidation mode with key supports at 1529 (weekly lower BB) and 1517. Conversely, only a strong breakout above the support-turned-resistance 1548 will spur KLCI to refill 1558/1568 gap (28 Jan) and advance further towards 1578 (100D SMA) and 1600 territory.

Given the COVID-19 outbreak which has disrupted several supply chains moving out from China, it could thwart global growth and flag recession fears; KLCI’s upside could be capped in the near term ahead of the busy Feb reporting weeks. Nevertheless, we see potential trading opportunities in the construction and building materials segments in the anticipation of stimulus measure announcement by the government on 27 Feb.

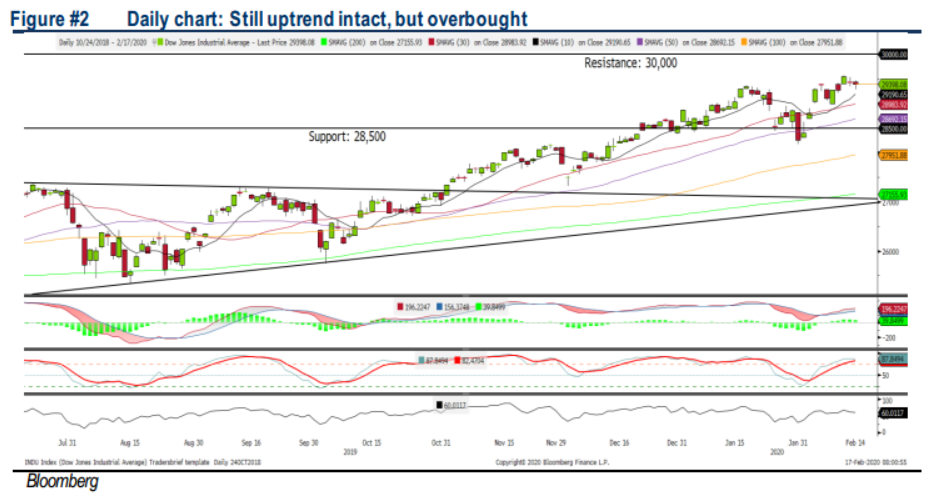

TECHNICAL OUTLOOK: DOW JONES

The Dow has trended sideways near the all -time-high region, the MACD Line is hovering above zero, while the MACD Histogram has weakened over the past two trading days. The Stochastic oscillator however, is overbought; hence the Dow’s upside could be limited around 29,500-30,000. Support is anchored around 28,500.

In the near term, the real impact of the coronavirus outbreak is still uncertain and the viral outbreak could pose a threat to global growth as the epidemic has spooked investors amid quarantines, supply-chain disruptions and factory shutdowns. Nevertheless, US investors found comfort in solid economic data, better-than-expected earnings reports and a signal that the Fed stands ready to act if needed. The Dow’s trading range will be located around 28,500- 30,000.

TECHNICAL TRACKER: Construction and Building Material

Recovering technicals and increasing trading interest. Last week, the Finance Ministry commented that a potential economic stimulus measure may be revealed (tentatively on 27th Feb) and the quantum will depend on the duration and impact of the Covid-19 outbreak. Although the stimulus measures could be targeting just the affected industries such as tourism, logistics and finance sector, we do not rule out that some of the mega projects (i.e. ECRL/ PTMP) may be expedited in 1H20. Also, soon after the comments by Finance Minister, construction (i.e. earthworks/pilling/consultant) and building material (steel and cement) segments have seen increasing trading interest. Should any announcement related to construction projects being revealed in the near term, it may trigger a broad base buying interest within the sector. We like HSSEB, MCEMENT and MELEWAR under this theme.

Source: Hong Leong Investment Bank Research - 18 Feb 2020

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

2

Good Articles to Share

Wall Street expert warns stock market is a 'really big accident waiting to happen'

3

Good Articles to Share

How insuring a pet may save money in the long run: Spot Pet CEO

4

Good Articles to Share

5

南洋 - 凭单专栏/温世麟

6

Good Articles to Share

Democrats might put ‘someone else’ in Kamala Harris’ place, GOP sen warns #shorts

7

Good Articles to Share

@tastyliveshow CEO: Betting on black swan events is ‘a complete waste of money’ #shorts

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....