Kenanga Research & Investment

Daily technical highlights – (POHKONG, TOMEI)

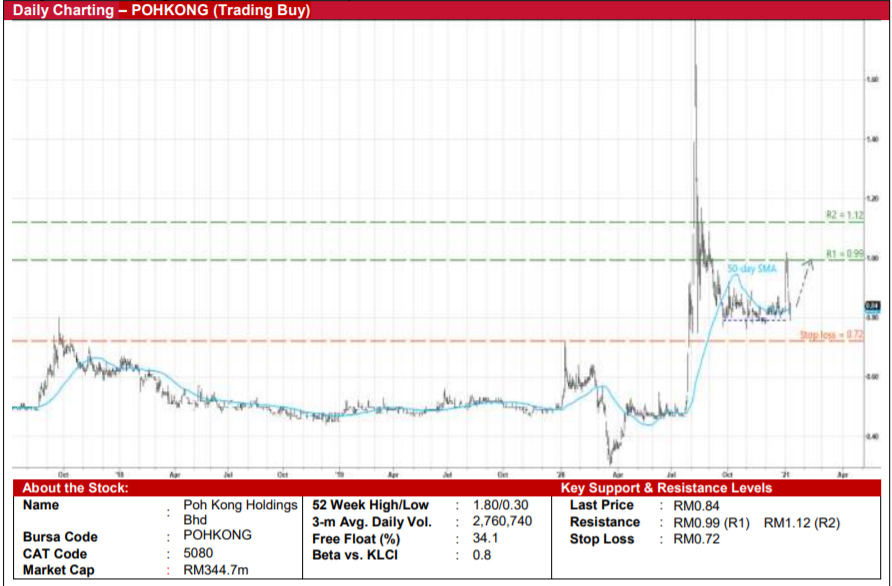

Poh Kong Holdings Bhd (Trading Buy)

• POHKONG, as a manufacturer cum retailer of jewellery in gold and gemstones, stands to benefit from: (i) higher gold prices, which would boost its profit margins given the lag effect of the gold raw material costs catching up with rising selling prices; and (ii) stronger Ringgit, as its raw materials (such as gold bars, diamonds and loose stones) are purchased in USD while the Group’s sales is denominated in Ringgit.

• With the USD (which has dropped 9% against the Ringgit since March last year) anticipated to weaken further going forward, this will likely lead to: (i) a continuation of the uptrend in gold prices, which tend to move inversely with the greenback (after the gold price has retraced 11% from a peak of USD2,075/oz in early August last year to USD1,850/oz currently); and (ii) better margins arising from lower raw material costs.

• Meanwhile, after posting net profit of RM24.4m (-3% YoY) in FY ended July 2020, the Group’s net earnings surged to RM14.6m (+81% YoY) in 1QFY21 mainly on account of higher gold prices.

• From a technical perspective, the stock is presently hovering near a horizontal support line (that has emerged following the share price’s plunge from its peak of RM1.80 in August last year) and around the 50-day SMA line.

• A likely resumption in buying interest (just like what happened early last week) could then push the stock towards our resistance thresholds of RM0.99 (R1; 18% upside potential) and RM1.12 (R2; 33% upside potential).

• Our stop loss price is pegged at RM0.72 (or 14% downside risk from yesterday’s close of RM0.84).

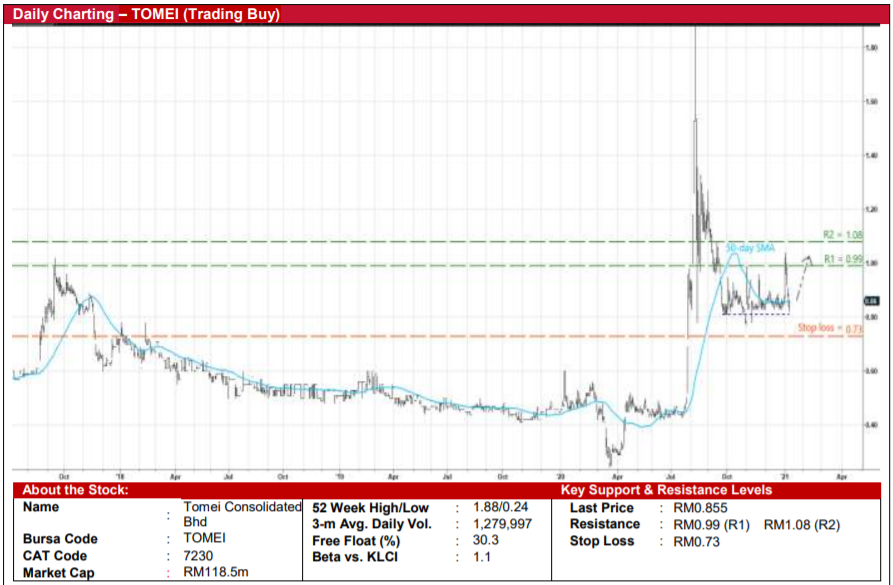

Tomei Consolidated Bhd (Trading Buy)

• TOMEI, as a manufacturer and retailer of gold, jewelleries and diamonds, is set to benefit from a weaker USD outlook, which could drive gold prices higher and lower the purchase cost of raw materials, and in turn translates to fatter profit margins for the Group.

• For 3QFY20, the Group saw its net profit jumped from RM2.1m a year ago to RM13.6m, taking its bottomline to RM19.5m (+222% YoY) for the nine-month ended September 2020 lifted by stronger profit margins.

• Technically speaking, TOMEI shares – after falling from a high of RM1.88 in August last year to settle at RM0.855 yesterday – could stage a rebound from a horizontal support line that stretches back to late September last year.

• A probable share price spurt – to break above the 50-day SMA line – will likely propel the stock to test our resistance thresholds of RM0.99 (R1) and RM1.08 (R2). This translates to upside potentials of 16% and 26%, respectively.

• We have placed our stop loss price at RM0.73 (or 15% downside risk).

Source: Kenanga Research - 12 Jan 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Kenanga Research & Investment

Actionable Technical Highlights - PRESS METAL ALUMINIUM HLDG BHD (PMETAL)

Created by kiasutrader | Nov 25, 2024

Actionable Technical Highlights - PETRONAS CHEMICALS GROUP BHD (PCHEM)

Created by kiasutrader | Nov 25, 2024

Weekly Technical Highlights – Dow Jones Industrial Average (DJIA)

Created by kiasutrader | Nov 25, 2024

Malaysia Consumer Price Index - Edge up 1.9% in October amid food price surge

Created by kiasutrader | Nov 25, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

3

4

5

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

6

7

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....