Kenanga Research & Investment

Daily technical highlights – (BONIA, PWROOT)

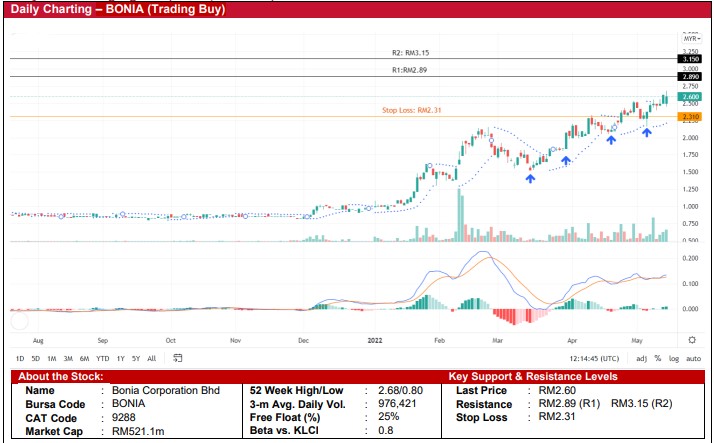

Bonia Corporation Bhd (Trading Buy)

• After breaking out from a sideways pattern in Dec 2021, BONIA’s share price has been trending upwards to form a sequence of higher highs and higher lows.

• With the Parabolic SAR indicator still rising and coupled with the bullish MACD signal, we anticipate that the stock will continue its upward trajectory.

• Thus, we believe that BONIA’s share price could climb towards our resistance thresholds of RM2.89 (R1) and RM3.15 (R2), which represent upside potentials of 11% and 21%, respectively.

• Our stop loss price level is set at RM2.31 (or a downside risk of 11%).

• Business-wise, BONIA is involved in the designing, manufacturing, retailing and wholesale of leatherwear, footwear, men’s apparel and accessories.

• BONIA reported a net profit of RM14.8m in 3QFY22 (-36% QoQ), which brought 9MFY22 net profit to RM32.9m (+128% YoY), lifted by the reopening of economic activities and strong consumer spending during festive seasons.

• Based on consensus forecasts, the group is expected to record a net profit of RM36.7m in FY June 2022 and RM48.9m in FY June 2023, translating to forward PERs of 14.2x and 10.7x, respectively.

• BONIA’s balance sheet is backed by net cash holdings and short-term funds of RM49.7m (translating to 24.8 sen per share) as of end March 2022.

Power Root Bhd (Trading Buy)

• PWROOT shares bounced up from a low of RM1.24 in March 2022 to form an ascending price channel since then.

• On the chart, the share price is expected to climb further in view of: (i) the rising Parabolic SAR indicator, (ii) the strengthening MACD signal, and (iii) the DMI Plus hovering above the DMI Minus.

• Riding on the positive momentum, the stock could rise to challenge our resistance levels of RM1.86 (R1; 11% upside potential) and RM2.02 (R2; 20% upside potential).

• We have pegged our stop loss at RM1.50, which represents a downside risk of 11%.

• Fundamental-wise, PWROOT is involved in the manufacturing and distribution of beverage products.

• The group reported a net profit of RM6.0m (+7% QoQ) in 3QFY22, which took 9MFY22 bottomline to RM13.7m (-48% YoY) as higher administrative costs (such as advertising and marketing expenses) and freight cost more than offset the higher sales in both the local and export markets.

• Going forward, in anticipation of robust domestic sales on the back of stronger consumer spending and improved ASPs, consensus is predicting PWROOT to report a net profit of RM19.5m in FY March 2022 before increasing to RM32.1m in FY March 2023, which translate forward PERs of 33.6x and 21x, respectively.

Source: Kenanga Research - 20 May 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Kenanga Research & Investment

Bond Weekly Outlook - MGS/GII likely to rise amid ongoing US economic resilience

Created by kiasutrader | Nov 22, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

2

3

Koon Yew Yin's Blog

CPO price is rising rapidly as shown by chart below - Koon Yew Yin

4

Axcapital's investment blog

KAB - Executing its way to a record quarter. Could more Petronas contracts be coming?

6

7

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....