Gadang was formerly known as Lai Sing Holdings Bhd which was incorporated in 1993 and listed in the second board of KLSE in 1994.

Current CEO Tan Sri Dato Kok Onn emerged as a major shareholder and took over the company's operation in 1997. The company's name was then changed to Gadang.

Gadang was transferred to main board in Dec 2007.

Gadang has 4 business segments which are

- construction

- property

- utility

- plantation

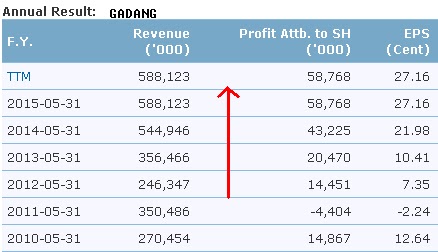

Its revenue and PATAMI grow for 4 consecutive years to a record high of RM588mil & RM58.8mil respectively in FY15 which ends on 31 May 2015.

The main growth driver is no doubt its construction and property divisions.

Construction

Construction is the bread and butter of Gadang. It contributes 76% of revenue and 58% PBT for the group in FY15.

The table below shows recent contracts secured by Gadang.

The table below shows recent contracts secured by Gadang.

| Date | Projects | Value | Completion |

| Jun14 | RAPID phase 2 | RM 350mil | Sep15 |

| May14 | Cyberjaya Housing Project | RM 1.055bil | 2023 |

| Oct12 | RAPID phase 1 | RM 312.8mil | Dec13 |

| Jul12 | MRT2 Kota Damansara-Dataran Sunway | RM 863.4mil | |

| Oct11 | Hospital Shah Alam | RM 410.9mil | 24 months |

| Jun11 | MRT2 phase 1 Sg Buloh depot | RM 23.9mil | 8 months |

| Jan10 | LCCT/KLIA runway (JV 70:30) | RM 291.2mil | Dec10 |

| Feb08 | Hospital Rehabilitasi Cheras (JV 55:45) | RM 341.8mil | May10 |

| Aug07 | LKSA package 1 (JV 50:50) | RM 278.9mil | Aug09 |

Its outstanding construction orders breached and stayed above RM1bil in FY12-FY14 thanks to the huge MRT2 jobs.

However, most jobs have been completed at the moment except the construction of MRT2 Kota Damansara - Dataran Sunway.

The Cyberjaya Housing Project is not included in the construction order book I guess, as it is regarded as a property development.

The Cyberjaya Housing Project is not included in the construction order book I guess, as it is regarded as a property development.

MRT2 progress at Dataran Sunway, May15

Gadang does not get any new construction job since Jun14. Though the management expected only RM100mil construction contract in FY15, there is actually none.

Jobs that it is bidding for are mainly related to RAPID. So the slow down in Oil & Gas sector certainly does not do it a favour.

So, perhaps its outstanding construction jobs should be much lower than RM700mil after the completion of its RAPID phase 2 at the end of this month.

Property

Gadang's property division did not do so well in my opinion compared to many other property developers.

It develops small projects here and there over the years.

Current active projects should be The Vyne in Sg Besi, Bandar Puncak Sena (GDV RM300mil) in Kedah and PR1MA project mentioned earlier in Cyberjaya.

I don't think Bandar Puncak Sena can contribute significantly to Gadang but The Vyne seems to be a good project with a GDV of RM500mil.

The Vyne

The Vyne which sits on a leasehold land Gadang acquired in 2010 for RM33mil, comprises 800 units high-end condominium in 5 blocks, which will be developed in 3 phases.

Phase 1 (Block A & B) has been launched around year 2013/14 and the construction of Black A has reached level 20 in May15.

Phase 2 (Block C & D) has also been launched probably last year but I'm not sure what is the latest sales status of these 2 phases.

According to an interview by MalayMailOnline published in Feb15, phase 1 & 2 of The Vyne were approximately 67% & 45% sold respectively, while phase 1A of Bandar Puncak Sena was 40% taken up.

The Vyne might be linked to an upcoming MRT station so it should get more interest from the market I guess.

Besides, Gadang has signed an agreement in May 2014 with government company Cyberview to jointly developed a PR1MA project known as Knowledge Workers Housing Project in Cyberjaya.

This is a huge project with GDV of RM1.055bil on a 109.3 acres land which should start in Q1 of 2015 and completed by Q2 of 2023.

It is expected to generate more than RM100mil revenue yearly to Gadang over a period of 8-9 years.

Phase 1 of this project has a GDV of RM150mil. However, I'm not sure how many shares Gadang has in this partnership.

Capital City

The talking point of Gadang recently is about the development of Capital City in Tampoi, Johor.

It is not a secret that Gadang's profit in the next 2-3 years will very likely be very very good because of this.

Gadang contributed the land for this project while Hatten Group & Sunbuild Development will build and sell the properties.

The whole Capital City development has a GDV of RM1.8bil. It consists of a retail mall known as Capital 21 (RM1.3bil), office suites or SOHO (RM200mil) and hotel suites (RM300mil).

So far the retail mall units have been launched in Dec13 and construction has started since Apr14. It is targeted to be completed in year 2017.

Gadang will get paid according to the construction progress of the mall.

In short, Gadang is entitled to a maximum of RM324mil for the whole project, with maximum profit of around RM220mil.

For the mall alone, Gadang can potentially get RM301mil, or profit of around RM200mil, paid in 4 stages in 3 years time until 2017.

Gadang will get payment for office & hotel suites only when they are launched later. The entire development is to be completed in 66 months according to the contract.

Gadang should have enjoyed some profit from Capital City in its FY15. Besides the land cost and tax, I think there is no other significant cost that Gadang needs to bear for this project.

In the next 2-3 years, I estimate that Gadang should get around RM50-60mil net profit per year in average from this project alone.

In the next 2-3 years, I estimate that Gadang should get around RM50-60mil net profit per year in average from this project alone.

The group's overall PATAMI in FY15 is RM58.8mil.

With the desire to grow its property division, Gadang has replenished its development landbank recently by acquiring:

- 62.84 acres freehold land in Semenyih for RM95.8mil in 2015 (potential GDV >RM450mil)

- 9.5 acres leasehold land in Taman Melawati KL for RM33.1mil in Jul14 (potential GDV RM505mil)

About its latest property unbilled sales, the only figure I can get is RM210mil in Nov14.

Utility

Gadang diversified into utility segment since 2005 by acquiring 100% of Singapore-based Asian Utilities Pte Ltd (AUPL) which has several water concessions in Indonesia.

In 2014, AUPL acquired 85% stake in PT Dewa Bangun Tirta (DBT) who has 25 years water treatment & supply concession starting from 2013 in Jawa Timur.

Yearly turnover of DBT is about Rp20bil (RM6mil).

Besides water supply, Gadang is also involved in hydropower generation in Indonesia by acquiring 60% of PT Ikhwan Mega Power (IMP) for RM3mil in 2014.

IMP has a 15-year 9 megawatt hydropower generation concession. However, the facility is still under construction and is expected to be completed by 2016.

Upon full commissioning, IMP is expected to generate yearly revenue of about Rp56bil (RM17mil).

In Jan15, Gadang added another 4 megawatt hydropower generation concession by acquiring 80% of PT Hidronusa Rawan Energi.

Management expects the whole utility segment to contribute RM20mil revenue in FY2016.

Plantation

I think Gadang's CEO likes recurring income. That's why he diversified into oil palm plantation as well.

Gadang acquired 5,181 acres of land in Ranau Sabah and planted it with oil palm trees in stages since 2009.

In 2015, trees planted in 2009 should have reached full maturity but too bad the CPO price is sluggish now.

Anyway, the plantation size is still small to make any meaningful contribution.

The management does not rule out further expansion of its plantation landbank in the future.

The management does not rule out further expansion of its plantation landbank in the future.

Overall, Gadang is a diversified group which depends on construction and property development.

Its construction division does not look too good at the moment with lack of contract award for the past one year.

Property division should do much better in FY16 with contribution from Capital City and The Vyne.

Earnings from utility segment should remain almost the same while plantation should see red again.

Gadang's PATAMI for FY15 is RM58.8mil.

So, Gadang's fully diluted EPS for FY15 will be about 25sen.

At current share price of RM1.18, it is trading at actual PE ratio of just 4.7x.

I think its PATAMI for FY16 will probably exceed RM70mil.

Its balance sheet and cash flow do not look bad either.

Any special reason why Gadang's share price is at RM1.18 now?

Is it because it is involved in property sector?

Anyway, what will Gadang do with the huge cash from Capital City land sale?

Jibailan2

No brained as loser! Drop from 1.40 to now.

2015-09-07 23:27