Good Articles to Share

Is AirAsia Group Bhd A Great Bargain Now? - Ian Tai

AirAsia Group Bhd (AAGB) is the largest low-cost carrier in Asia. It operates nine airlines in six countries across Asia. As of 9 June 2019, AAGB is valued at RM 9.7 billion in market capitalisation. In this article, I’ll bring an update on the airline’s latest financial results, major growth plans and valuation figures. Thus, here are 8 key things to know about AAGB before you invest.

-

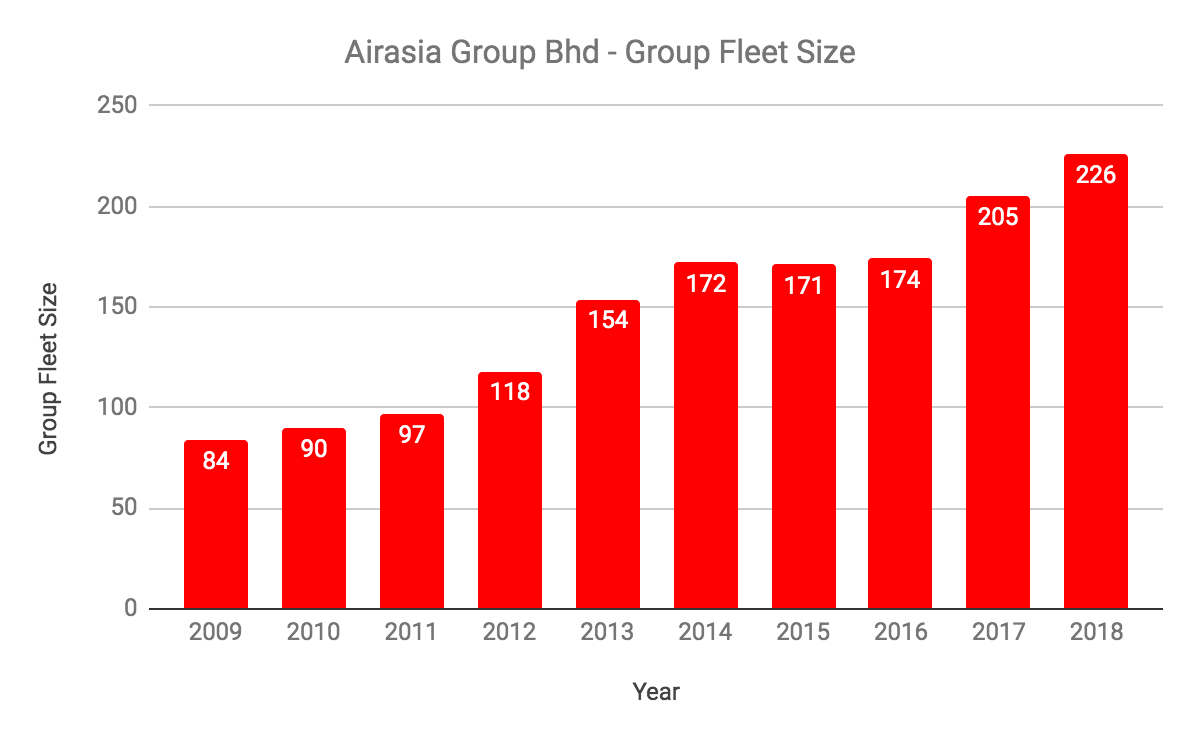

Fleet Size

AAGB has increased its fleet size from 84 aircrafts in 2009 to owning as much as 226 aircrafts in 2018. Out of which, 141 aircrafts are operating under Airasia Malaysia. The growth in fleet size is due to its continuous expansion in Airasia Malaysia and the launch and growth of Airasia in a handful of countries such as Indonesia, Thailand, the Philippines, India, and Japan during the 10-year period.

Source: AAGB’s Annual Reports

-

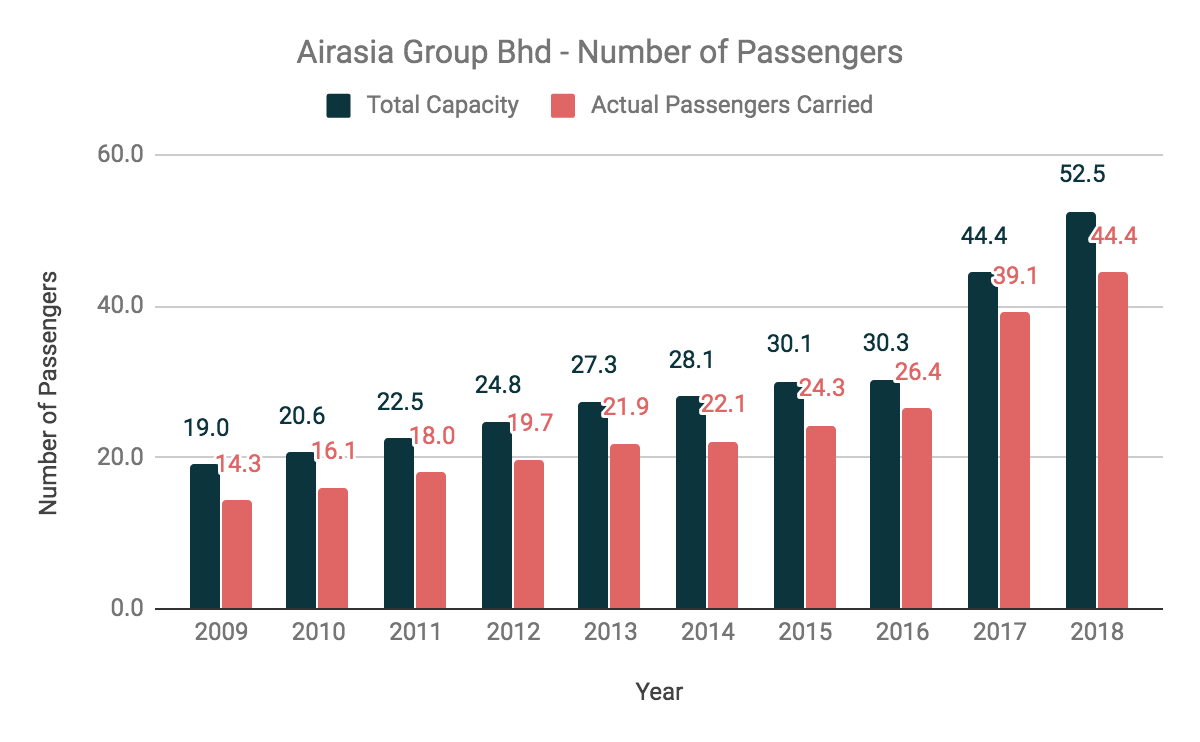

Total Capacity & Load Factor

As a result, AAGB increased its total passenger capacity from 19 million in 2009 to 53 million in 2018. In total, the number of actual passengers carried has grown from 14 million in 2009 to 44 million in 2018, hence, improving its load factor from 75% in 2009 to 85% in 2018.

Source: AAGB’s Annual Reports

-

Local Market Share

AAGB is enjoying significant local market share in Malaysia, Thailand & the Philippines. Its market share in Indonesia and India remains below 5% while Airasia Japan is fairly new. In 2018, Airasia Malaysia continues to be the bread and butter for AAGB as its overseas airlines are still not profitable.

|

Nations |

Revenue 2018 (RM Million) | Net Operating Profits 2018 (RM Million) | Domestic Market Share (%) |

| Malaysia | 8,900 | 4,806 | 58% |

| Thailand | 4,866 | 7 | 32% |

| Philippines | 1,602 | -155 | 20% |

| Indonesia | 1,191 | -266 | 2% |

| India | 1,317 | -365 | 5% |

| Japan | 69 | -162 | n/a |

Source: AAGB’s Annual Report 2018 & Airasia 3.0 Presentation in April 2019

-

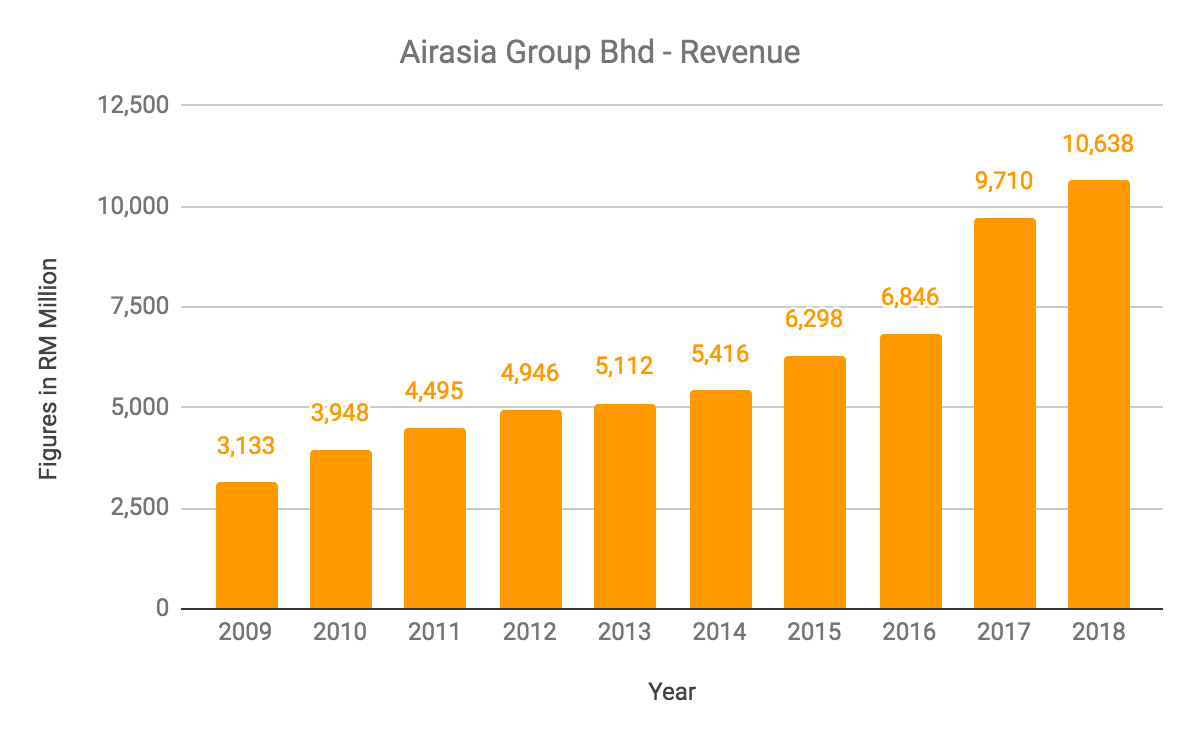

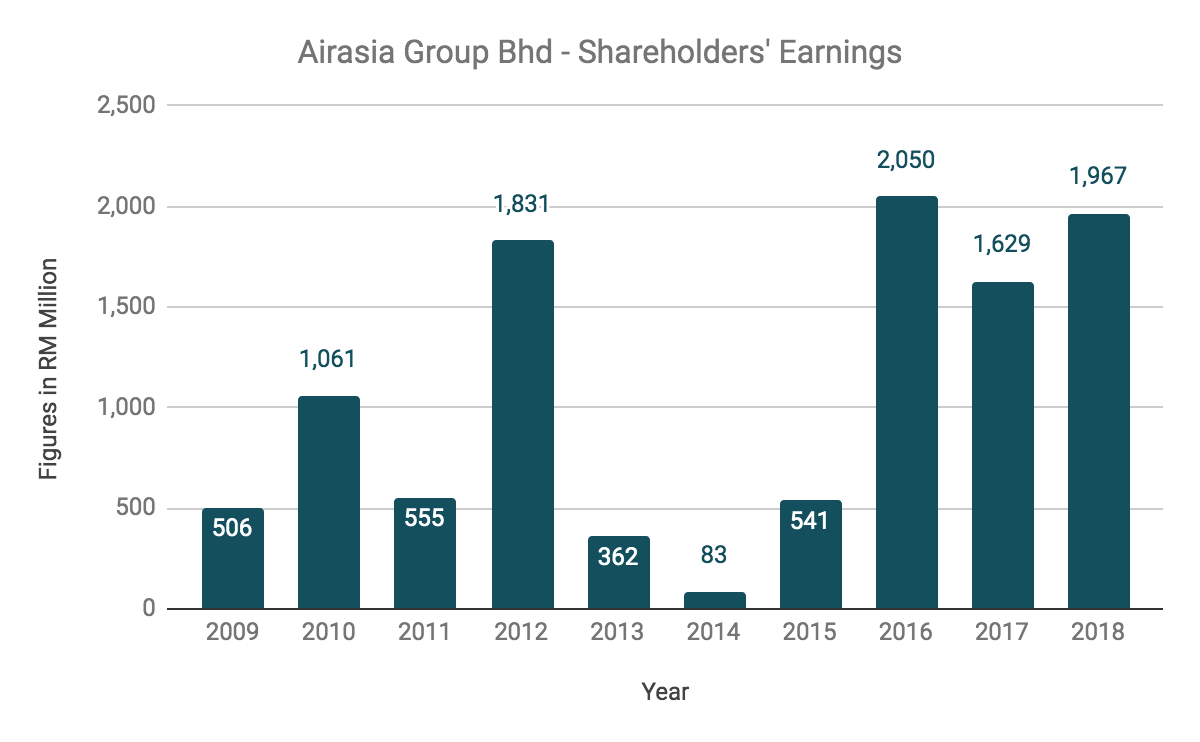

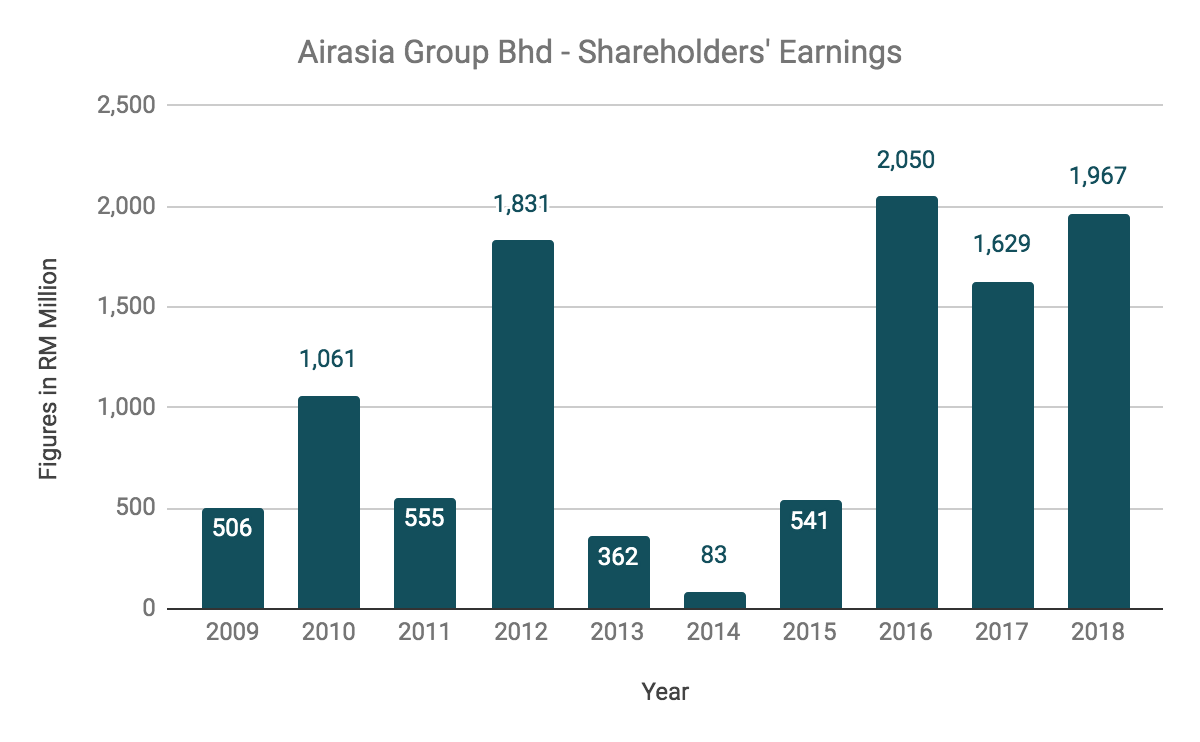

Financial Results

In line with its fleet expansion, AAGB has achieved continuous increase in total revenues from RM 3.1 billion in 2009 to RM 10.6 billion in 2018. Its shareholders’ earnings, however, were volatile as it was impacted by fuel prices and numerous one-off gains and losses such as:

– Fluctuations of Foreign Exchanges

– Fair Value Changes in Derivatives

– Purchase and Disposal into subsidiaries, associates and joint ventures

– Disposal of property, plant, and equipment

Source: AAGB’s Annual Reports

-

Latest 12-Month Results

For the last 12 months, AAGB has generated RM 10.8 billion in revenue and RM 978.8 million in shareholders’ earnings or 29.3 sen in earnings per share (EPS). In Q4 2018, AAGB has recorded a substantial RM 395.0 million in quarterly losses. This is because it incurred RM 254 million in additional fuel expenses due to a hike in jet kerosene prices and a total of RM 318 million in one-off expenses.

Figures in RM Million unless stated otherwise

| Year | Q2 2018 | Q3 2018 | Q4 2018 | Q1 2019 | Total |

| Revenues | 2,624 | 2,609 | 2,823 | 2,780 | 10,836 |

| Earnings | 362 | 916 | -395 | 96 | 979 |

| EPS (Sen) | 10.8 | 27.4 | -11.8 | 2.9 | 29.3 |

Source: AAGB’s Quarterly Reports

-

Balance Sheet Strength

AAGB has reduced its non-current liabilities substantially over the last 5 years, down from RM 12.0 billion in 2014 to RM 5.5 billion in 2018. This had resulted in a substantial fall in gearing ratio from 263.4% in 2014 to 89.2% in 2018.

In 2019, AAGB has adopted the MFRS 16 accounting policy. It measures lease liabilities based on the present value of future lease payments on its right-of-use assets. The adoption of this policy has increased AAGB’s asset column and liabilities column by RM 9.4 billion and RM 9.6 billion respectively. As a result, AAGB’s gearing ratio increased substantially to 201.0% in Q1 2019 from 89.2% in Q4 2018.

AAGB has reported to have RM 8.8 billion in current assets and RM 8.4 billion in current liabilities. Thus, its current ratio is 1.05.

-

Airasia 3.0

AAGB aspires to be the preferred travel & digital platform in Southeast Asia. It would focus on three areas for growth. They include:

Airline

AAGB intends to complete net addition of 18 aircrafts in 2018 and thus, move towards owning 500 aircrafts by 2020. In addition to growing key markets, AAGB is exploring opportunities for expansion in China and as well as in Vietnam.

Source: Airasia 3.0 Presentation in April 2019

Digital

AAGB remains big on data. Moving forward, it has identified a number of new data sources to drive expansion across AAGB’s ecosystem. They include statistics in airport terminals such as

– Passengers’ queue time.

– Weight of Passengers and Cabin Baggage

– Passengers’ Movements

– Counter Transactions … etc.

They enable AAGB to identify brand new sources of revenues and also opportunities for cost reductions.

Technology

AAGB intends to further develop its marketplaces which include a few major websites such as Airasia.com, BigPay, and Teleport.

Airasia.com will be developed into a comprehensive travel and lifestyle marketplace which encompasses online travel, ecommerce, media, and ride-hailing activities such as transportation and food delivery.

BigPay is one of the fastest growing fintech companies in Malaysia with over 0.5 million users to-date since its launch in January 2018. BigPay is Asia’s Money App which offers services such as e-wallet, remittances, & loans to millenials and travelers in Southeast Asia.

Teleport is established to simplify cargo supply chain, thus, significantly reducing air cargo fulfillment from 138 hours to around 12 hours. Thus, it allows AAGB to tap into rising demand for both social commerce and ecommerce across Southeast Asia.

-

Valuation Figures

As of 9 June 2019, AAGB is trading at RM 2.90 a share. In Point 5, AAGB made 29.3 sen in EPS. Thus, its current P/E Ratio is 9.90. For Q1 2019, it has reported to have RM 2.47 in net assets share. Therefore, AAGB has a current P/B Ratio of 1.17, which is below its 10-year average of 1.462.

AAGB has paid out 12.0 sen in dividends per share (DPS) per annum for the last 3 years. Thus, it offers a dividend yield of 4.14% per annum if it is able to maintain its DPS at 12.0 sen in subsequent years to come. The dividend figures are exclusive of a special dividend of 40.0 sen in 2018. This is because the 40.0 sen in special DPS are paid from one-off profits derived from the sale of 79 aircrafts and 14 engines in 2018.

VIA’s Verdict

AAGB has been aggressive in expanding its markets and sources of income. This had resulted in stable growth in revenues for the past 10 years. But, it recorded a lot of one-off transaction gains and losses and has been (and will be) affected by the ups and downs in fuel prices. They caused AAGB’s earnings to be volatile as shown in the graph below. It has caused AAGB’s stock price to be volatile too for the last 10 years.

Source: AAGB’s Annual Reports

Source: Google Finance

Are you able to find the resemblance between the two charts above? Volatility in profits had caused stock prices to be volatile.

The question is: ‘Would you invest in AAGB at RM 2.90 a share today?’

https://valueinvestasia.com/is-airasia-group-bhd-a-great-bargain-now/

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Good Articles to Share

India's Modi denies stoking divisions to win election, files nomination

Created by Tan KW | May 14, 2024

China strongly opposes U.S. tariff hikes, pledging measures to defend rights

Created by Tan KW | May 14, 2024

LIVE: Protests as Georgian parliament holds final reading of the 'foreign agents' law

Created by Tan KW | May 14, 2024

Ukraine asks Blinken for air defenses during surprise visit | REUTERS

Created by Tan KW | May 14, 2024

Discussions

Be the first to like this. Showing 15 of 15 comments

10billion and growing company with pe of only 9, it is definitely worth more than rm2.7 imo

2019-06-23 22:03

(US/CHN trade war doesn't matter) Philip

Instead of using or, fleet size, market share etc, the most important metric in investing in an airline is one which no one seems to pay attention to.

What is air Asia seat cost per mile (or km). It doesn't matter how big your market share is or how many planes you own. If your total seat cost per mile is lower than the competition and still profitable, then the whole system works.

Problem is when fuel and ancillary costs escalate and the selling price per seat doesn't make sense, then losses can loom far faster than one can imagine.

My flight from kk to kl cost me rm214 return ticket. It's definitely good for me and keeps a full flight, but is it a workable system for air Asia investors?

2019-06-23 22:13

tony Fernandez wants people to value AA as internet company but Malaysia too small and no scale

2019-06-24 07:11

Hahahaha,

Good morning qqq3 the pro trader, who trade the good, the worst, the ugly and the beautiful why hold only slow moving 4 stocks. Shouldn’t you change to fast and furious Dayang, Naim, Yinson, Hibiscus or even Inari for trading?

Posted by qqq3 > Jun 11, 2019 9:25 AM | Report Abuse

this rally, I only have 4 stocks....Ekovest, Armada, Jaks, Teo Seng.....all also do just as well as Dayang yesterday.......

2019-06-24 07:33

Dayang I bot at 1.02 sold at 1.09...next day 1.20.............of course I sold 1 day too soon.

2019-06-24 07:42

G20 meeting this week end................I have one week window to play......no more.

2019-06-24 07:44

Hahahaha,

qqq3 learn from CPTeh how to day trade for 3 cents profit. Then you have many more days to trade for profit but remember to cutloss when things go the other way othwrwise CPTeh will laugh at you for holding high.

2019-06-24 08:15

Post a Comment

Featured Posts

MQ Trading Signals

Time

Signal

Duration

Type

2024-05-14 16:35:00

TURTLE SYSTEM 20

5 Mins

BUY

2024-05-14 16:30:00

EMA 5

10 Mins

BUY

2024-05-14 16:30:00

TURTLE SYSTEM 20

10 Mins

BUY

2024-05-14 16:20:00

EMA 5

5 Mins

BUY

2024-05-14 16:20:00

ADX

5 Mins

BUY

Apps

Top Articles

1

Koon Yew Yin's Blog

2

3

4

save malaysia!

5

Good Articles to Share

6

THE INVESTMENT APPROACH OF CALVIN TAN

7

RHB Investment Research Reports

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Value Investor Coo1eo

Check soem typo. Also where is the point of the impending social dividend declared. 90sen???

2019-06-23 14:00