Money Thoughts

5 Minute Read: REVENUE (0200)

xiiaolol1996

Publish date: Fri, 06 Mar 2020, 11:34 PM

xiiaolol1996

0 4

Sharing weekly financial news and thoughts in Malaysia stock market

REVENUE (0200)

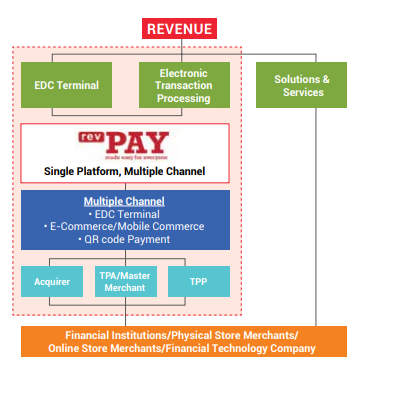

Listed in ACE Market July 2018, Revenue Group Bhd is mainly a payment solution platform provider. The company provides rental and sale of electronic data capture (EDC) terminal, EMV Smart Card Technology, Terminal Management System, Loyalty System, Consumer Behavioural Management System, Web-based Payment System, and Payment Transaction Management System. The company alliance partners include AmBank, Affin Bank Real Rewards, Comex GeneSys, Visa, MasterCard, MEPS, VeriFone, Petronas, Touch ’n Go and many more. The company provide the latest technological framework while keeping operational low costs and provide the supporting infrastructure for who need it.

Business Model

It has three segments which contributes to its business revenue:

Electronic Data Capture (EDC) terminals

EDC terminal, as shown in the Figure above, is a device used to read information encoded in bankcard's magnetic stripe, perform authorization, store and transmits the data to the acquirer for processing. In simple terms, the EDC machine act as a middleman that allows you and the merchant to perform transactions in a cashless environment. It contributes to an average 45% to 55% of its total revenue, and its gross profit margin (GPM) stands at around 40% to 50% including its rental, sales and maintenance of the EDC terminal.

Electronic Transaction Processing (ETP)

Electronic transaction processing, as its name suggest, is a profit received when a transaction is processed. When the EDC terminal is used for transactions, REVENUE takes up certain amount of commission in every bankcard's transaction value called Net Merchant Discount Rate (MDR). It also generate revenue from a pre-determined commission earned from the processing of electronic transactions via e-commerce or mobile channel like e-wallet transaction (Touch'N Go, Grab, etc). It is the SECOND largest contributor to REVENUE's revenue taking up 30% to 40% of its total revenue. Its gross profit margin stands at a high of 75% which really are the money-making tree for REVENUE. If there are more transactions, there will be more ETP generated.

Solution, Shared Services

In the solution, shared services segment, the group provides IT solution and services, digital payment services, and procurement logistic services. Although its generated revenue is small, it is slowly growing since 2018 and its margin is really high too, standing at around 75% to 80%.

Financial Health

Revenue & Profit Margin Growth

To evaluate whether a company is performing well, the first condition is it must be growing steadily. You can see from the figure above that from 3-2018, The Group's revenue has been growing at least 40% a year. This is a REALLY GOOD sign that the group is currently on the right track and the products and services that they provide are in high demand. Its NET profit margin, maintained above 12% for the past 8 quarters.

Balance Sheet Strength

Current Ratio (CR) is currently 2.11, which is considered healthy. Debt-to-Equity ratio (D2E), is at 0.51 which shows the company has minimal debt and its cash flow are still healthy for the company's normal operations. In the Group's Annual Report 2019, You can see the receivables increased by RM10million (almost 100%), and its payables also increased by RM6 million (160%), indicating the company has HIGH demand on its products, where its inventories also increased by RM4.42 million. The debt has been growing, but the Group has been managing it well to keep the CR above 1.5 and D2E under 0.5. Any sign of D2E above 0.5 should be a warning sign.

If the company's receivables is significantly higher than its payables, it might face difficulty in cash flow, because no one is paying the company's money and its difficult to continue operations. To understand this, we look at its cash flow statement:

To make things simpler for everyone else and make this article not 100,000 words, I will just talk about the overall view from its cash flow. Net cash generated operating activities has decreased RM10 million as compared to last year, because the company bought a lot of new equipments (Inventories) as I said before, and its increment in receivables is higher than its payables, it will have a decrease in net cash. However, you can see the company's confidence in its expansion where its net cash used in investing activities increased by RM6million. Its net cash from financing activities increased by 18 million, mainly attributed to the money raised from its initial public offering (IPO).

Management Overview

The Group is lead by Mr. Eddie Ng Chee Siong, The CEO which has 15 years of experience in local electronic payments industry. In 2003, He co-founded Revenue Harvest with two of his friends Mr. Brian Ng and Mr. Dino Ng ShihFang. Mr. Brian, the Chief Operating Officer (COO) who was a senior engineer of an optician R&D department help led the day-to-day operations of the group. Mr. Dino, the Group Technology Officer is responsible for payment security related systems. Good as everyone is very experienced.

Major Risks

- Heavily reliant on major customers. If one customer stopped working with the group, the group may incur heavy losses.

- Moderately affected by the fluctuations in USD/MYR exchange as EDC terminals are purchased in USD. Depreciation of MYR will increase the expenses and lower the overall margin of the operations. Its also affected by China RenMinBi/MYR as one of their online merchants operates a marketplace (e-commerce) in China.

- Rapid changes in regulations where the current technology become obsolete. The group might have to write off or impair big amount of equipment at the time they are required to follow new regulations. However, the group continue to innovate and maintain its products to the latest technology.

Valuations

- Price-to-Earning Ratio (P/E) - 50

- Return on Equity (ROE) - 16%

- NTA - 0.27

First of all, is P/E ratio of 50 high? It looks high right? A high P/E ratio can mean two things, either the company is overvalued (Value Investing), or its stock are highly demanded (Growth Investing). An electronic payment stock cannot be simply evaluated by looking at its P/E, because its an up-trending & growing stock in a rapidly escalating industry. Comparing to its peer, GHLSYSTEM which has been listed for more than 10 years, has a P/E of 43. Paypal, the world's largest electronic payment system, has a P/E of 50. Hence, P/E ratio of 50 for Revenue can be considered FAIR.

Its ROE stands at 16%, which is healthy as long the group is able to maintain a good ROE quarterly. Some industries have a high ROE as they require little or no assets while others require large infrastructure builds before they generate profit. For Revenue which has very high margin, I will expect an ROE of at least 15% and above and any value below that will indicate a bad management either in cost management and margin control. NTA is slightly low compared to its price but it is fine for an IT stock as it has been growing for the past 8 quarters.

My Evaluation

E-wallet has been trending where the government has been pushing initiatives like E-Tunai Rakyat program encouraging people towards cashless environment. This will continue to be the main driving force for the Group's revenue as the current market exposure towards cashless environment are still little. Eventually, revenue generated by electronic transaction processing will be more than EDC, as there will be only be limited growth of total merchants but ample space for ETP to grow. Revenue's competitor GHL, currently has an ETP of 65% to 35% roughly of ETP vs EDC whereby Revenue is currently at 45-45-10 (EDC-ETP-SS). Bear in mind that there might be sign of a stagnant market whereby its ETP earnings has been growing slower as compared to 2018. This might be an indication of a market stagnation where the market already has enough EDC terminals.

At this point of time of writing, fears of Wuhan continue to loom and IT IS EXPECTED than The Group's earning in ETP and EDC will be affected as economy grow slower (they are dependent on total spending in the market). I still favor electronic payment industry very much and with only two company to choose from the sector, Revenue perform significantly better than GHLSystem (I might write this in another post in the future) in terms of their margins, growth and prospects. To fight Wuhan virus, China banks are destroying and disinfecting $600 billion paper notes (Yuan) and this further improved my prospect towards the benefit of a cashless society. In the future, cryptocurrency (cashless) will be ruling over paper notes and I foresee a slightly worse economy projection in Malaysia 2020 but surely the sky will be blue after everything settle down. Who knows it might a blessing in disguise for us investors?

Click the link to join my English Malaysian Stock Discussion Grou!

Disclaimer: I do not suggest any stocks purchase or buying as these are merely analysis on the stocks. Your investment decision are purely YOURS and ALL YOURS and I do not take any responsibility on your gain/loss.

REVENUE (0200)

Listed in ACE Market July 2018, Revenue Group Bhd is mainly a payment solution platform provider. The company provides rental and sale of electronic data capture (EDC) terminal, EMV Smart Card Technology, Terminal Management System, Loyalty System, Consumer Behavioural Management System, Web-based Payment System, and Payment Transaction Management System. The company alliance partners include AmBank, Affin Bank Real Rewards, Comex GeneSys, Visa, MasterCard, MEPS, VeriFone, Petronas, Touch ’n Go and many more. The company provide the latest technological framework while keeping operational low costs and provide the supporting infrastructure for who need it.

Business Model

It has three segments which contributes to its business revenue:

Electronic Data Capture (EDC) terminals

EDC terminal, as shown in the Figure above, is a device used to read information encoded in bankcard's magnetic stripe, perform authorization, store and transmits the data to the acquirer for processing. In simple terms, the EDC machine act as a middleman that allows you and the merchant to perform transactions in a cashless environment. It contributes to an average 45% to 55% of its total revenue, and its gross profit margin (GPM) stands at around 40% to 50% including its rental, sales and maintenance of the EDC terminal.

Electronic Transaction Processing (ETP)

Electronic transaction processing, as its name suggest, is a profit received when a transaction is processed. When the EDC terminal is used for transactions, REVENUE takes up certain amount of commission in every bankcard's transaction value called Net Merchant Discount Rate (MDR). It also generate revenue from a pre-determined commission earned from the processing of electronic transactions via e-commerce or mobile channel like e-wallet transaction (Touch'N Go, Grab, etc). It is the SECOND largest contributor to REVENUE's revenue taking up 30% to 40% of its total revenue. Its gross profit margin stands at a high of 75% which really are the money-making tree for REVENUE. If there are more transactions, there will be more ETP generated.

Solution, Shared Services

In the solution, shared services segment, the group provides IT solution and services, digital payment services, and procurement logistic services. Although its generated revenue is small, it is slowly growing since 2018 and its margin is really high too, standing at around 75% to 80%.

Financial Health

Revenue & Profit Margin Growth

To evaluate whether a company is performing well, the first condition is it must be growing steadily. You can see from the figure above that from 3-2018, The Group's revenue has been growing at least 40% a year. This is a REALLY GOOD sign that the group is currently on the right track and the products and services that they provide are in high demand. Its NET profit margin, maintained above 12% for the past 8 quarters.

Balance Sheet Strength

Current Ratio (CR) is currently 2.11, which is considered healthy. Debt-to-Equity ratio (D2E), is at 0.51 which shows the company has minimal debt and its cash flow are still healthy for the company's normal operations. In the Group's Annual Report 2019, You can see the receivables increased by RM10million (almost 100%), and its payables also increased by RM6 million (160%), indicating the company has HIGH demand on its products, where its inventories also increased by RM4.42 million. The debt has been growing, but the Group has been managing it well to keep the CR above 1.5 and D2E under 0.5. Any sign of D2E above 0.5 should be a warning sign.

If the company's receivables is significantly higher than its payables, it might face difficulty in cash flow, because no one is paying the company's money and its difficult to continue operations. To understand this, we look at its cash flow statement:

To make things simpler for everyone else and make this article not 100,000 words, I will just talk about the overall view from its cash flow. Net cash generated operating activities has decreased RM10 million as compared to last year, because the company bought a lot of new equipments (Inventories) as I said before, and its increment in receivables is higher than its payables, it will have a decrease in net cash. However, you can see the company's confidence in its expansion where its net cash used in investing activities increased by RM6million. Its net cash from financing activities increased by 18 million, mainly attributed to the money raised from its initial public offering (IPO).

Management Overview

The Group is lead by Mr. Eddie Ng Chee Siong, The CEO which has 15 years of experience in local electronic payments industry. In 2003, He co-founded Revenue Harvest with two of his friends Mr. Brian Ng and Mr. Dino Ng ShihFang. Mr. Brian, the Chief Operating Officer (COO) who was a senior engineer of an optician R&D department help led the day-to-day operations of the group. Mr. Dino, the Group Technology Officer is responsible for payment security related systems. Good as everyone is very experienced.

Major Risks

- Heavily reliant on major customers. If one customer stopped working with the group, the group may incur heavy losses.

- Moderately affected by the fluctuations in USD/MYR exchange as EDC terminals are purchased in USD. Depreciation of MYR will increase the expenses and lower the overall margin of the operations. Its also affected by China RenMinBi/MYR as one of their online merchants operates a marketplace (e-commerce) in China.

- Rapid changes in regulations where the current technology become obsolete. The group might have to write off or impair big amount of equipment at the time they are required to follow new regulations. However, the group continue to innovate and maintain its products to the latest technology.

Valuations

- Price-to-Earning Ratio (P/E) - 50

- Return on Equity (ROE) - 16%

- NTA - 0.27

First of all, is P/E ratio of 50 high? It looks high right? A high P/E ratio can mean two things, either the company is overvalued (Value Investing), or its stock are highly demanded (Growth Investing). An electronic payment stock cannot be simply evaluated by looking at its P/E, because its an up-trending & growing stock in a rapidly escalating industry. Comparing to its peer, GHLSYSTEM which has been listed for more than 10 years, has a P/E of 43. Paypal, the world's largest electronic payment system, has a P/E of 50. Hence, P/E ratio of 50 for Revenue can be considered FAIR.

Its ROE stands at 16%, which is healthy as long the group is able to maintain a good ROE quarterly. Some industries have a high ROE as they require little or no assets while others require large infrastructure builds before they generate profit. For Revenue which has very high margin, I will expect an ROE of at least 15% and above and any value below that will indicate a bad management either in cost management and margin control. NTA is slightly low compared to its price but it is fine for an IT stock as it has been growing for the past 8 quarters.

My Evaluation

E-wallet has been trending where the government has been pushing initiatives like E-Tunai Rakyat program encouraging people towards cashless environment. This will continue to be the main driving force for the Group's revenue as the current market exposure towards cashless environment are still little. Eventually, revenue generated by electronic transaction processing will be more than EDC, as there will be only be limited growth of total merchants but ample space for ETP to grow. Revenue's competitor GHL, currently has an ETP of 65% to 35% roughly of ETP vs EDC whereby Revenue is currently at 45-45-10 (EDC-ETP-SS). Bear in mind that there might be sign of a stagnant market whereby its ETP earnings has been growing slower as compared to 2018. This might be an indication of a market stagnation where the market already has enough EDC terminals.

At this point of time of writing, fears of Wuhan are still looming and IT IS EXPECTED than The Group's earning in ETP and EDC will be affected as economy grow slower (they are dependent on total spending in the market). I still like electronic payment industry very much and with only two company to choose from the sector, Revenue perform significantly better than GHLSystem (I might write this in another post in the future). I foresee a slightly worse economy projection in Malaysia 2020 but hopefully there won't be any major incidents happening in any imminent future.

Click the link to join my English Malaysian Stock Discussion Grou!

Disclaimer: I do not suggest any stocks purchase or buying as these are merely analysis on the stocks. Your investment decision are purely YOURS and ALL YOURS and I do not take any responsibility on your gain/loss.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Money Thoughts

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Stock Market Enthusiast

Top 3 AI/Data Center Newsflow for the 3rd Week of December - #TENAGA, #YTL, #YTLPOWER

2

save malaysia!

3

Good Articles to Share

4

Good Articles to Share

5

Good Articles to Share

Gaza ceasefire deal 'closer than ever', says Hamas and two allies

6

Good Articles to Share

Ryan Serhant makes bold pitch to fix the housing ‘affordability crisis’

7

Good Articles to Share

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....