Money Thoughts

Rate Cut. How to Select a Bank Stock?

xiiaolol1996

Publish date: Wed, 04 Mar 2020, 07:18 AM

xiiaolol1996

0 4

Sharing weekly financial news and thoughts in Malaysia stock market

Hello,

Today BNM announced another rate cut by 25 bps to 2.50% from 2.75% as the central bank is "intended to provide a more accommodative monetary environment to support the projected improvement in economic growth amid price stability". This is the SECOND time the central bank cut the overnight policy rate (OPR) this year and it is expected as the political uncertainties domestically and the economy slowdown globally will starts to drag down Malaysia's economy growth in the next few quarters. Rate cut will stimulate the economy's growth positive but it is too broad to talk about all aspects.

Hence I would like to focus on How to select a Bank Stock?

The Rate Cut's Impact

Interest rate cut lowers the minimum interest charged by the banks to the lessee (the tenant), with the intention to stimulate growth with the loan interest getting lower and more money will flow into the market. Everybody said banks will get affected by interest rate cut but how exactly and where exactly?

Bank's Operation

When the interest rates dropped, more people can borrow. This is mainly because fixed deposit (FD) or bonds yield will drop, and people tend to look for alternative to invest. That is why exactly how interest rate cut stimulate the economy. People take out money from their fixed deposit and inject it into the market (stocks, bonds, real estates) whatsoever because the yield is just higher!

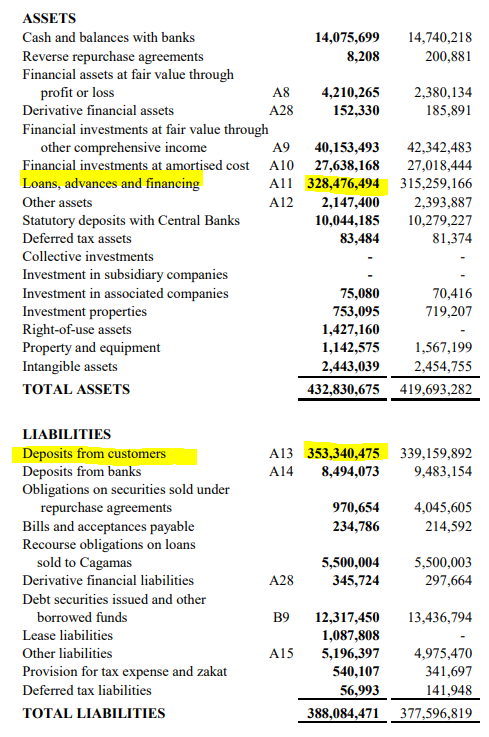

Taking Public Bank (PBBANK)'s latest QR (4Q19) as example, we can see that PBBANK's cash deposit from customers is around RM353 billion, up RM14 billion from Dec'18. Its loan take up RM330 billion, which is around 93% of the total cash deposit of customers. To remain competitive, banks always keep its rate as low as possible but it cannot be lower than the OPR rate. Hence, the more money they have, the higher the interest they can generate using a fixed interest rate. When they have lesser money, they can borrow lesser and their NIM drop. Simple right?

So people asked me, which bank will get affected the most from the OPR cut? List of banks are CIMB, MAYBANK, HLB, AMBANK, BIMB, PBBANK and so on. I would like to take an example for CIMB and PBBANK. As you know, CIMB today dropped -2.17% while PBBANK rose 3.98%. Same same bank why different story?

Three parameters that I used to evaluate bank: ROE, Price-to-Book Ratio (P/B), and NIM.

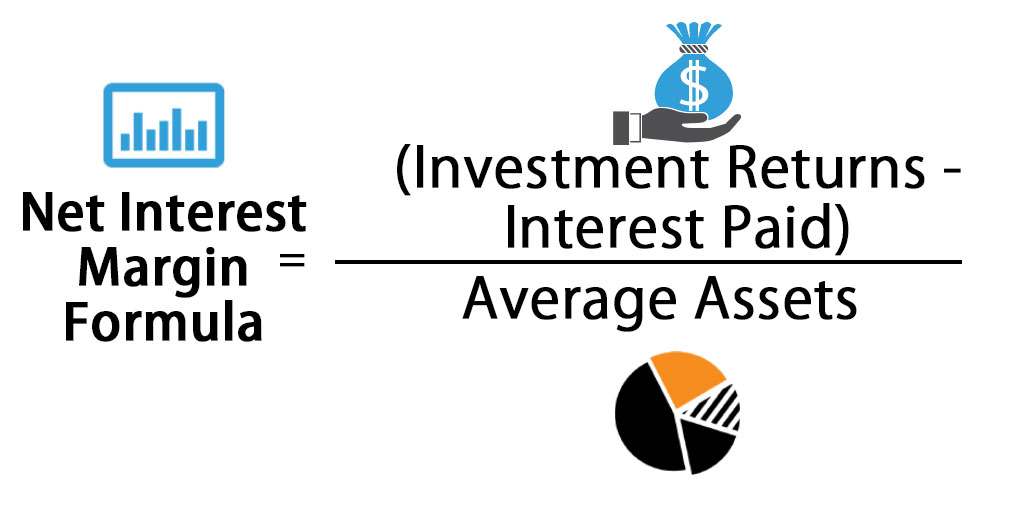

Net Interest Margin (NIM)

Banks typically makes money from three things: net interest margin (NIM), interchange fees and other services fees.

Banks make profit by lending money to other. Net interest margin (NIM) is the difference between amount of interest gained by lending to others and the amount of money that is required to pay to the lender divided by total assets.

Interest income takes up almost 90% of a bank's revenue so logically a high NIM will represent a highly attractive banking stocks. Is looking at only NIM enough though? NO! NIM does not account for fees and non-interest incomes that banks generate through services related to brokerage and deposit accounts and therefore we will need other parameter to judge the bank stocks.

Importance of ROE

ROE is one of the key indicator for banks' stocks. People always talk about ROE ROE. So how important is ROE? Lets use an example to remember better:

CIMB's total asset is RM573 billion, while PBBank's total asset is RM473 billion as of 4Q2019.

Logically, as banks earn money by earning interest lending out their money, given same interest rate, CIMB SHOULD earn more than PBBANK. Right?

Look at CIMB and PBBANK's profit for last quarter.

Having lower amount of assets, PBBANK earns MORE THAN DOUBLE what CIMB earns. What makes the difference? The differences comes in as CIMB has higher debts, higher expenses and this lower down its shareholder's equity (Equity = Total Asset minus Total Liabilities). Hence, if CIMB has higher debts and expenses, it will reflect in its shareholder's equity. That's when ROE comes in:

ROE = Net Income / Shareholder's Equity

The higher the ROE, the better the organization manages the shareholder's money to generate income. ROE of CIMB and PBBANK stands at 8.1 and 12.64 respectively, meaning that PBBANK manages money better than CIMB.

Why Price-to-Book Ratio (P/B)

In banks, we always look at price-to-book ratio. The lower, the better. The price-to-book ratio, or P/B ratio, is a financial ratio used to compare a company's book value to its current market price. P/B ratios are often used to compare banks, because most assets and liabilities of banks are constantly valued at market values.

P/B = Share Price / Book Value

CIMB has a P/B ratio of 0.79, while PBBANK has a P/B ratio of 1.58. This means CIMB is significantly undervalued in terms of P/B as compared to PBBANK. But does that mean CIMB is a good buy, or PBBANK is a bad buy? Not necessarily because the raise in P/B ratio might be caused by the expectations and confidences from its investors that it will generate profit in the future. A low P/B ratio might be due to its recent drop in share price due to bad quarters. Always research before judging anything.

My Evaluation

Having said all these, banking stocks will take a short dip but I believe after the Muhyidin's takeover Malaysia's stocks should perform better as the political uncertainties fade away. From the stimulus package, all banks are required to provide financial relief in the form of payment moratorium comprising restructuring and rescheduling loans for affected businesses and individuals. However, as economy is expected to slow down further due to the CoVid outbreak, banks might suffer more bad debts and defaults as lenders face difficulties in their business. I personally prefer a rate cut of 50 bps to 2.25% but I think the central bank might wanna play it from the safe side to prevent sudden inflation bounce.

Is it time to collect some bank stocks? If you have cash to spare and don't mind to keep it for few years, WHY NOT?

Thats it for today!

Join my telegram group for Stocks Discussion!

Also visit my blog: https://moneytots.blogspot.com/

More articles on Money Thoughts

Discussions

2 people like this. Showing 5 of 5 comments

One of the most useless article I ever saw. You tell us ratio and profitability for what? I can get those from

Investopedia

2020-03-04 07:33

Rate cut is bad for banks

1) When banks offer Fd rate deposits the high interest is fixed for 1 year, 3 years, 5 years or more.

2) Banks already gave out loans with variable interest. So interest rate down banks have to cut and earn less

So while banks fd paid out to customers are locked in banks earning will go down if interest rate drop

SO WHEN INTEREST IS DOWN BANKS WILL SUFFER

BETTER SELL OFF ALL BANK SHARES

2020-03-04 07:39

But today most bank counters up! Maybank new government started the engine. Is not logic as Dow Jones down >780 points. Wait and see time

2020-03-04 22:01

Shares pricing relies on market perception { totally not related or correlated with price to book ratio} without prejudice how often do u find a full fledged accountant doubles up a successful trader. Read the book why a A student works for C student's { then u will understand

2020-03-06 13:33

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE INVESTMENT APPROACH OF CALVIN TAN

2

All Official Update

3

My Trading Adventure 2025

4

Stock Market Enthusiast

Feng Shui Market Outlook for FBM KLCI in the Year of the Wood Snake (2025)

5

Bursa Stock Talk

6

My Trading Adventure 2025

7

My Trading Adventure 2025

8

Readers' Digest MY

Japan’s Telecommunication Boom: Innovation, Growth & the Future

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

boringzack

Educational, good job

2020-03-04 07:32