Rakuten Trade Research Reports

The Research Hive - Media Chinese International Ltd (MEDIAC, 5090)

rakutentrade

Publish date: Tue, 21 Apr 2020, 03:50 PM

rakutentrade

0 2,137

An official blog in I3investor to publish research reports provided by Rakuten Trade research team.

All materials published here are prepared by Rakuten Trade. For latest offers on Rakuten Trade products and news, please refer to: https://www.rakutentrade.my/

To sign up for an account: http://bit.ly/40BNqKI

Rakuten Trade

Hotline: +603 2110 7110 (Account Opening, General enquiry)

Email: customerservice@rakutentrade.my

All materials published here are prepared by Rakuten Trade. For latest offers on Rakuten Trade products and news, please refer to: https://www.rakutentrade.my/

To sign up for an account: http://bit.ly/40BNqKI

Rakuten Trade

Hotline: +603 2110 7110 (Account Opening, General enquiry)

Email: customerservice@rakutentrade.my

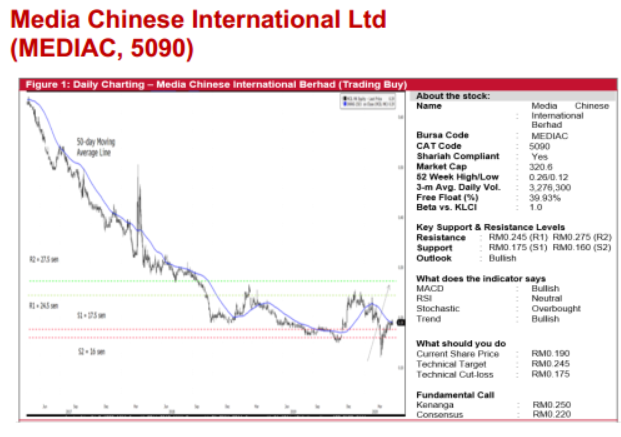

Media Chinese International Ltd (Trading Buy, TP:RM0.245, SL: RM0.175)

• Media Chinese International Ltd (MCIL) is expected to turn around in FY Mar 2020 after posting a reported net loss of RM46.1m in FY19. 9MFY20 net profit came in at RM36.2m.

• The improved performance will be lifted by cost trimming initiatives and tax incentives (for its travel and travel related services). MCIL, which derives roughly half of its revenue from overseas, is also a net beneficiary of a stronger USD versus MYR.

• More interestingly, the Group is currently sitting on net cash of RM265.8m as of end-Dec 2019, which translates to 16 sen per share or 84% of its current share price.

• MCIL is projected to pay net DPS of 1.5 sen, translating to an attractive dividend yield of 7.9% based on its current share price.

• Technically speaking, the stock has been trending south since May 2013, sliding from a peak of RM1.35 to an all-time low of RM0.12 on 17 Mar 2020.

• After bouncing up from the low, the stock is now testing its 50-day moving average line. Riding on the positive momentum, its share price could recover to our first resistance (R1) threshold of 24.5 sen (representing a 29% potential upside). This also coincides with our research team’s fundamentally derived target price (which is based on 0.6x FY21E NTA).

• Beyond which, the next resistance level (R2) is set at 27.5 sen (+45% potential upside).

• On the downside, our support lines are seen at 17.5 sen (R1) and 16.0 sen (R2), translating to downside risks of 8% and 16%, respectively.

Source: Rakuten Research - 21 Apr 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Rakuten Trade Research Reports

Mega Fortris Berhad - Growth Is Signed, Sealed and Delivering…

Created by rakutentrade | Nov 11, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

2

4

bearisking

5

6

save malaysia!

7

HLBank Research Highlights

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....