Rakuten Trade Research Reports

Foreign Equities (HK) - WHARF REAL ESTATE INVESTMENT - BUY With 22.8% Potential Upside.

rakutentrade

Publish date: Mon, 14 Aug 2023, 08:38 AM

rakutentrade

0 1,855

An official blog in I3investor to publish research reports provided by Rakuten Trade research team.

All materials published here are prepared by Rakuten Trade. For latest offers on Rakuten Trade products and news, please refer to: https://www.rakutentrade.my/

To sign up for an account: http://bit.ly/40BNqKI

Rakuten Trade

Hotline: +603 2110 7110 (Account Opening, General enquiry)

Email: customerservice@rakutentrade.my

All materials published here are prepared by Rakuten Trade. For latest offers on Rakuten Trade products and news, please refer to: https://www.rakutentrade.my/

To sign up for an account: http://bit.ly/40BNqKI

Rakuten Trade

Hotline: +603 2110 7110 (Account Opening, General enquiry)

Email: customerservice@rakutentrade.my

TECHNICAL ANALYSIS

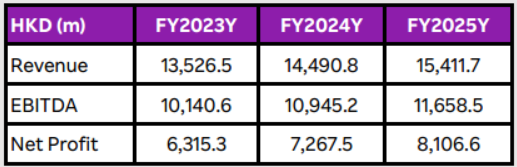

Wharf experienced a 3-day consecutive sell-down last week despite a turnaround in earnings YoY for 1HFY23. However, it missed market estimates due to modest Q2 recovery which was affected by economic uncertainties. All its MA lines are trading below its current share price hence the potential opportunity for accumulation during weakness, supported by its strong fundamentals.

Fundamentals

Net profit is expected to grow at a CAGR of 13% for the next 3 years with strong net margins ranging from 46%-50%.

Source: Rakuten Research - 14 Aug 2023

To sign up for an account: http://bit.ly/40BNqKI

[Youtube Tutorial] Account Opening & Enable Foreign Equity: http://bit.ly/3I5Jzxo

More articles on Rakuten Trade Research Reports

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Open a Moomoo Account Today and Win an Apple iPad Air*!

Apps

Top Articles

1

2

博傻理论

3

Good Articles to Share

4

THE INVESTMENT APPROACH OF CALVIN TAN

MKHOP (5139) What Is Its Current Forward P/E and Intrinsic Value, Calvin Tan

6

7

KLSE Traders Update and Ideas

8

M+ Online Research Articles

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....