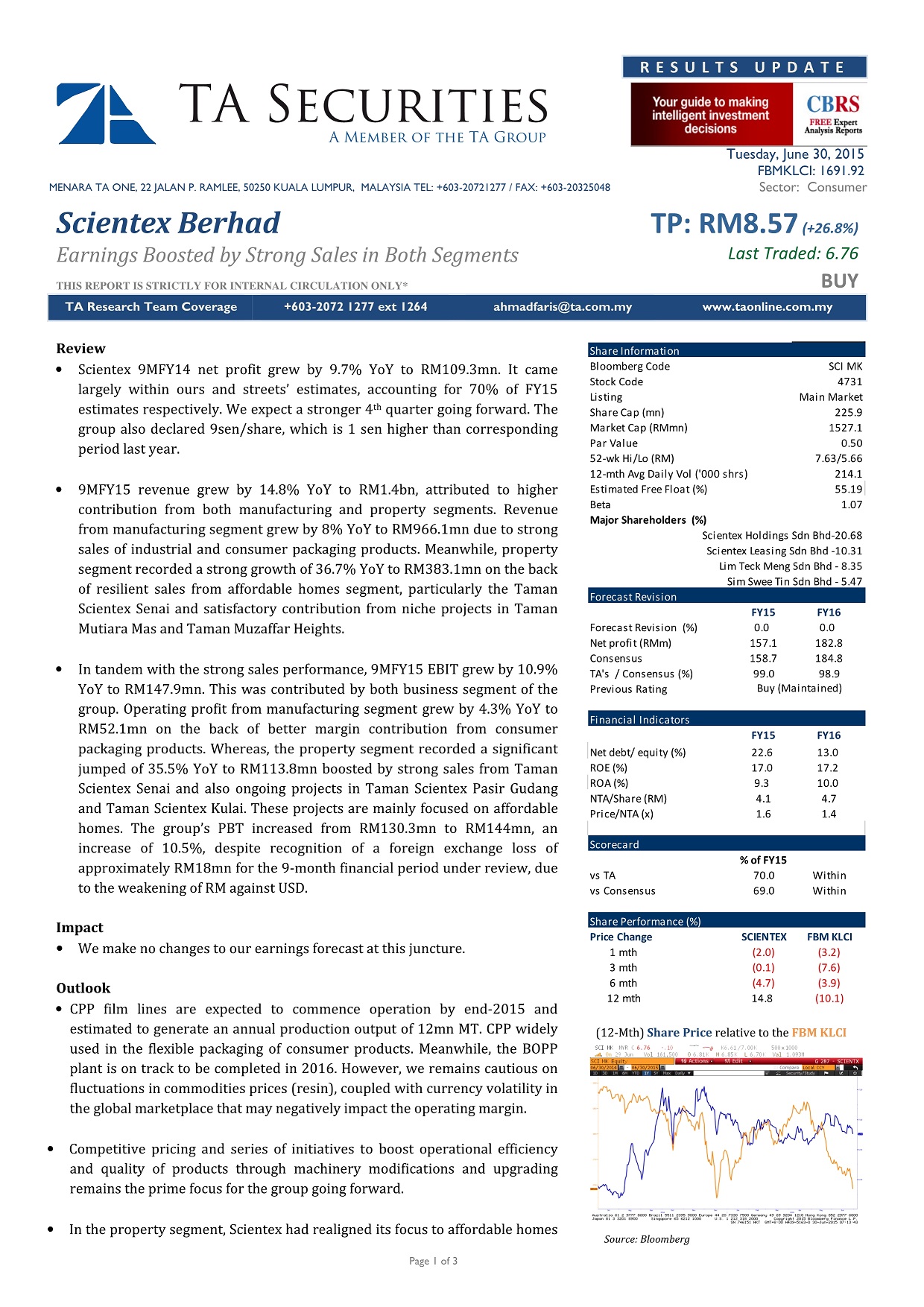

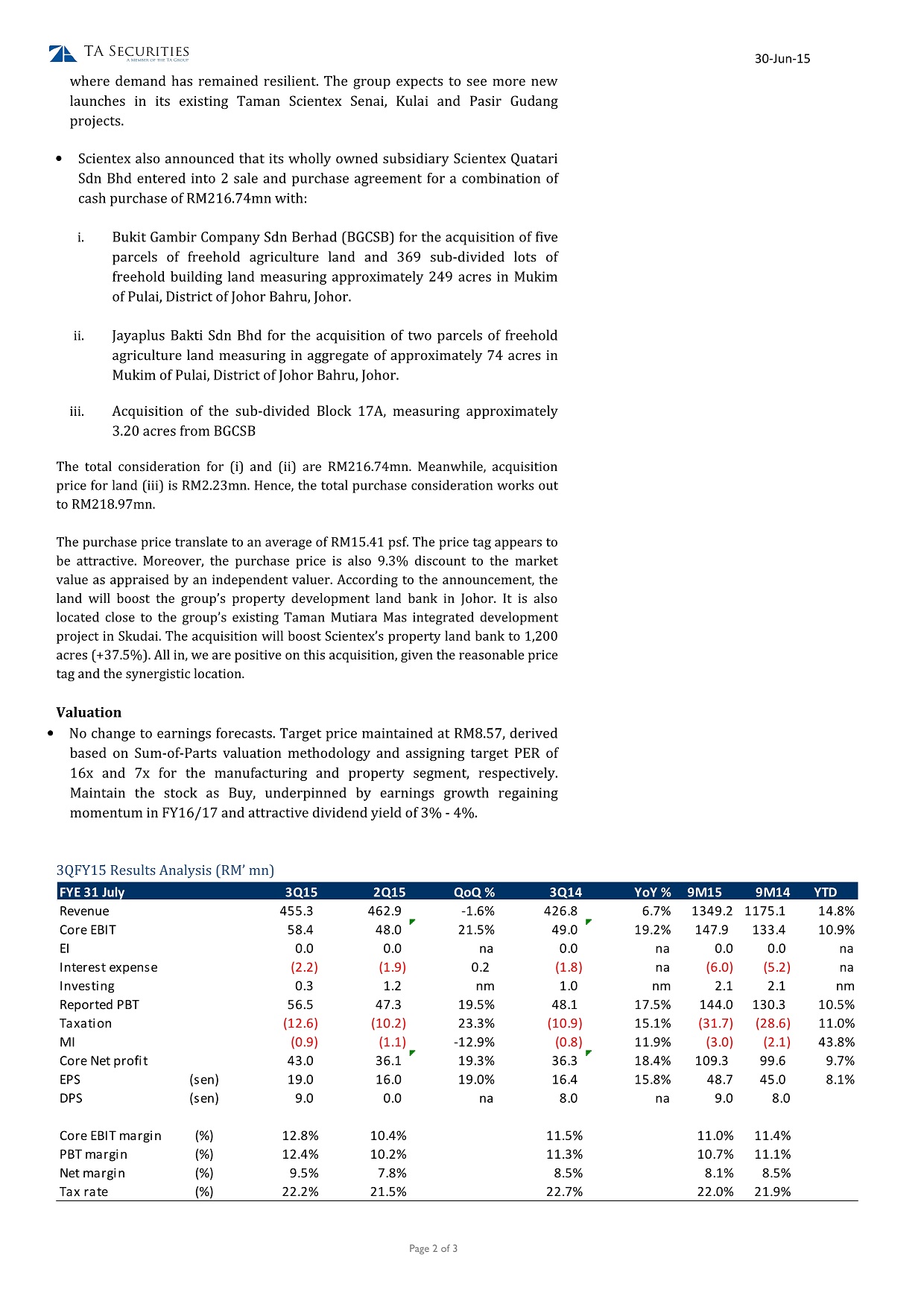

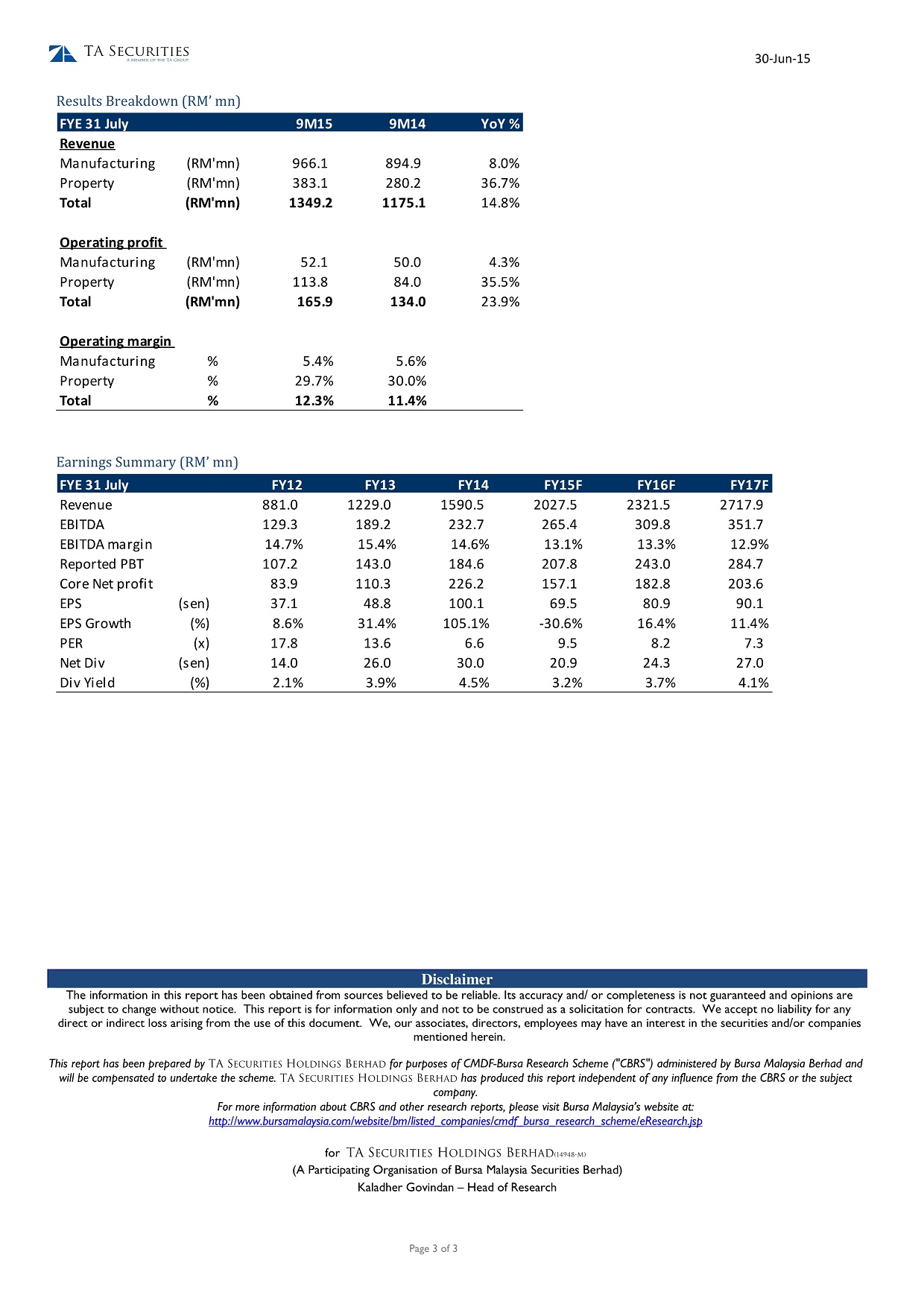

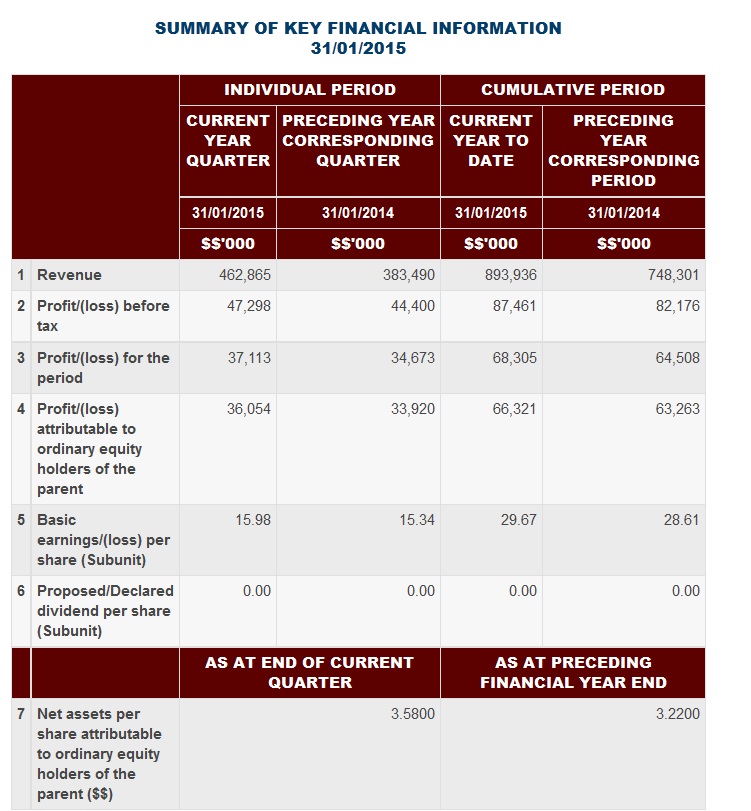

以下纯粹个人投资收集与记录,且本人非专业分析员,买卖亏盈自负。 The articles here solely the collection or opinion of the author and do not represent professional advice in investment

Lim: More than 70% of our business comes from exports.

SHAH ALAM: Scientex Bhd ( Valuation: 1.50, Fundamental: 1.70), which saw its net profit doubling to RM60.85 million in its first quarter ended Oct 31, 2015 (1QFY16) from the previous year, expects its FY16 performance to normalise.

This is because, according to managing director Lim Peng Jin, Scientex has reduced its US-dollar-denominated loans and adopted a new hedging position.

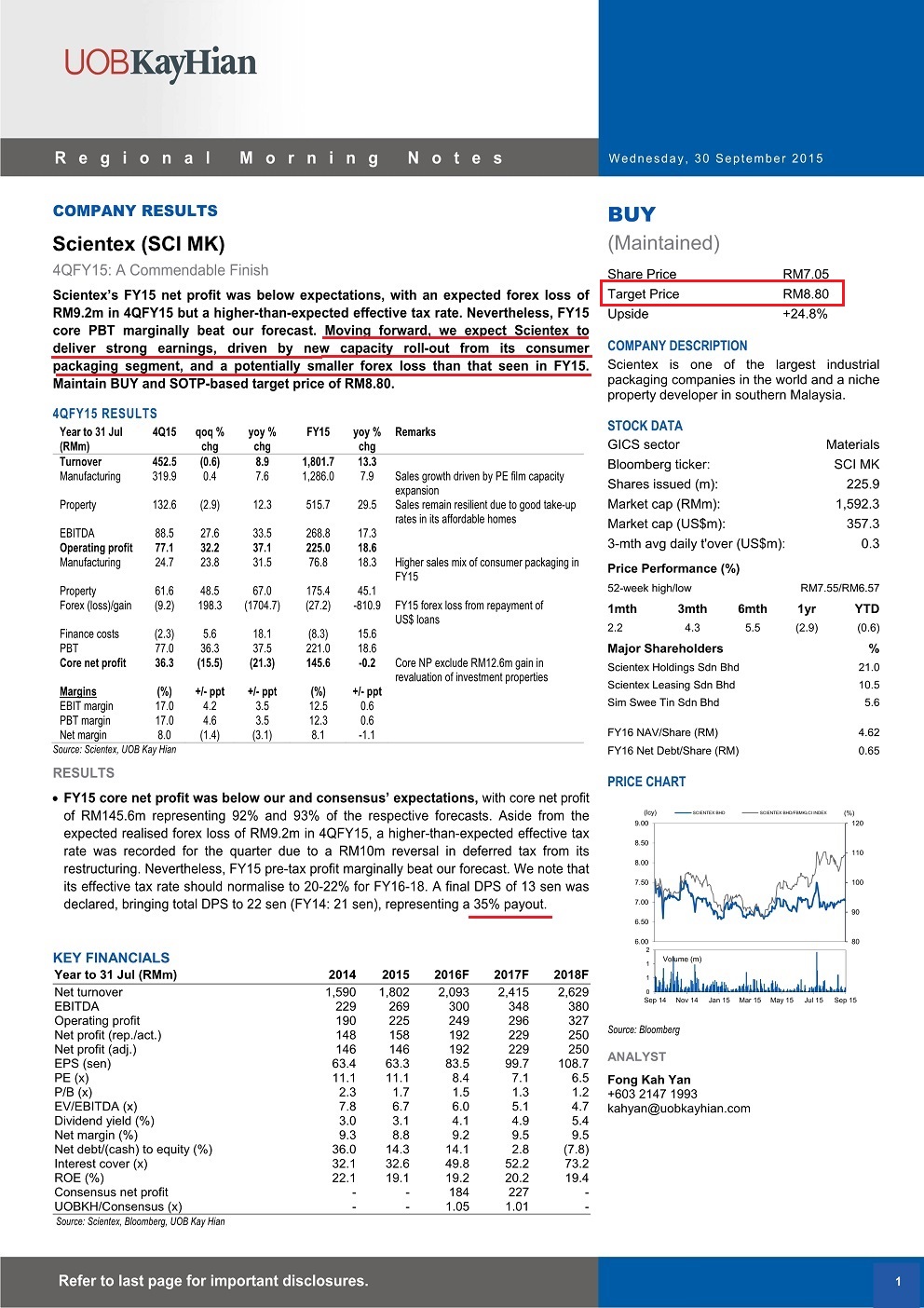

Scientex’s FY15 core net profit was flat at RM149.2 million, according to Kenanga Research in its Sept 30 note. Although property earnings before interest and tax (Ebit) improved 45% to RM175.4 million and manufacturing Ebit rose 12% to RM76.8 million, its overall earnings were dragged down by RM27.2 million of foreign exchange loss realised, as it pared down its US-dollar borrowings by 80% to RM55.9 million.

Scientex also saw higher effective taxation (from 19% to 27%) due to the timing of its deferred tax recognition, which should normalise in the next financial year, Kenanga Research had noted.

Judging by its first-quarter result, and with the absence of tax adjustment, the group’s full-year performance would be encouraging, said Lim.

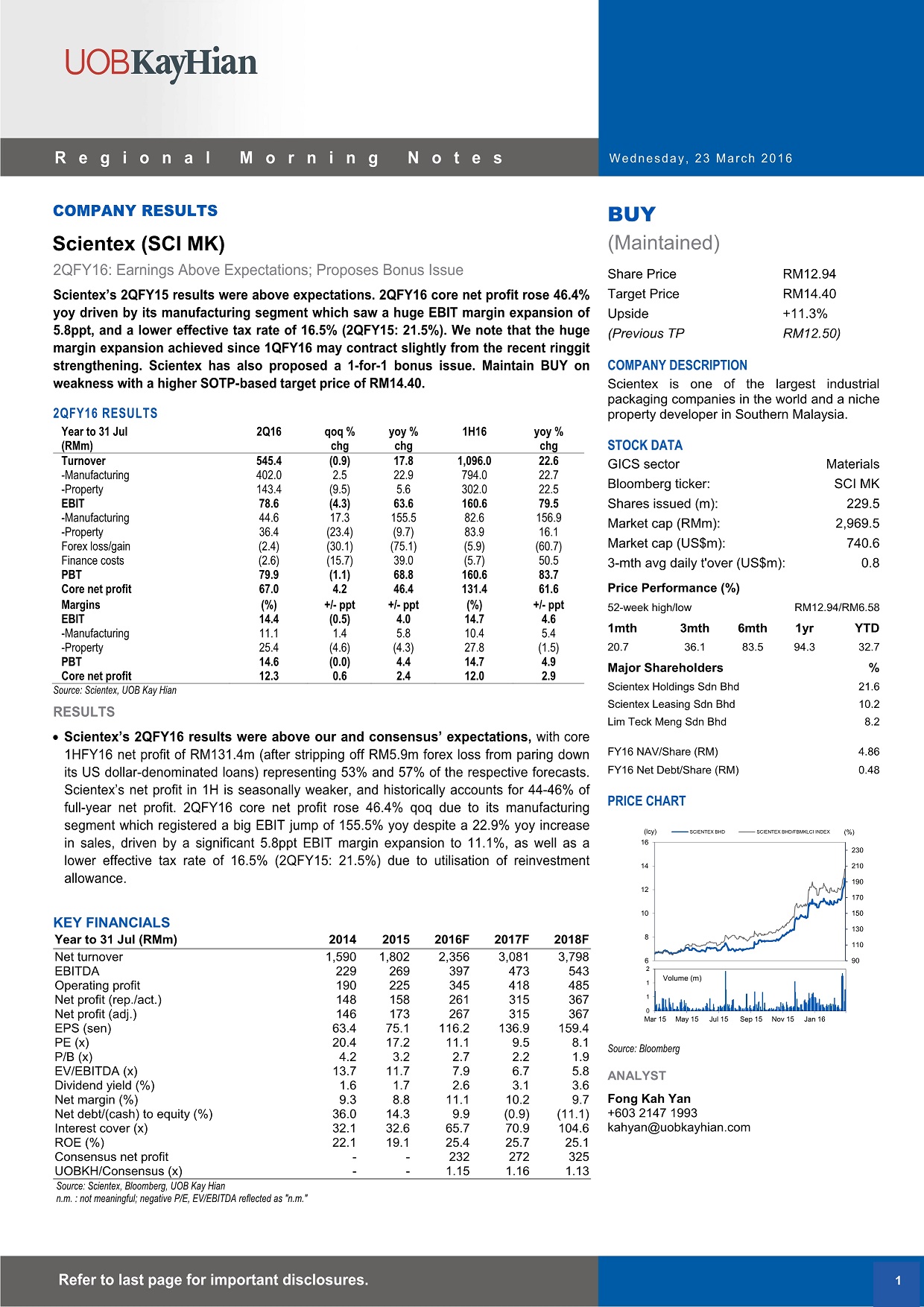

The company doubled its net profit to RM60.85 million in 1QFY16 from RM30.27 million a year ago, as revenue grew 27.7% to RM550.6 million from RM431.1 million, driven by higher packaging product manufacturing revenue and property development income.

“We are benefiting from the strengthening of the US dollar and low oil prices, as more than 70% of our business comes from exports,” Lim told reporters after the group’s AGM yesterday.

To maintain growth, the packaging manufacturer and property developer is still actively looking to acquiring new packaging assets and land banks.

“Having said that, new expansions will have to wait until the second half of next year. Our focus in the first half is to execute the plans we put in place in FY15,” Lim said. As such, Scientex is not talking to any packaging party yet.

“[As for the land bank] we don’t limit ourselves to only Johor, but we don’t have anything concrete yet,” he added.

He also said as long as Scientex can maintain its current growth, 30% of the group’s net profit will be allocated for dividends, with the remainder for business expansion.

“This year (FY16), we will see better results and operating cash flow,” he added. The company’s cash flow in FY15 stood at RM200 million.

The company has set aside RM460 million for capital expenditure for FY16; RM200 million is for property expansion, with the remainder for the packaging business.

“Three new packaging plants will start operations by the middle of next year. Our current capacity is about 5,000 tonnes per month, which should rise to 12,000 tonnes,” said Lim.

“Thirty per cent of the group’s new plant capacity is for the Japanese market. Japan and Southeast Asia will remain our focus in terms of consumer packaging,” Lim said.

On property development, the total gross development value of the group’s projects in hand is RM1.3 billion.

Lim said Scientex’s management wants to build affordable homes priced below RM500,000 and landed properties, which have not been affected by the economic downturn.

As at Oct 31, Scientex’s unbilled sales stood at RM632.2 million, which it will be recognising up till 2018.

Scientex’s stock ended 55 sen or 6.4% higher at RM9.15, valuing it at RM1.94 billion, and was the fourth top gainer across the bourse yesterday.

The job of every company is to make money, and there is no money like cash. Cash flow from operations (CFFO) is the purest inflow and outflow of cash in relation to actually doing business. From a company health perspective it is one of the most important measures.

Companies require capital expenses in purchasing and upgrading plant and equipment for growth. The money is not gone. It is carried on the balance sheet as an asset. The end goal is for the company to generate a return on the asset. Free cash flow (FCF) is what is left after those expenses.

Free cash flow is like the end all goal of companies. The point is to do so well that you make so much money that even after all the checks written to expand the business you still have a lot of cash. Cash is pretty much the most important thing, and FCF is the most flexible kind of cash there is. With this internally generated FCF, a company can pay out dividend consistently, buy back its shares when they are selling cheap, pare down loans, or invest in other profitable ventures, all done without assuming more debts which makes the business more risky in times of the down turn in economy, or asking more money from shareholders, or issuing more shares to private investors, often at a discount, and hence diluting the earnings per share of the existing shareholders.

There are some companies doing so well that even after heavy expansion they have a lot of cash left over. Scientex Berhad is one of them, and it has been using this FCF to do most of the above.

Scientex Berhad

Scientex Berhad is engaged in two operating segments: property segment, which is in the business of constructing and developing residential and commercial properties, and manufacturing segment, which is mainly in the business of manufacturing various packaging products and manufacturing materials for automotive interior. Included in this segment is also the marketing and sales of laminating polyurethane adhesives. The packaging business unit manufactures various packaging products, which caters for packaging for logistics purposes, general purpose packaging and packaging for bulk handling. The polymer business unit manufactures polyvinyl chloride (PVC) leather cloth, PVC/polypropylene (PP) and PVC/polyethylene (PE) foam and thermoplastic olefin/PP foam sheets for automotive instrument panels, door trims and headlining for car manufacturers in the Asia Pacific region.

I have written a couple of investment thesis on Scientex since 14 months ago when its share price was at RM5.74 apiece as shown in the link below.

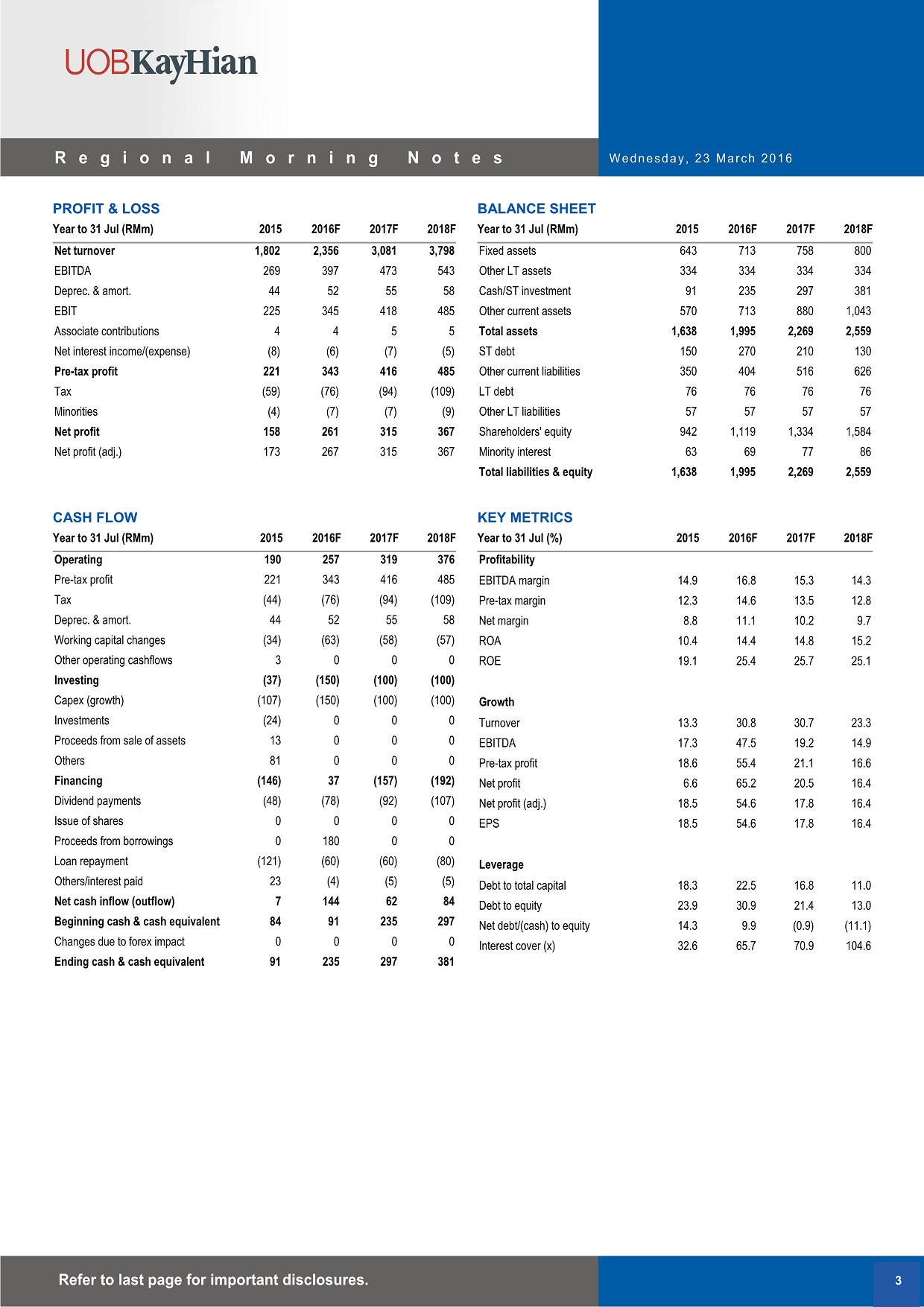

Scientex just announced unaudited earnings results for the year ended July 31, 2015. Revenue for the year improved by 13.3% to RM1.8b and operating income jumped by 18.6% to RM225m. Earnings per share, EPS was 70 sen, against 67 sen a year ago. Net cash from operating activities was RM190m, against RM154m a year ago.

At the close of RM7.40 today, the PE ratio is 10.5; not that cheap compared to its historical PE ratio, and an enterprise value of 8.7 times its operating income. However, it is slowly transforming itself to a big regional PVC/polypropylene and PVC/polyethylene business. The attractiveness of investing in Scientex actually lies in its cash flow.

Cash flows of Scientex

For the latest annual financial results ended July 31st 2015, net income is RM162m while its cash flows from operations (CFFO) is 17% more at RM190m. This signifies the good quality of its earnings. It spent a considerable amount of money in capital expenses of RM116m, and yet there is still abundant free cash flow, FCF of RM74m left. This is 4.1% of revenue and 6.3% of invested capital (IC), in hard cash. It is from this FCF that RM47m was paid out as dividends, and partly paid down its debts.

Figure 1 below shows that the growth of net profit of Scientex at a compounded annual growth rate, CAGR of 30% for the last 12 years.

There is not a single year when it made losses. CFFO grows at tandem and it has been consistently above the CFFO, showing a high quality earnings.

Scientex does use considerable amount of debt of a total of RM254m. However this debt is only 0.24 times its total equity, and its CFFO covers a whopping 23 times its interest payment. Scientex has done a good job utilizing other people’s money to yield a high return on equity of 19%.

Not only CFFO is positive every year, its FCF is also positive every year without fail, except for a single year in 2004 when it spent a relative high capital expenses as shown in Table 1 below.

Table 1: Cash flows of Scientex

Over the last 13 years, it has produced a total FCF of RM689m which it used to invest in profitable investments and paying dividends to shareholders, invest in profitable comanies, and not from your own money (right issues), continued borrowing from banks, or by giving a piece of the business from other private investors (private placement).

Conclusions

Scientex has high revenue and profit growth for the last 12 years. Despite the very high growth, It still have positive and reasonable good FCF every year. It even earns more cash than its accounting profit every year. After spending huge amount of capital expenses and acquiring other companies in the same business, and as a result, it earns more profit and hard cash.

Scientex appears to be the kind of company investors should look out for investing for the long term; A regional and world market leader, high return on capitals, a cash cow, but trading at reasonable price, or may be even cheap price.

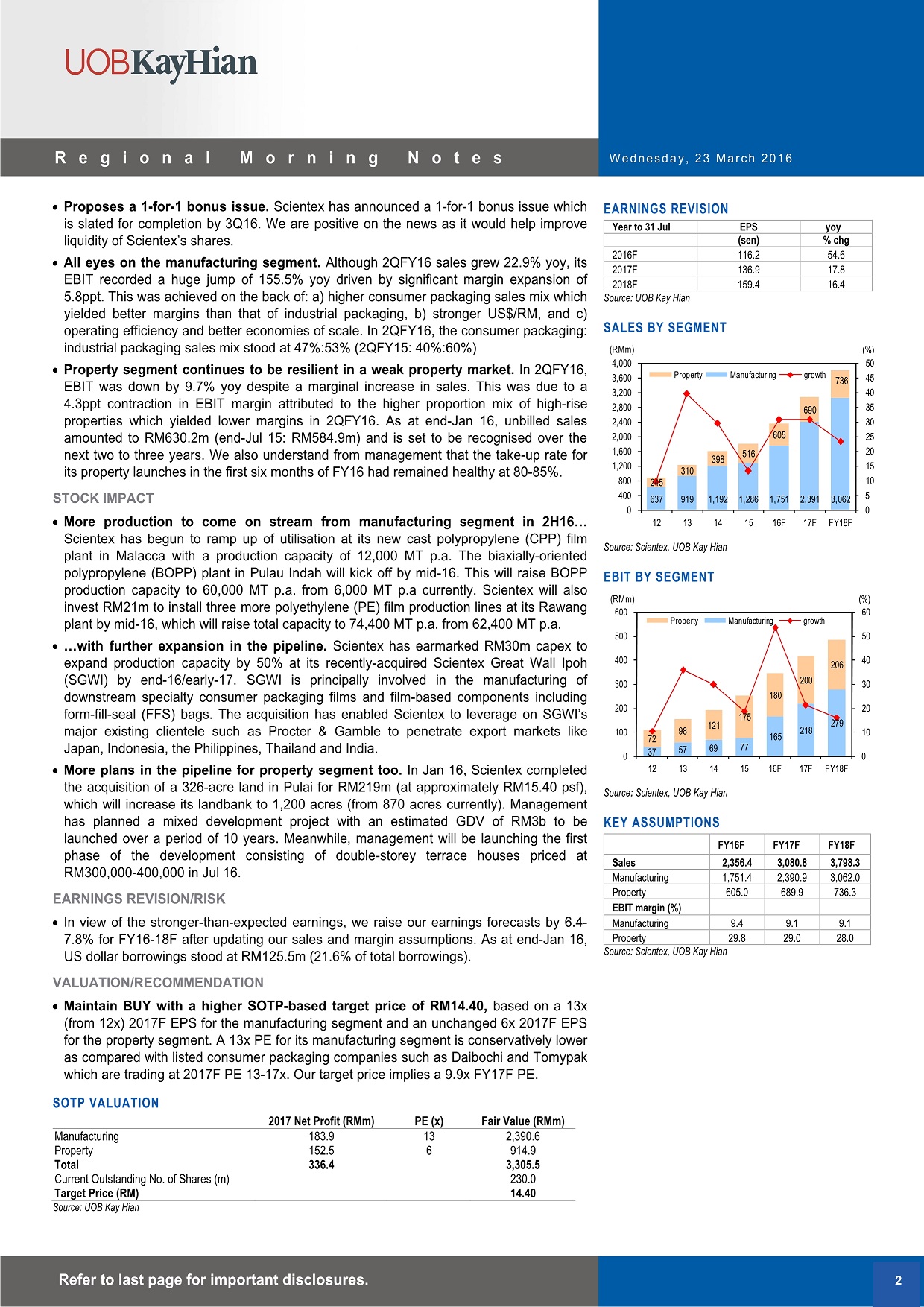

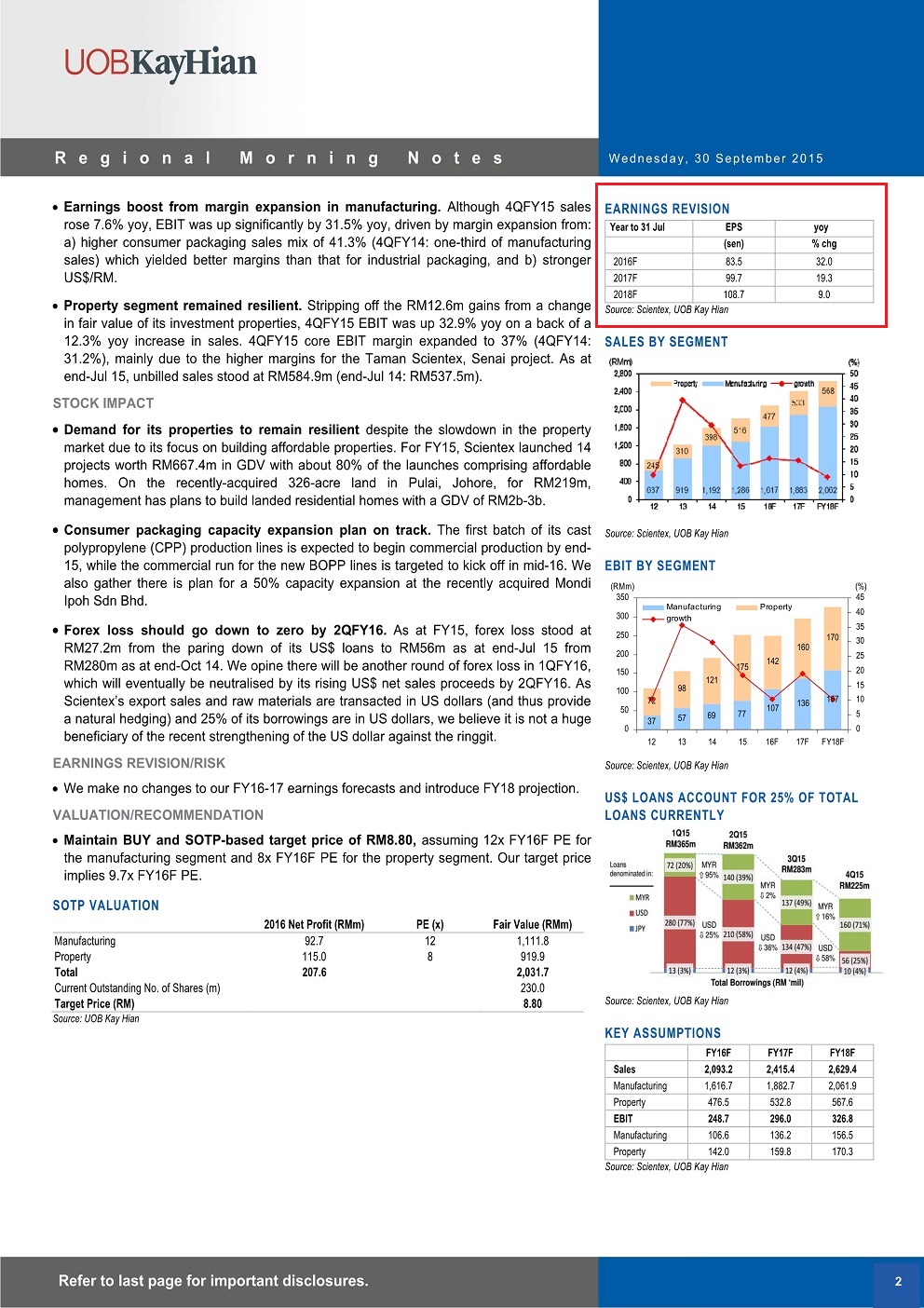

Scientex has proposed to acquire a consumer packaging player, MISB,from Mondi for MYR58m. Maintain BUY, with a higher SOP-based TP ofMYR8.80 (20.5% upside) while we roll over our valuation period to 2016 from FY16 (Jul). We are neutral on the minimally earnings-accretive acquisition, which could prove to be potentially cheap. We also retainour earnings forecast pending more details due in September.

Proposed acquisition. Scientex has proposed to acquire a 100% equity stake in Mondi Ipoh SB (MISB) from Mondi Consumer Packaging International (Mondi). The purchase consideration is MYR58m, funded by cash from internally-generated funds. MISB is slated to boost Scientex’s consumer packaging production capacity by about 30% to 76,800 tonnes from 60,000 tonnes. The acquisition is targeted to be completed by 11 Aug 2015. We believe funding should not be an issue as: i) net of the acquisition as of 3Q15, Scientex would have a remainingMYR5m cash position with a net gearing level of 0.33x, and ii) it also has a healthy FY15F net cash generation of MYR56m.

Neutral impact, potentially cheap. An acquisition P/E of 20.4x based on FY14 earnings appears to be on the high side, if we take into accountthe fact that its peers are trading at 18.6x (Scientex itself is trading at 10.5x). Meanwhile, MISB’s FY14 earnings of MYR2.8m would have aminimal accretive impact of ~2% to Scientex’s 2015F earnings. On the operational front, MISB’s FY14 net profit margins are also at a razor-thin2%. However, these factors combined may be moot, if synergistic benefits are realised. Based on our valuation sensitivity analysis, improving margins to 5% from its current ~2% could see the acquisition valued at a forward P/E of 8.2x.

Maintain BUY with a higher TP. We make no changes to our earnings forecasts pending more details from management, which are due in September at its FY15 analyst briefing. We maintain our BUYrecommendation, and take this opportunity to roll over our valuation period to 2016 from FY16, with a revised SOP-based TP of MYR8.80 (from MYR7.90) at an implied P/E of 9.5x 2016.

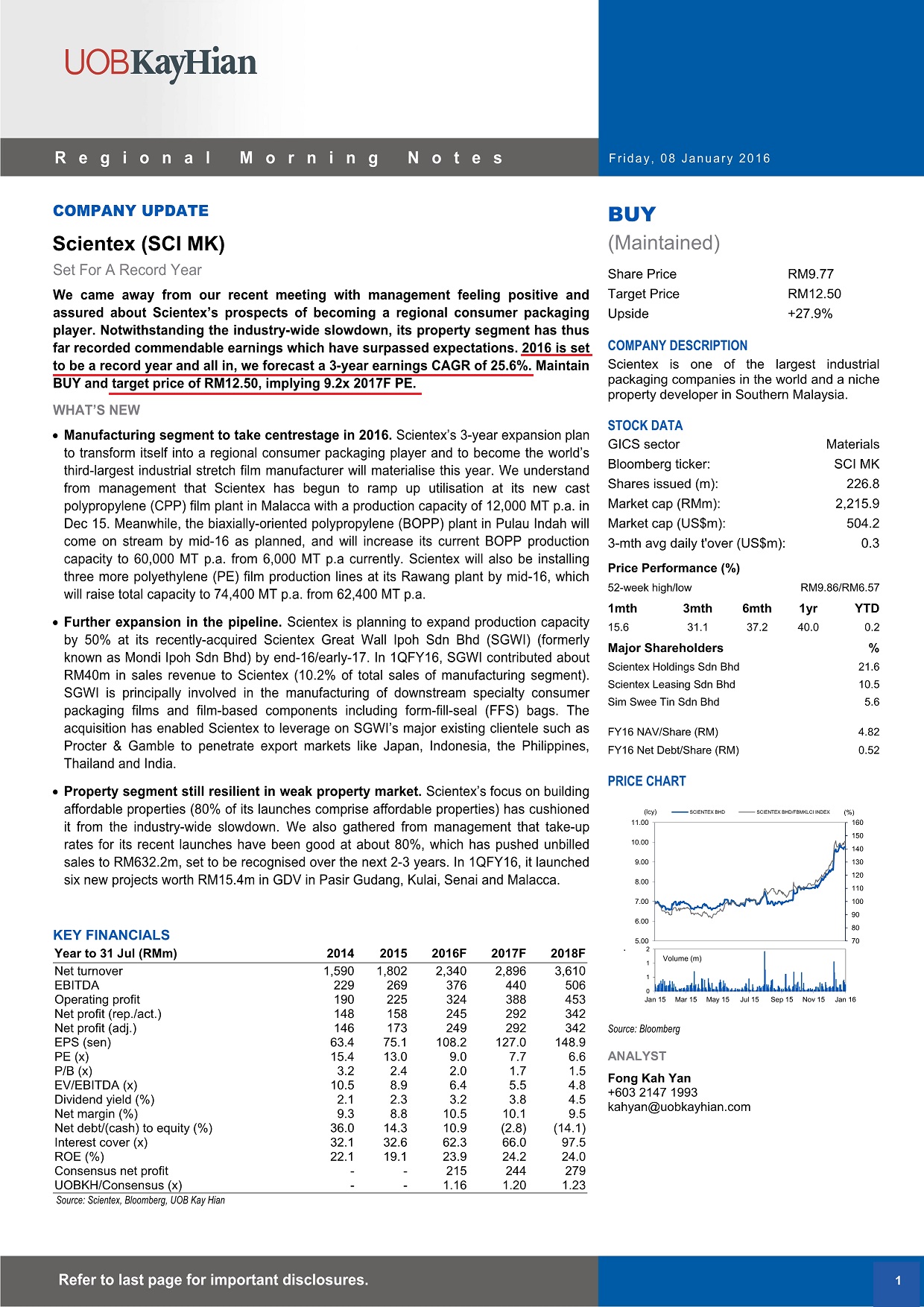

Scientex’s 1QFY15 (Jul) core earnings of MYR35.5m met our expectations. Maintain BUY, with our SOP-based TP unchanged at MYR8.64 (26.3% upside). We continue to like the stock for: i) its long-term earnings prospects leveraging on its expansion strategy to quadruple its consumer packaging capacity by 2017, ii) relatively sturdy balance sheet, and iii) committed management team.

Largely in line. 1QFY15 revenue closed at MYR431.1m (+18.2% YoY), driven by both its packaging arm (+10.8% YoY) as well as its property development segment (+46.5% YoY). EBIT, meanwhile, grew by a smaller 15.5% YoY to MYR44.9m due to: i) higher depreciation in tandem with its capacity expansion, and ii) revised pricing under its packaging arm to increase market penetration to fully utilise its new capacity. All in, 1QFY15 core earnings of MYR35.5m came in at 19.7% and 19.9% of consensus and our full-year estimates respectively. We deem this in line with our expectations, as 2H is seasonally stronger.

Sturdy balance sheet. Recall that Scientex has proposed to invest over MYR240m in capex over the next two years to quadruple production capacity under its consumer packaging segment to 120,000 tonnes come 2017 from 54,000 tonnes currently. We continue to believe funding should not be an issue, given: i) its relatively manageable net gearing level of 0.34x currently, ii) operating cash flow of over MYR200m per year, and iii) an additional MYR40m cash inflow from FutChem’s subscription of 5% stake in its consumer packaging arm.

Forecasts and risks. With the results coming largely in line, we make no changes to our FY15F-17F forecasts. Key risks include a potential slowdown in property sales amidst rising costs of living and potential fluctuations in the prices of resin, which is its core production input.

Maintain BUY. Scientex’s share price has retraced by over 11%, in tandem with the recent market selldown. We see this as an appealing opportunity for investors to accumulate, as we continue to like the stock for: i) its long-term earnings prospects leveraging on its expansion strategy to quadruple its consumer packaging capacity by 2017, ii) relatively sturdy balance sheet, and iii) committed management team. Maintain BUY with our SOP-based TP unchanged at MYR8.64.

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....