Airasia - Oppurtunity to Accumulate before it really Fly

Airasia - Oppurtunity to Accumulate before it really Fly

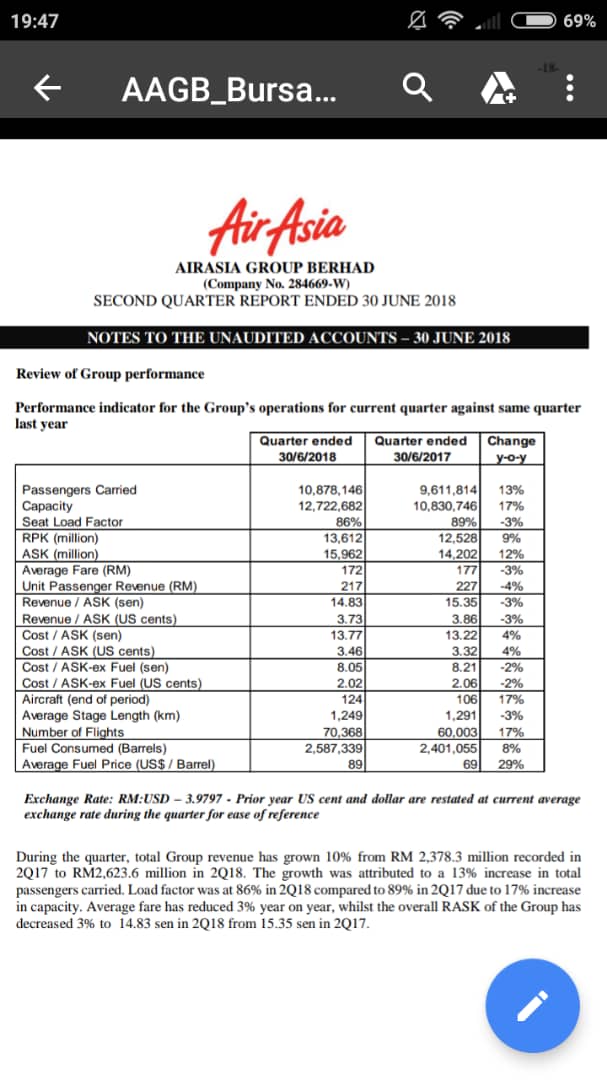

Quick Analysis on AirAsia:

2Q18 Qtr results represent a good efficient on Tony`s management team in deliver their earning result despite fuel jet price hit $89. This 2Q18 result show it actual core biz earning, EPS 10.8sen. impressive is even oil price $89, cost ASK is 13.77sen vs 2Q17 oil price $69 cost ASK 13.22sen drop (-4%) only with $20 oil price difference (-29% worse). This show Airasia leadership are strong in lean cost operation and still manage to deliver good satisfaction earning result despite high oil price fluctuation.

Relook on its core business QoQ comparison, 1Q18 cost ASK 13.55sen with oil price $83 against 2Q18 cost ASK 13.77sen with oil price $89 (-1.6% worse). In general, discount any unforseen condition, by right airline worst Qtr earning result fall in 2nd Qtr every year due to lack of traveller travel. Moving next Qtr as expected, more travellers will start to fly and go holiday by early 4Q18 season (Oct - Dec period), thus expected 4Q18 earning result will be better as predicted by sector analysts.

Share Price Analysis:

In term of share price calculation, assume worst 2Q18 EPS remain across all Qtrs, then 10.8 x 4 = 43.2sen ; airline biz sector fall within PE 8 to 10, worst case share price valuation should be RM 3.45 to RM 4.32 range. Yet, not included upcoming 4Q18 AAC selloff announcement in Oct/Nov, payout by Dec 2018, expect to pay 70 to 80sen payout + additional Expedia biz selloff payable divident of 7sen by 4Q18. That's represent a total of 77 to 87 sen /share special dividend payout by 4Q18.

High potential for Airasia's share price to appreciate and go higher is there, but in slower mode due to market noise fluctuation. If investor really reassess and revisit on its short to near term period of next 1 to 2 mths, the price will go up quietly unnotice to RM4.00+ range till 3Q18 Qtr result. Airasia will raise under investor low radar at non-significant volume vs price trade appreciation to avoid big mass foreign fund big stocks accumulation. With current low undervalued share price, it is an attractive stock selection among big investor and it will raise quickly once jet fuel oil price and RM currency get stablize.

Barring any unforeseen circumstances, I believe Airasia will remains positive for overall results in 2018, capable to hit beyond Rm4.50 level at conservative mode if all goes smoothly per plan.

Assessing the Market Outlook by Analyst:

"AirAsia did surprisingly well, beating our and market forecasts," said Crucial Perspective CEO Corinne Png, who has covered Asian transport equities for over 15 years at J.P. Morgan, Citigroup and HSBC.

The research firm said AirAsia's stock has been oversold, and presents a good buying opportunity when oil prices and the Ringgit Malaysia stabilize — even though it has limited fuel hedging and most of its overseas joint venture carriers were loss-making

Risk associated to Airasia that affect its earning results:

1) Higher fuel jet price

2) Local Currency fluctuation

3) Geo-political market sentiment - US China trade war

Latest Bursa announcement on AAC sell off- dated 3rd Sept 2018:

The Company wishes to announce the completion of the transfer of an additional number of aircraft pursuant to the Incline B SPA and the FLY SPA on 30 August 2018. The total number of aircraft involved under the abovementioned transfer is 15 aircraft and AAGB has received USD201.5 million in gross proceeds in the form of USD151.5 million as cash consideration and 3,333,333 FLY Equity issued at USD15.00 per FLY Depository Share to AAGB in accordance with the FLY Subscription Agreement.

To date, the cumulative number of aircraft transferred is 54 aircraft and AAGB has already received gross proceeds totalling USD703.1 million.

AAGB is still on track to complete the disposal of the remaining 30 aircraft and 14 aircraft engines under the Incline B SPA and FLY SPA as planned.

http://www.bursamalaysia.com/market/listed-companies/company-announcements/5903361

Happy Invest!

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Discussions

3 people like this. Showing 3 of 3 comments

Analyst prediction from CIMB, not from AAGB...

" Separately, AAGB recently completed the sale of the residual 25% stake in AAE Travel to Expedia on 14 Aug 2018 for US$60m, or 7 sen/share, which we expect will be paid out as special dividends before end-2018F"

"The sale of 84 planes to BBAM is partly complete, with 39 aircraft transferred up to 8 Aug 2018, and another 45 transfers to be completed by Nov 2018F, in AAGB’s estimate. We estimate that special dividends of up to 75 sen may be declared. According to AAGB’s verbal guidance during the results conference call, the special dividends related to the BBAM transaction may be declared during the release of the 3Q18F results in late-Nov, and be paid in 4Q18F or 1Q19F"

2018-09-03 15:32

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-17 16:20:00

MACD/RSI

5 Mins

SELL

2024-07-17 16:00:00

EMA 5

10 Mins

SELL

2024-07-17 16:00:00

ADX

10 Mins

SELL

2024-07-17 16:00:00

TURTLE SYSTEM 20

10 Mins

SELL

2024-07-17 16:00:00

TURTLE SYSTEM 55

10 Mins

SELL

Apps

Top Articles

1

南洋行家论股

2

BreakingOut

3

Koon Yew Yin's Blog

4

Bursa Stock Musings - Thoughts & Ideas

PGF Capital - insti shareholding up from 5% to 14%! (part 1)

5

The Alpha Trader

6

南洋行家论股

7

RHB Investment Research Reports

8

How to become a resilient trader

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

sean_limkh

Thanks for the analysis!

2018-09-03 14:05