AmInvest Research Reports

Stock on Radar - Homeritz Corporation

AmInvest

Publish date: Thu, 02 May 2024, 10:34 AM

AmInvest

0 9,531

An official blog in I3investor to publish research reports provided by AmInvest research team.

All materials published here are prepared by AmInvest. For latest offers on AmInvest trading products and news, please refer to: https://www.aminvest.com/eng/Pages/home.aspx

Tel: +603 2036 1800 / +603 2032 2888

Fax: +603 2031 5210

Email: enquiries@aminvest.com

Office Hours

Monday to Thursday: 8:45am – 5:45pm

Friday: 8:45am – 5:00pm

(GMT +08:00 Malaysia)

All materials published here are prepared by AmInvest. For latest offers on AmInvest trading products and news, please refer to: https://www.aminvest.com/eng/Pages/home.aspx

Tel: +603 2036 1800 / +603 2032 2888

Fax: +603 2031 5210

Email: enquiries@aminvest.com

Office Hours

Monday to Thursday: 8:45am – 5:45pm

Friday: 8:45am – 5:00pm

(GMT +08:00 Malaysia)

Company Background. Homeritz Corporation (Homeritz) is a leading manufacturer of upholstered home furniture in Malaysia. The group operates primarily as an integrated original design manufacturer (ODM) and original equipment manufacturer (OEM), producing a complete range of upholstered home furniture products. Its main activities include the design, manufacturing and sale of upholstered home furniture, with its customers mainly consisting of overseas wholesalers and retailers. Currently, the group exports its products to more than 40 countries worldwide, spanning Europe, Australasia, North & South America, Asia and Africa.

Prospects. (i) Strengthen research & development to innovate and improve existing designs while developing new, innovative products, (ii) Invest in upgrading equipment and machinery to enhance efficiency, productivity and product quality, (iii) Diligently seek and test new raw materials to facilitate the production of high-quality products at competitive costs, (iv) Continuously diversify and introduce new products to meet evolving client needs and expand market reach, (v) Adopt aggressive marketing strategies and collaborate closely with clients to secure larger market segments, and (vi) Enhance production efficiency to increase competitiveness in pricing and effectively meet market demand.

Financial Performance. In 1HFY24, Homeritz posted higher revenue of RM111.3mil (+41.4% YoY) with a PAT of RM18.3mil (+54% YoY). This was mainly attributed to the increase in volume sold, greater economies of scale, quicker time-to-market, effective cost management and favorable foreign currency exchange.

Valuation. Homeritz is trading at an attractive FY24F P/E of 8.7x, versus Bursa Consumer Index’s 5-year forward average of 17.7x. As a comparison, Spring Art Holdings and Wegmans Holdings, both also involved in the furniture sector, trade at much higher trailing P/Es of 17.8x and 15x respectively.

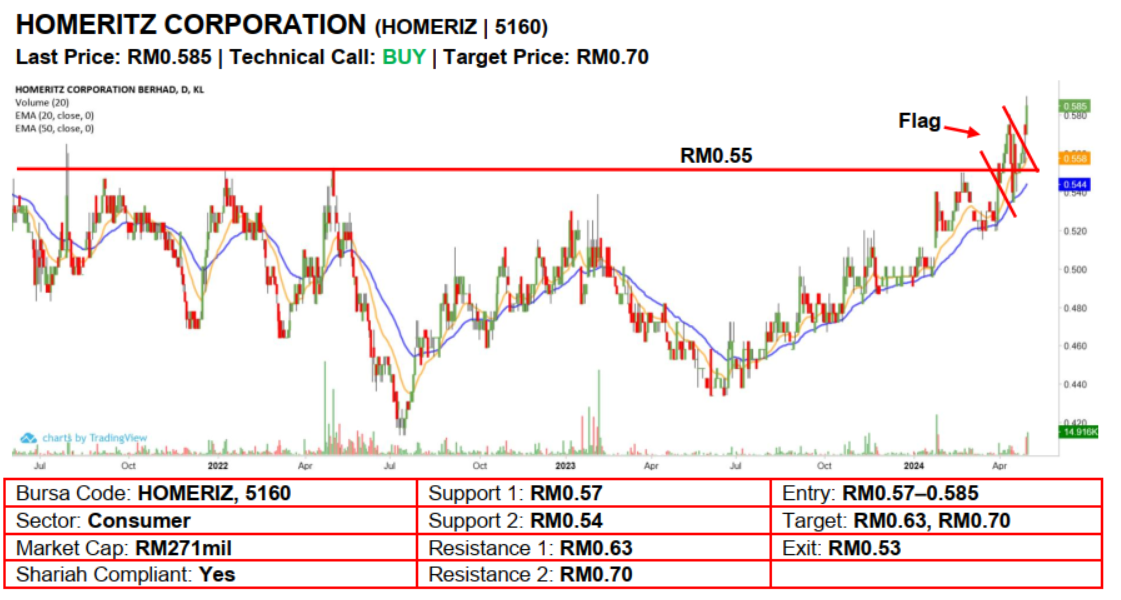

Technical Analysis. We expect further upside for Homeritz after it surged to a new 3-year high with a long white candle on Tuesday. The stock’s move above the RM0.55 resistance coupled with rising EMAs indicate that the near term upward momentum may persist. A bullish bias may emerge above the RM0.57 level with stop-loss set at RM0.53, below the 50-day EMA. Towards the upside, nearterm resistance level is seen at RM0.63, followed by RM0.70.

Source: AmInvest Research - 2 May 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on AmInvest Research Reports

KEYFIELD INTERNATIONAL - Prospects remain intact post-vessel visit

Created by AmInvest | Jan 22, 2025

UOA REAL Estate Investment Trust - Overall occupancy rate of assets improved in 4QFY24

Created by AmInvest | Jan 22, 2025

SUNWAY REIT - Marginal accretive to distributional income from the

Created by AmInvest | Jan 22, 2025

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-22 11:30:00

OBV

30 Mins

BUY

2025-01-22 11:30:00

TURTLE SYSTEM 55

30 Mins

BUY

2025-01-22 10:00:00

EMA 5

Hourly

BUY

2025-01-22 10:00:00

TURTLE SYSTEM 20

Hourly

BUY

2025-01-22 09:50:00

ADX

10 Mins

BUY

Apps

Top Articles

1

Mercury Securities Research

2

HLBank Research Highlights

3

PublicInvest Research

4

黄金十年-延续篇

5

RHB Investment Research Reports

6

7

MQ Market Updates

8

RHB Investment Research Reports

Market Strategy - Data Centre-Artificial Intelligence Party Pooper

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....