Alpha Stock Hunt

Alpha Stock Hunt (19 - 23 Oct 2020)

ripmorepoints

Publish date: Mon, 19 Oct 2020, 11:53 AM

ripmorepoints

0 4

Welcome to my blog. This is where I share my two cents on the potential alpha / gem stocks waiting to be unfold by smart investors.

The methodology combines the analysis of stocks momentum as part of the Technical Analysis and peers comparison as part of the Fundamental Analysis

The methodology combines the analysis of stocks momentum as part of the Technical Analysis and peers comparison as part of the Fundamental Analysis

Hey, it’s time for the hunt of alpha stocks again! KLCI almost erased its gain from the previous week as the bourse closed slightly above 1500 psychological level. Let’s hope it will remain supported above 1500.

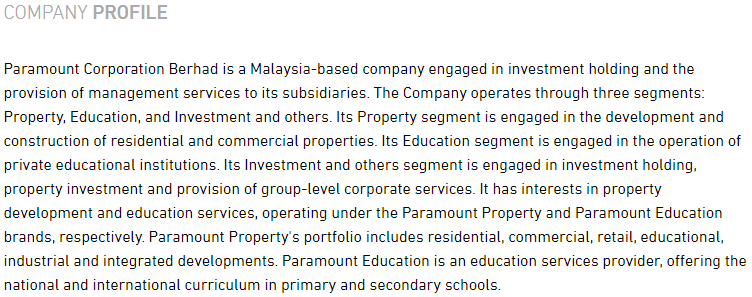

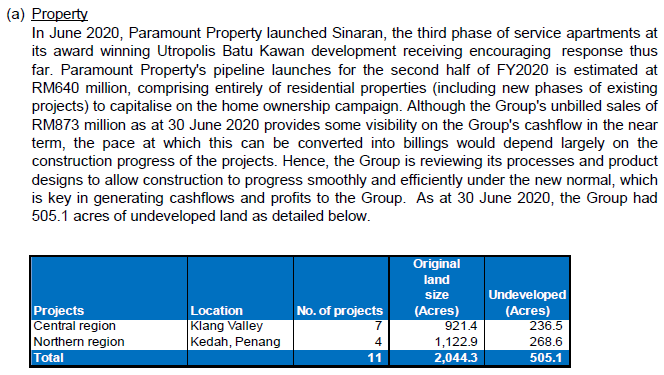

1. PARAMON (1724)

Catalysts

- Large Landbank and GDV

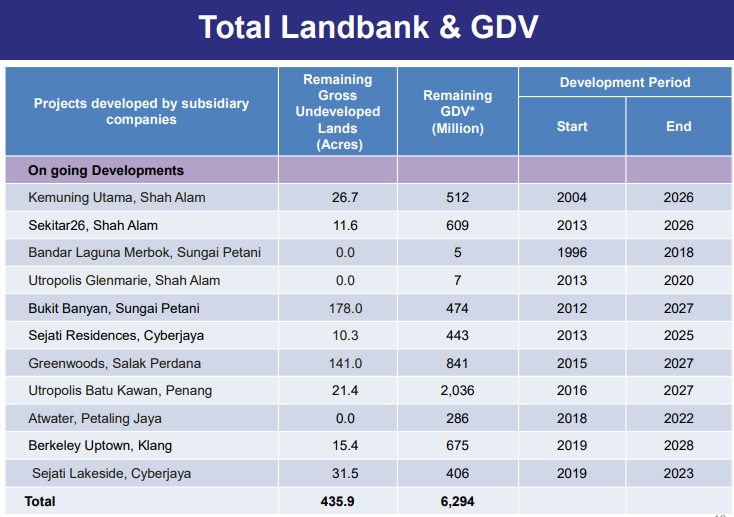

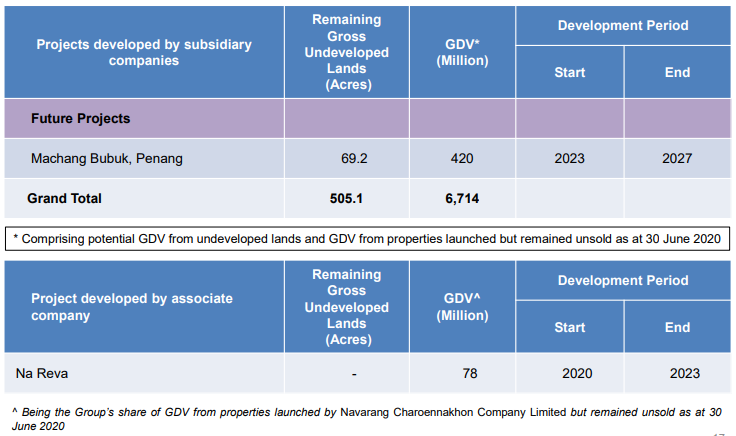

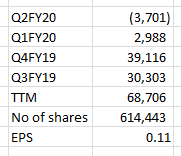

In its latest Q2FY20 results, PARAMON had highlighted its pipeline launches for 2H2020 is estimated at RM640mil. In addition, PARAMON currently has unbilled sales of RM873mil as at 30 June 2020.

Notwithstanding the above, PARAMON has undeveloped lands amounted to 505.1 acres with potential GDV of RM6,714mil.

2. Reversion to Sector Mean P/E

![]()

Based on peer analysis, the Trailing P/E of PARAMON at 6.5x is relatively low as compared to its sector average P/E of 14.6x. Even at a conservative take profit P/E of 10-12x, there is at least 50% upside to PARAMON.

Risks

- Unexpected delay in project completion

- Increase in debt burden

- Lower sales of new properties than expected

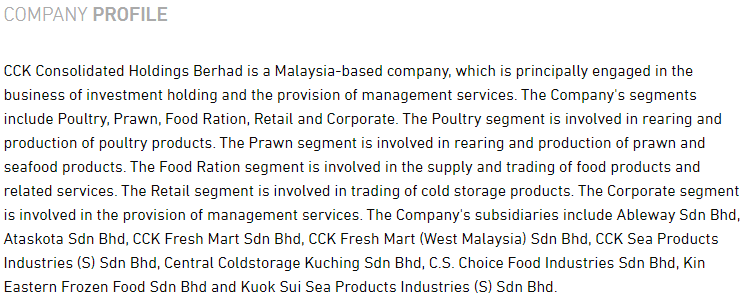

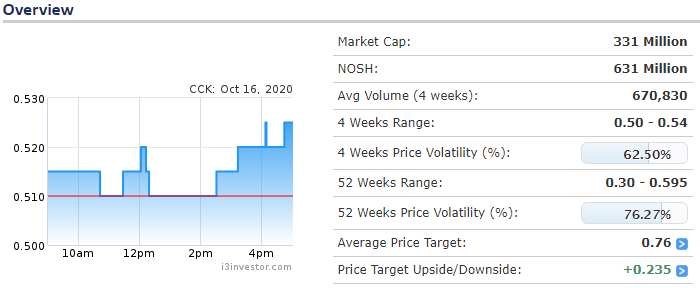

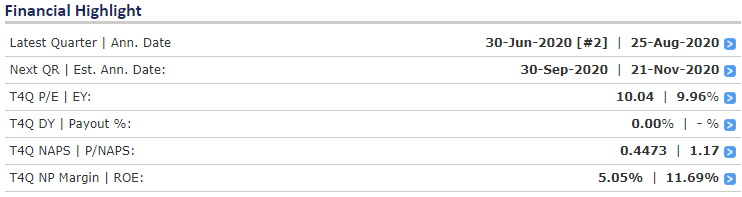

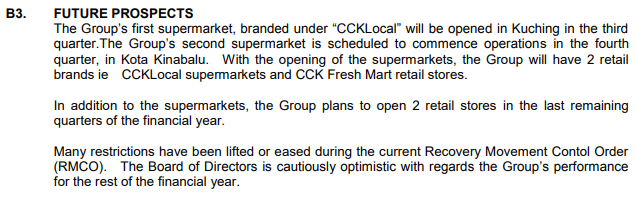

2. CCK (7035)

Catalysts

- Venture into Supermarket Business

CCK had launched its 1st supermarket, CCK Local at Kuching City Mall on 31st July 2020. From its Facebook page, the supermarket has similar layout to premium supermarket such as Jaya Grocer, Cold Storage and Village Grocer. Also, the supermarket seems to carry a fair share of imported groceries from Australia and New Zealand.

Source: https://www.facebook.com/CCKLocal/photos/?ref=page_internal

2. Reversion to Sector Mean P/E

![]()

Based on peer analysis, the Trailing P/E of CCK at 10x is relatively low as compared to its sector average P/E of 19.7x. Even at a conservative take profit P/E of 13-15x, there is at least 30% upside to CCK.

Risks

- Lower sales from retail segment due to MCO

- Unexpected delay in new supermarket launching

- Unfavorable exchange rate

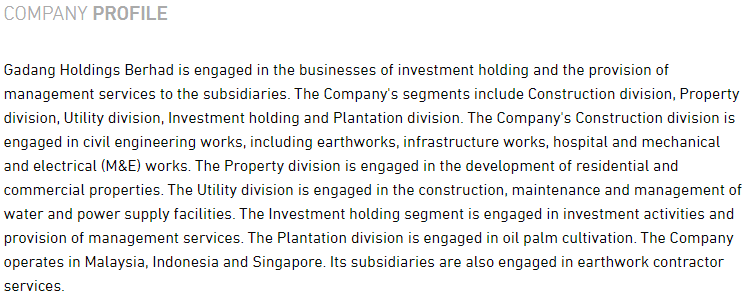

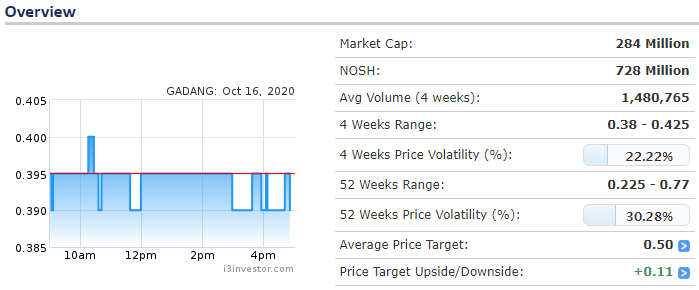

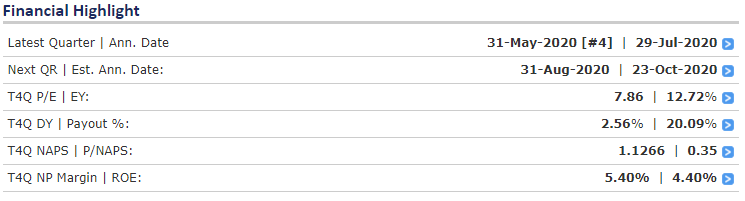

3. GADANG (9261)

Catalysts

- Higher Recurring Income

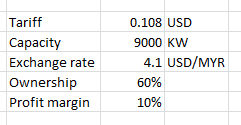

GADANG has highlighted that the construction of the 9MW mini-hydro power plant in Lintau, Sumatera, is progressing well and is scheduled for completion by the end of 2020.

Based on a conservative profit margin of 10%, the 9MW mini-hydro power plant is expected to contribute approximately RM2.0mil in profit.

Source: https://repit.wordpress.com/projects/feed-in-tariff-fit/

2. Reversion to Sector Mean P/E

![]()

Based on peer analysis, the Trailing P/E of GADANG at 7.4x is relatively low as compared to its sector average P/E of 17.0x. Even at a conservative take profit P/E of 10-12x, there is at least 35% upside to GADANG.

Risks

- Unexpected delay in project completion

- Lower than expected in order book replenishment

- Unfavorable exchange rate

DISCLAIMER: The information above is provided for education purpose only and does not constitute a buy or sell recommendation. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of you acting based on this information.

More articles on Alpha Stock Hunt

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

2

3

4

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

5

6

Koon Yew Yin's Blog

CPO price is rising rapidly as shown by chart below - Koon Yew Yin

7

Axcapital's investment blog

KAB - Executing its way to a record quarter. Could more Petronas contracts be coming?

8

save malaysia!

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....